Welcome to American Century Investments®

The Countdown Is On!

Your retirement plan is closing, but there's still time to stay in charge of where your money goes. That’s how we can help. Call us for guidance about your options and which investments may be most suitable—all at no charge. We want to help you make the best decision for you. Get started by talking to a specialist.

Call 888-

What Are Your Options?

Move Your Money Now

Move your money to a Rollover IRA now and keep saving for your future—in an investment you choose and that works for your specific goal.

Wait—Let It Auto Move

Take no action and your money will automatically move to a Rollover IRA into a money market fund, which are generally not designed for retirement. Additional steps will be required to access your money.

Cash Out With Penalties

Withdrawing your retirement savings can be tempting, especially for short-term expenses. But taking your money now may cost you in taxes and penalties.

Hear more about your options? Call us at 888-

A Rollover Individual Retirement Account (IRA) allows you to save for retirement tax-deferred, meaning you won't pay taxes until you withdraw the money. It's intended for money "rolled over" from a qualified retirement plan, like your employer’s. When you choose a Rollover IRA, the tax-deferred benefits you had with your retirement plan stay intact, and there is no penalty to roll over the money.

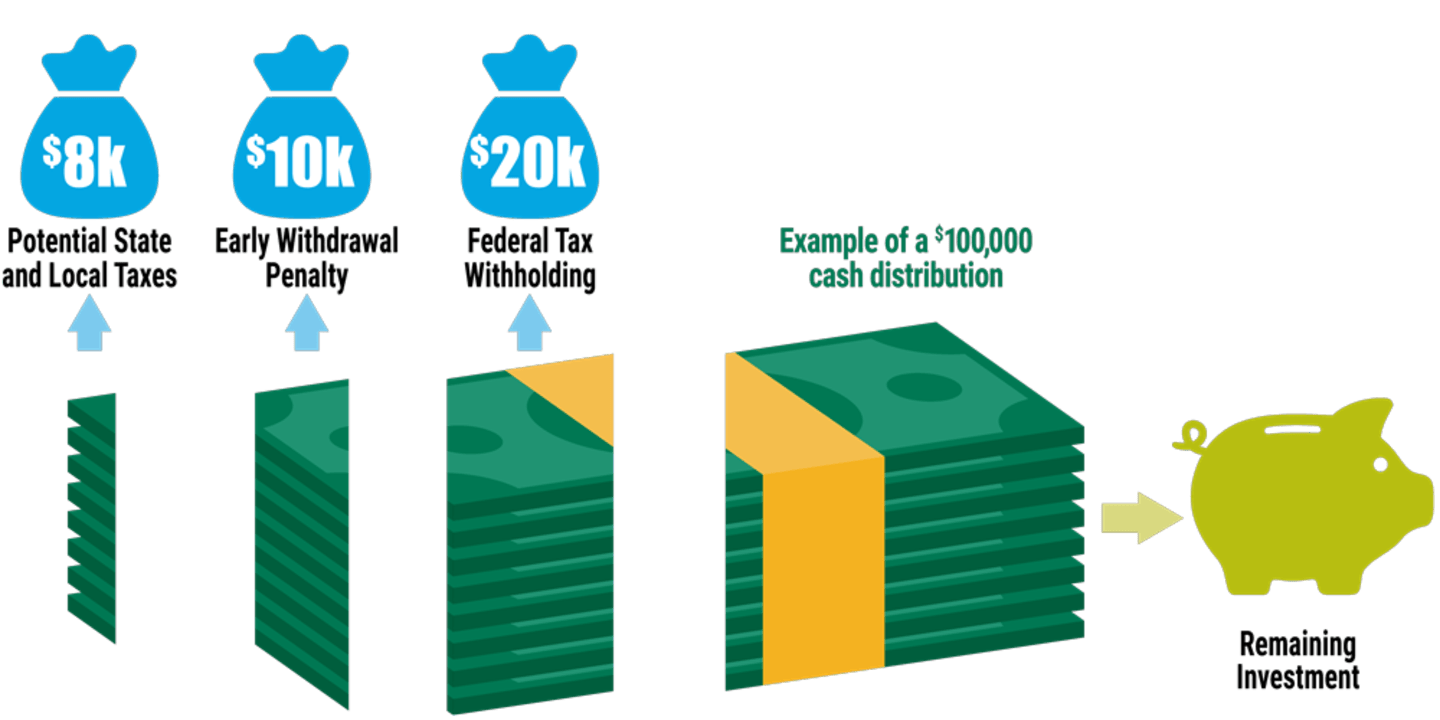

Thinking about Cashing Out? Think Again.

Depending on your situation, you could end up with about 60% of your original savings due to taxes and penalties if you are under age 59½. *

* Taxes are deferred until withdrawal. State and local income taxes may also apply at withdrawal. A 10% penalty will be imposed for early withdrawal.

Special rules apply to Roth assets. Please consult your tax advisor.

Penalty may apply if you don’t meet the age requirements.

Investment Options

We believe a sound diversification strategy aligned with your goals is the foundation of long-term investing success. A good mix of investments is key to weathering the ups and downs of the market. Explore our target date portfolios designed specifically for retirement investing or build your own portfolio from our complete list of funds. Note, our free guidance also includes help with choosing a portfolio that fits you. Call 888-

Option 1: Invest with Target Date Portfolios

Explore One Choice® Target Date Portfolios, designed specifically for retirement investing. Simply find a fund based upon your birth year and future retirement date. Your money will be automatically diversified in up to 16 funds in a single investment.

