401(k) Plans Should Play Better Defense for Younger Participants

Target-date funds with less aggressive equity allocations can better serve younger participants when considering all risks, including leakage.

Key Takeaways

Young 401(k) participants face unique risks that challenge the traditional high-equity approach of target-date funds.

While high equity allocations aim to maximize returns over long horizons, early withdrawals and market volatility pose significant threats to retirement savings for younger workers.

A more balanced risk-return approach with moderate equity exposure may better protect and grow younger participants’ retirement savings.

Rethinking Equity Allocations for Younger Workers

Many 401(k) plan sponsors feel compelled to choose target-date funds (TDFs) that have recently delivered strong returns. In an environment where equities have performed well, this means funds with high equity allocations.

They reason that doing so helps plan participants build their account balances, particularly those with a less-than-optimal savings record. Therefore, this emphasis on returns and high equity allocations can be particularly notable in TDFs for young plan participants.

At the same time, younger participants' contributions to their 401(k) accounts — both in dollar terms and as a percentage of income — are often relatively low. Noting this, defined contribution (DC) plan sponsors often believe that because younger participants have many years ahead of them before they retire, they should allocate most of their 401(k) savings to equities.

As we discuss here, combining these things can result in suboptimal equity allocations for young plan participants.

Glide paths with high equity allocations implicitly endorse the view that, because younger workers won’t retire for decades, they can and should accept the risk that goes along with high equity exposures.

However, the assumptions embedded in academic research that lead to recommended equity allocations as high as 100% in the early years often do not capture what happens in the real world.

In this article, we argue that TDFs with less aggressive glide paths may better serve young workers and that 401(k) plan sponsors should not use past returns as the main criterion for selecting TDFs.

We show that high equity allocations ignore sequence-of-returns risk and leakage/ abandonment (early withdrawals) and downplay the importance of establishing strong savings habits early in one’s career. This is a disservice to younger participants, who could end up with significantly larger retirement nest eggs if their TDFs played smarter defense.

Is There a Typical Glide Path for TDFs?

The U.S. equity market has delivered impressive returns over the past decade. As a result, TDFs with aggressive equity allocations and a higher-for-longer glide path have outperformed more conservative TDFs. This, in turn, has pushed more TDF providers to use increasingly higher equity allocations.

While this trend has led to high returns for many, we argue that return is not the only metric 401(k) plan providers should use in selecting TDFs.

