Rate Cuts on Hold as Fed Confronts Stubborn Inflation

Top of Mind: We think there is still an opportunity to manage reinvestment risk as we await lower interest rates.

Key Takeaways

Lingering inflation continues to challenge monetary policy. The Fed left short-term interest rates unchanged at a two-decade high.

Despite recent upticks in inflation, we believe pricing pressures should ease as rent growth retreats, which should calm core inflation.

As we await lower rates, we believe there's still an opportunity to manage the emerging threat of reinvestment risk in fixed-income portfolios.

The Federal Reserve (Fed) left its short-term interest rate target unchanged on May 1, acknowledging a lack of further progress in taming inflation. While the economy logged a weaker-than-expected first-quarter annualized growth rate of 1.6%, policymakers stayed fixated on restoring 2% core inflation.

Year-over-year headline inflation jumped for the second consecutive month in March to 3.5%, its highest level since September. Core inflation (excludes food and energy prices) was 3.8% in March, unchanged from February. The Fed’s favorite inflation gauge, core personal consumption expenditures (PCE), held at 2.8% in March, the same as February’s reading.

Fed Board Chair Jerome Powell reiterated the Fed’s rationale for holding interest rates steady. Policymakers still believe rates are sufficiently restrictive to stem core PCE. But Powell noted the timetable may be longer than originally expected, and the Fed will keep rates higher for as long as necessary.

Despite this uncertainty, we still believe easing should start later this year. Shelter costs, a key component of unwavering inflation, have been slowing and may ultimately drive down core inflation. If this outlook unfolds, we believe investors should consider how falling interest rates could affect their cash and fixed-income allocations.

Trends in Housing Data Suggest Inflation May Soften

We believe there may be good reason for the Fed to remain patient with core inflation data. Specifically, rent payments are slowing.