A One Choice Target Date Portfolio's target date is the approximate year when investors plan to retire or start withdrawing their money. The principal value of the investment is not guaranteed at any time, including at the target date.

Each target-date One Choice Target Date Portfolio seeks the highest total return consistent with American Century Investments' proprietary asset mix. Over time, the asset mix and weightings are adjusted to be more conservative. In general, as the target year approaches, the portfolio's allocation becomes more conservative by decreasing the allocation to stocks and increasing the allocation to bonds.

By the time each fund reaches its target year, its target asset mix will become fixed and will match that of One Choice In Retirement Portfolio.

One Choice® In Retirement Portfolio

Birth Year: 1962 or earlier

Retirement Year at Age 65: 2027 or earlier

Birth Year: 1963 – 1967

Retirement Year at Age 65: 2028 – 2032

Birth Year: 1968 – 1972

Retirement Year at Age 65: 2033 – 2037

Birth Year: 1973 - 1977

Retirement Year at Age 65: 2038 – 2042

Birth Year: 1978 – 1982

Retirement Year at Age 65: 2043 – 2047

Birth Year: 1983 – 1987

Retirement Year at Age 65: 2048 – 2052

Birth Year: 1988 – 1992

Retirement Year at Age 65: 2053 – 2057

Birth Year: 1993 – 1997

Retirement Year at Age 65: 2058 – 2062

Birth Year: 1998 – 2002

Retirement Year at Age 65: 2063 – 2067

Birth Year: 2003 and after

Retirement Year at Age 65: 2068 and after

Key Benefits:

- Instant, broad diversification

- Professionally and actively managed

- Adjusts to grow more conservative

Option 2: Build Your Own Portfolio

Choose different investment types for a well-rounded portfolio. That includes a variety of stock, bond and cash equivalent investments, such as a money market fund. The investment mix you select should align with your risk comfort level, your timeline and investment goal. Creating this kind of diversified portfolio can potentially offer a smoother ride through market volatility.

Answers for Your Questions

Taking your retirement plan money in cash may provide quick access, but it may not be the best long-term financial move because of the possible tax consequences. You can end up with about 60 percent of your original savings due to taxes and penalties if you’re under age 59½. Plus, you lose the opportunity for your investment to continue to grow in a tax-deferred account.

Yes, you can make contributions to your IRA subject to the IRA annual contribution limits. Note that adding a contribution will change the status of your IRA from a "Rollover" to a traditional IRA. You must also keep Roth IRA and traditional IRA money separate.

If you combine rollover assets and new contributions in the same account, the combined assets are considered "commingled" and may not be able to be rolled over into a new employer's plan.

Yes, you can contribute to a traditional and/or Roth IRA even if you participate in an employer-sponsored retirement plan (including a SEP or SIMPLE IRA plan), as long as you stay within the IRS annual contribution limits.

Yes. You can roll over Roth dollars from a qualified retirement plan (for example, a 401(k) plan), into a Roth IRA. With a Roth IRA, you make contributions with money you've already paid taxes on (after-tax) and your money may potentially grow tax-free. Different from a Traditional or Rollover IRA, you won't pay taxes when you withdraw the money in retirement, as long as you have had the account for at least five years and you are at least age 59½.

For 65 years, American Century Investments has helped investors like you with their retirement goals. Our mission is to help you succeed. We also know that how we invest and serve you matter as much as the mission. They’re important for your investing world and the world we all live in.

How? Every year, 40% of our dividends fund breakthrough medical research aimed at defeating diseases like cancer and Alzheimer’s. When you invest with us, you also become part of the story. Learn more about this unique purpose and how we’re in it together.

Your employer and American Century Investments are working together to provide retirement solutions to help you stay on the right path toward retirement. That includes help deciding the next step for your retirement savings and free investment guidance.

A Plan Closing Doesn’t Have to Derail Your Plans

A specialist can help walk through your options and make the decision that’s right for you.

Educational Tools & Resources

We understand all the different options that you are facing when deciding what to do with your 401(k) money. Our educational pieces and calculators are designed to help you make the decision that's right for you.

Diversification does not assure a profit nor does it protect against loss of principal.

IRS Circular 230 Disclosure: American Century Companies, Inc. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated with American Century Companies, Inc. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

This information is for educational purposes only and is not intended as tax advice. Please consult your tax advisor for more detailed information or for advice regarding your individual situation.

This information is for educational purposes only and is not intended as a personalized recommendation or fiduciary advice. There are different options available for your retirement plan investments. You should consider all options before making a decision. Our representatives can help you evaluate all of your distribution options.

IRA investment earnings are not taxed. Depending on the type of IRA and certain other factors, these earnings, as well as the original contributions, may be taxed at your ordinary income tax rate upon withdrawal. A 10% penalty may be imposed for early withdrawal before age 59½.

Please consult your tax advisor for more detailed information regarding the Roth IRA or for advice regarding your individual situation.

Taxes are deferred until withdrawal if the requirements are met. A 10% penalty may be imposed for withdrawal prior to reaching age 59½.

You could lose money by investing in a mutual fund, even if through your employer's plan or an IRA. An investment in a mutual fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

You should consider the fund's investment objectives, risks, charges and expenses carefully before you invest. The fund's prospectus or summary prospectus, which can be obtained by calling 1.800.345.2021, contains this and other information about the fund, and should be read carefully before investing. Investments are subject to market risk.

American Century Investment Services, Inc., Distributor

©2026 American Century Proprietary Holdings, Inc. All rights reserved.