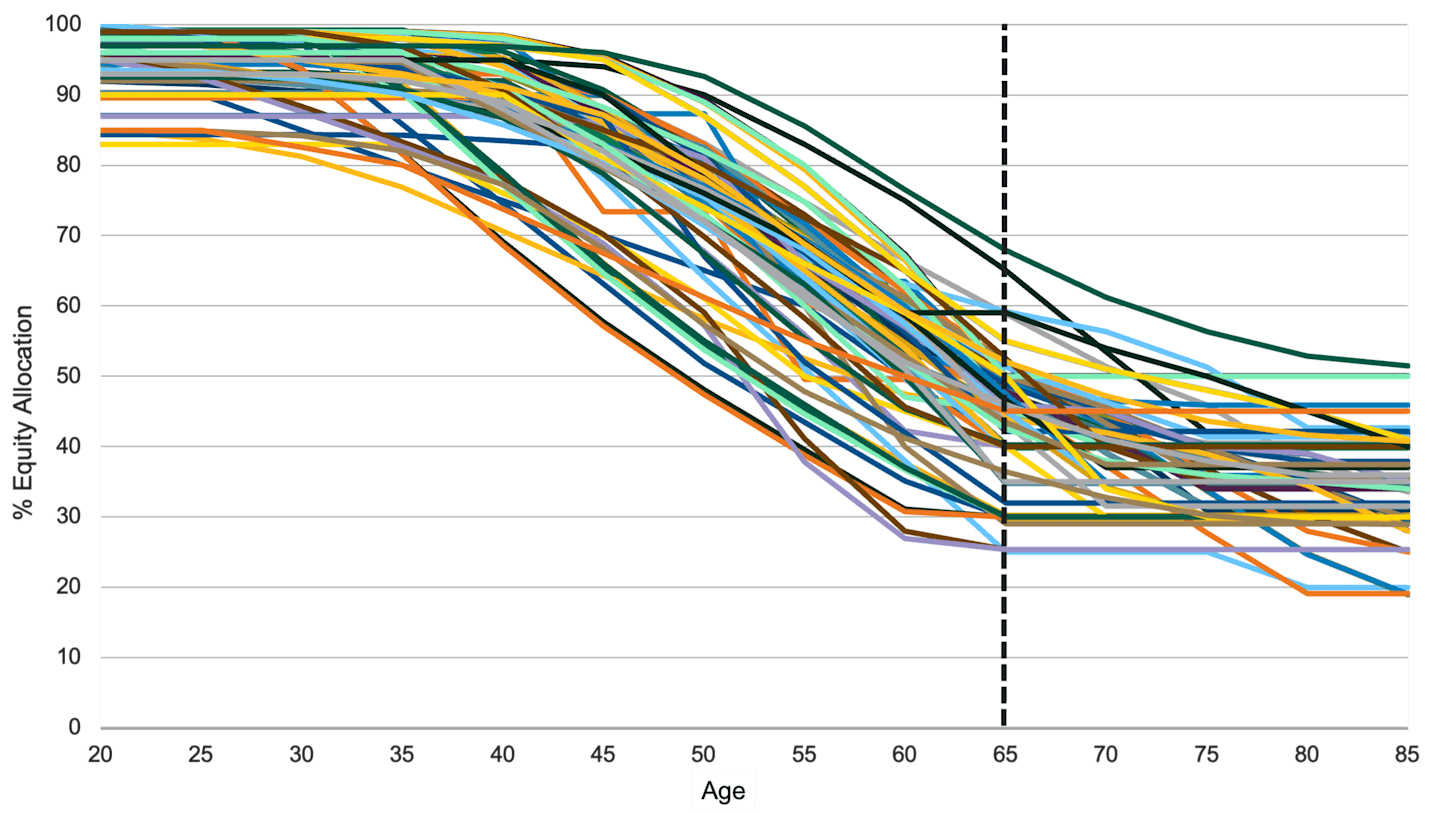

Consider the range of equity allocations in the glide paths embedded in TDFs used by 401(k) plans. Figure 1 shows that many TDFs use equity allocations of 95% or higher for plan participants in the early stages of their careers and keep close to 70% in equities until retirement is less than 10 years away. Still, many are less aggressive, and some are quite conservative.

Figure 1 | Equity Allocations (Glide Paths) of TDFs from the Largest U.S. Asset Managers

Data as of 6/30/2025. Source: Fund prospectuses and websites, Morningstar.

There are substantial differences among TDF glide paths because providers disagree about the best approach and inputs needed to determine what is optimal. Still, asset managers know many DC plan sponsors choose TDFs based on past returns.

Therefore, many TDF providers retain very high equity allocations for the first 20 to 25 working years, increasing risk for young and mid-career participants whose savings are invested in these funds.

Sequence-of-Returns Risk in TDFs

High equity allocations in TDFs may underestimate sequence-of-returns risk, where the timing of investment returns affects outcomes. This concept explains why two savers who experience the same arithmetic average returns can end up with significantly different account balances, depending on the order in which those returns occur.

Naïve discussions of sequence-of-returns risk argue that the pattern of returns only matters in the withdrawal phase (post-retirement), not the accumulation phase (pre-retirement).

However, claiming that two series of returns with the same arithmetic average will produce the same investment result assumes investors do not contribute to or take distributions from their accounts. This assumption does not hold up in the real world.

Not only do plan participants make ongoing contributions, but many sources show that 40% (or more) of Americans have taken early withdrawals from their 401(k)s.1

A Wall Street Journal article titled “Americans See Their 401(k)s Not Just as Nest Eggs but as Rainy Day Funds” notes that nearly one-third of people who leave their jobs do not roll 401(k) assets over into another tax-deferred retirement account.2 The Secure 2.0 Act of 2022 made it easier to take hardship and certain other withdrawals, and in most cases, it was penalty-free.

Many Plan Participants Treat Their 401(k) Funds as Emergency Savings

Worsening the impact of early withdrawals, the hardship that often motivates them is a job loss. When unemployment rises due to a weak economy or recession, the equity markets are likely to suffer a downturn.

In this scenario, those who take early withdrawals from TDFs with high equity allocations are forced to sell more of their holdings to generate the cash they need. This permanently reduces the base on which to build future returns. Withdrawals in a declining stock market would not erode a participant’s holdings to the same degree if a TDF had a less aggressive equity allocation.