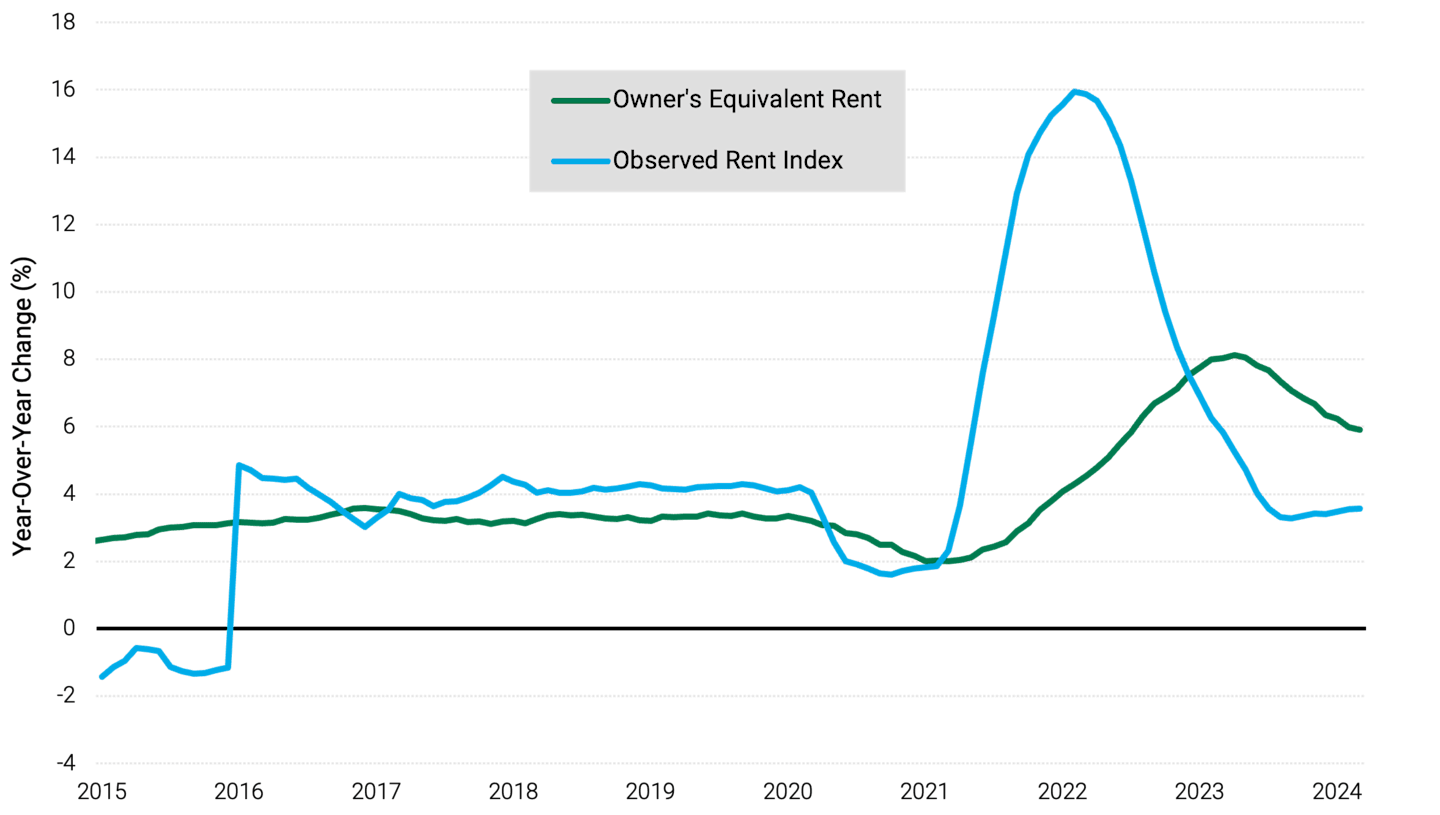

Shelter costs have been a primary driver of inflation’s persistence, accounting for more than 60% of the core Consumer Price Index’s (CPI’s) year-over-year increase. CPI’s shelter component includes rental values, lodging away from home and owners’ equivalent rent (OER), the component’s largest module. OER represents the amount of monthly rent equal to the monthly expenses of owning a home.

While the year-over-year change in OER has trended lower recently, it’s still nearly double pre-COVID levels, as Figure 1 illustrates. Meanwhile, Figure 1 also shows that growth in actual rental payments has dropped to pre-2020 levels. We believe the slowdown in actual rent growth is a good predictor of a continued downward move in OER.

Figure 1 | Rent Costs Show Signs of Cooling

Data from 1/30/2015 - 3/29/2024. Source: FactSet; Zillow Economic Research.

As Rate Cuts Come into Focus, Reinvestment Risk Rises

In our view, recent trends in rent payments should eventually curb the core inflation rate, allowing the Fed to cut rates. This view underscores what we believe is a pertinent issue for fixed-income investors — reinvestment risk.

Reinvestment risk is the possibility that investors may not be able to reinvest cash flows at the same yield they’re currently earning. This risk typically emerges when interest rates are falling, presenting a two-pronged challenge for some fixed-income investors:

Rates on Treasury bills, savings accounts, CDs and other cash equivalents typically move in tandem with the federal funds rate. So, when the Fed cuts short-term rates, yields on these holdings also drop, reducing investors’ monthly income.

A declining interest rate environment typically drives bond prices higher, pushing up the cost of reinvesting in longer-maturity, higher-yielding securities.

Responding to a Changing Rate Environment

If the Fed starts cutting rates later this year, yields on Treasury bills, CDs and similar products will likely drop, too. Therefore, reinvesting in these same vehicles won’t provide the return potential they’re offering today.

In our view, there is still time to confront reinvestment risk before the Fed changes course. Waiting until rates decline to shift into higher-yielding, longer-maturity bonds could mean buying bonds at higher prices. But making the move before Fed easing may help by:

Securing today’s relatively higher yields.

Adding duration, which can generate capital appreciation when interest rates fall.

Our fixed-income managers believe higher-quality bonds with attractive yields, including U.S. Treasuries and higher-credit-quality corporate and securitized bonds, may help weather a slower economy.

Stay Focused on Your Investment Plan

As in all periods of market uncertainty, we believe it's imperative to remain disciplined and focused on your specific investment plan. Investing across multiple asset classes and focusing on risk management may be prudent in the current market climate.

It’s also important to remember that attractive investment opportunities often emerge during these periods. We suggest investing with experienced professionals with the insights and discipline to recognize and potentially capitalize on such prospects.

Authors

Inflation in Focus

Get market updates, behavioral insights and investment ideas.

Past performance is no guarantee of future results. Investment returns will fluctuate and it is possible to lose money.

References to specific securities are for illustrative purposes only, and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments' portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

In certain interest rate environments, such as when real interest rates are rising faster than nominal interest rates, inflation-protected securities with similar durations may experience greater losses than other fixed income securities. Interest payments on inflation-protected debt securities will fluctuate as the principal and/or interest is adjusted for inflation and can be unpredictable.

Generally, as interest rates rise, the value of the bonds held in the fund will decline. The opposite is true when interest rates decline.

Diversification does not assure a profit nor does it protect against loss of principal.