Of course, job loss is not the only reason for early withdrawals. Employees are increasingly auto-enrolled in 401(k) plans, and if they get into financial jams, these accounts can look like “found money.” Of the close to 40% of Americans who have taken early withdrawals, 24% do so to pay down personal debt, and 21% use the money to meet recurring bills.3

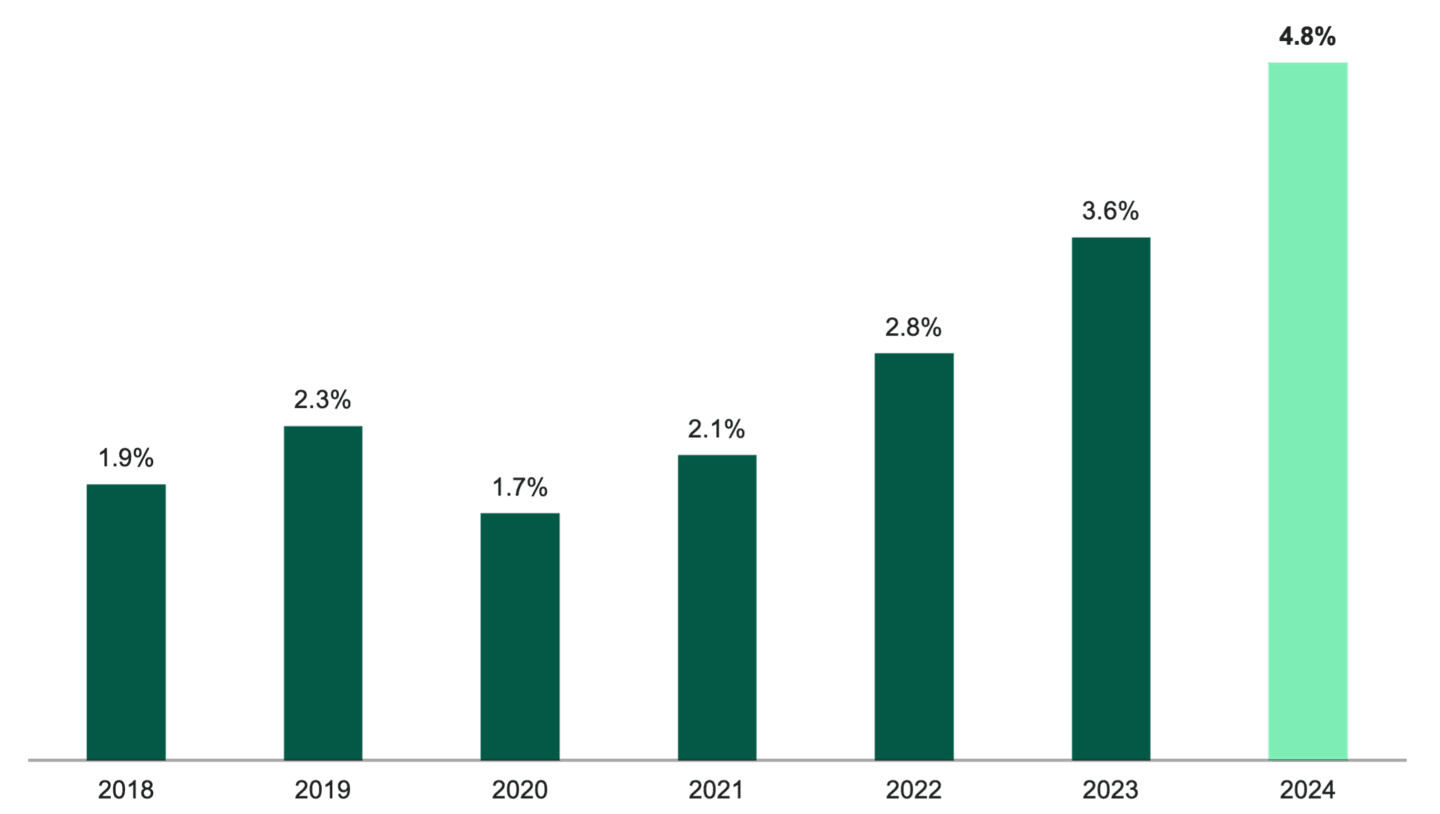

According to Vanguard, a record number of plan participants (4.8%) took hardship withdrawals from 401(k)s in 2024, as shown in Figure 2.4

Figure 2 | A Growing Number of Employees Are Using 401(k) Accounts as Emergency Funds

Data from 2018 – 2024. Source: Vanguard Group. Note: Based on nearly five million 401(k)-type accounts.

Gen Zers, who are early in their work lives, have the highest percentage (26%) of hardship/ early withdrawals from a 401(k) plan of any age group. The same Vanguard survey reported that 51% of Gen-Z workers struggle to make ends meet.5

Many are also paying down student loans, as the lengthy COVID-era moratorium on repaying these loans has ended. Those defaulting on federal student loans could have their wages garnished.

This increases the likelihood that younger plan participants will make early withdrawals from their 401(k) accounts, exposing them to sequence-of-returns risk.

Return Volatility Increases Abandonment

Aside from sequence-of-returns risk, evidence shows that investors who experience volatile returns and large losses are at risk of moving out of equity investments entirely in favor of cash. Of course, this means their returns will not keep up with inflation. Worse, many will throw in the towel when equity market volatility becomes too great to stomach, abandoning their savings plan altogether.

High volatility and large losses are more likely to happen in TDFs with high equity allocations.

Abandonment risk can be particularly acute for younger participants who may, after suffering a big loss, decide to pay the penalty, use whatever they have left for some other purpose (a YOLO mentality), and start saving sometime later.

Furthermore, pushing equity allocations higher in the hopes of boosting returns offers comparatively little benefit to young plan participants because their account balances are typically fairly small.

A better approach: Our research shows that balancing return and risk considerations in the glide path and avoiding extremes in equity allocation, even for younger participants, may help mitigate sequence-of-returns risk. It also has the potential to reduce abandonment risk by reducing volatility, which may help younger participants stay the course.

Why Take More Investment Risk if It’s Not Necessary?

A higher savings rate means account balances grow faster. Therefore, participants who save at a decent rate do not need aggressive equity allocations. Given these reasons, more moderate and stable TDFs may suit them better.

Figure 3 examines the average return, standard deviation and Sharpe ratio for various blends of stocks and bonds computed from six-year windows of rolling quarterly returns. We use the six-year windows because, as discussed above, many plan participants take early withdrawals. Thus, returns calculated over lengthy periods may not capture what many workers actually experience.

Figure 3 | Less Aggressive Equity Allocations Have Offered More Attractive Risk-Adjusted Returns

Calculated from quarterly returns over rolling six-year windows from June 30, 2005, through June 30, 2025. Values are annualized. The risk-free rate used to compute Sharpe ratios is the three-month T-bill rate. Source: FactSet.

These results show that although higher equity allocations generated higher returns, on a risk-adjusted basis, the more balanced allocations were more efficient. The analysis shows that based on broad market index returns, an 85% stock/15% bond mix earned 90% of the gains of a 100% equity allocation with only 85% of the risk.

Which Matters More: Savings Rate or Investment Return?

Research shows equity allocations along a TDF’s glide path should not be viewed in isolation; participants’ savings rates should be an integral part of determining what is optimal, along with risk tolerance, lifecycle consumption patterns and other factors.6

The Good News: A 2025 Transamerica Center for Retirement Studies survey shows that 76% of Gen-Z workers are saving for retirement through 401(k)s or similar workplace plans.7 And, of the Gen Zers contributing to a retirement savings plan, the majority are doing so at a rate that is not too far behind their older peers. A recent survey from Fidelity shows the average 401(k) savings rate for Gen-Z employees is 11.2%, versus 13.5% for Millennials and 15.4% for Gen-Xers.8

The Bad News: TDF providers rarely acknowledge that a plan’s recommended savings rate has implications for optimal equity allocations; they are essentially treated as independent decisions.

Figure 4 illustrates the relationship between a participant’s savings rate and the annual average return from investing in TDF. From the perspective of a young participant with a zero balance at the start of the period, the analysis shows that a one percentage point increase in the participant’s savings rate makes a bigger difference in accumulated wealth after 10 years. This is more significant than a 1 percent difference in annual returns.

Figure 4 | Comparing Outcomes for Two Participants

A higher savings rate created more wealth than a higher return.

This data is for illustrative purposes only. Source: American Century Investments.

Of course, having a higher savings rate and a high average return would be ideal. However, participants only control their savings rate and can increase it without taking on more risk, especially with support from the plan sponsor. The average return is not under the participant’s or the plan’s control.

Challenging the Case for Higher Equity in Target-Date Funds

Lastly, we address three commonly heard arguments for why younger participants should accept higher risk in their TDFs.

Argument: Younger plan participants have a high risk tolerance and thus should take on more equity risk than older workers, who tend to have a lower risk tolerance.

Counterargument: There is a difference between an individual’s risk tolerance and risk capacity. While risk capacity—how much risk an individual can afford to take—is higher when retirement is far off, research suggests that risk tolerance is a relatively stable personality trait and is unlikely to change significantly over an individual’s life.9 Therefore, young people are not necessarily more risk-tolerant than their older counterparts, just further from retirement, which gives them a higher risk capacity.

Argument: Aggressive equity allocations make sense when retirement is far off.

Counterargument: Evidence presented here shows that younger 401(k) plan participants often do not buy and hold all the way to retirement; thus, the argument that they should be almost 100% invested in equities does not hold up. Furthermore, equity returns going forward are unlikely to resemble what we have experienced over the past 10 years. Given historical equity and bond returns, the recent double-digit equity return premium over bonds is unlikely to continue.

Argument: Younger people are risk-takers in their investing habits, so TDFs should reflect this.

Counterargument: Gen Zers are increasingly exploring nontraditional ways to grow their wealth and income, including cryptocurrencies and sports betting. While this shows a willingness to accept significant losses in pursuit of gains, it suggests young plan participants need less volatility and greater certainty from their retirement plan savings to balance risk-taking in other areas. DC plan sponsors should also consider that income uncertainty and wealth affect risk tolerance differently for men and women.10

Rethinking Retirement Strategy for Younger Employees

There is no disputing the fact that the more an individual saves for retirement, the better. And leaving those savings untouched to compound returns is critical to achieving financial security in retirement. However, 401(k) plan participants do not always save optimally, and many tap those savings long before they retire.

As a result, sequence-of-returns risk is relevant for younger participants, who may not be as risk-tolerant as conventional wisdom suggests. Given the realities of how Gen Zers tend to view their 401(k) savings, we believe plan sponsors should consider the risks they face and focus on achieving a higher savings rate rather than pursuing higher returns.

Thus, while it may seem counterintuitive, we believe it makes sense for 401(k) plans to choose TDFs that balance return and risk considerations for their younger participants instead of chasing past returns.

Authors

Take a Closer Look at Our Multi-Asset Solutions

The journey matters as much as the outcome.

Related Insights

Lynn Cavenaugh, “Nearly Half of Americans Have Taken Early 401(k) Withdrawals (Including Tim Walz),” BenefitsPRO, October 15, 2024.

Anne Tergesen, “Americans See Their 401(k)s Not Just as Nest Eggs but as Rainy Day Funds,” Wall Street Journal, July 26, 2025.

Lynn Cavenaugh, “Nearly Half of Americans Have Taken Early 401(k) Withdrawals (Including Tim Walz),” BenefitsPRO, October 15, 2024.

Aliss Higham, “Americans Are Dipping into Their Retirement Funds,” Newsweek, March 27, 2025.

Catherine Collison and Heidi Cho, “An Uncertain Future: Retirement Prospects of 4 Generations: 25th Annual Transamerica Retirement Survey of Workers, Transamerica Center for Retirement Studies®,” June 2025.

Radu Gabudean, Francisco Gomes, Alexander Michaelides and Yuxin Zhang, “On Optimal Allocations of Target-Date Funds,” Journal of Retirement, October 31, 2021.

Catherine Collison and Heidi Cho, “An Uncertain Future: Retirement Prospects of 4 Generations: 25th Annual Transamerica Retirement Survey of Workers, Transamerica Center for Retirement Studies®,” June 2025; Catherine Collison and Heidi Cho, “The Multigenerational Workforce: Life, Work, & Retirement: 24th Annual Transamerica Retirement Survey of Workers,” Transamerica Center for Retirement Studies®, June 2024.

Daniel de Visé, “We’re Saving Almost Enough in Our 401(k) Retirement Plans. Here’s the Magic Number,” USA Today, June 12, 2025.

Gerhard Van de Venter, David Michayluk and Geoff Davey, “A Longitudinal Study of Financial Risk Tolerance,” Journal of Economic Psychology 33, No. 4 (August 2012): 794-800.

Patti J. Fisher and Rui Yao, “Gender Differences in Financial Risk Tolerance,” Journal of Economic Psychology 61 (August 2017): 191-202.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

The information is not intended as a personalized recommendation or fiduciary advice and should not be relied upon for investment, accounting, legal or tax advice.

No offer of any security is made hereby. This material is provided for informational purposes only and does not constitute a recommendation of any investment strategy or product described herein. This material is directed to professional/institutional clients only and should not be relied upon by retail investors or the public. The content of this document has not been reviewed by any regulatory authority.