How Volatility Can Generate Opportunities in Corporate Bonds

New issues, especially those arising from M&A activity, may offer attractive opportunities for active corporate bond managers.

Key Takeaways

Elevated market volatility and robust corporate M&A and capital spending have boosted the number of new bonds available to investors.

When many issuers compete for investor dollars, new bonds often feature pricing incentives to attract buyers.

In our view, pricing incentives offer active investors an important source of performance potential that passive strategies can’t capture in real time.

Market volatility has recently been on the upswing, as investors digest the effects of Federal Reserve (Fed) policy uncertainty, uneven economic data and geopolitical unrest. While these short-term market swings can be unsettling, they can also prove rewarding, particularly for active bond managers seeking value and opportunity.

Why a Growing Supply of Corporate Bonds Matters

Recent market volatility hasn’t derailed issuance in the U.S. corporate bond sector, giving active managers a growing pool of potential investments. Whether to refinance maturing debt or finance mergers and acquisitions (M&A) and capital expenditures, corporations have unleashed a significant supply of bonds on the market.

Corporate bond issuance in the first two months of 2026 totaled nearly $485 billion, up 12.4% year over year.1

For issuers, timing is everything. Amid this year’s volatile backdrop and interest rate uncertainty, corporations have adjusted their bond issuance to capitalize on market swings.

Active Investing: The Key to Finding New Issues

Similarly, active investors have relied on the market’s ups and downs to secure value among corporate bonds. Unlike passive strategies, these investors can proactively pursue opportunities as issuers bring bonds to the market and as market conditions shift.

In our view, a key benefit of active management is the ability to uncover opportunities before they reach the broader bond market. Finding such issues is an ongoing effort involving stringent research and coordination with analysts, traders, portfolio managers and underwriters.

Supply Growth Helps Secure Lower Pricing

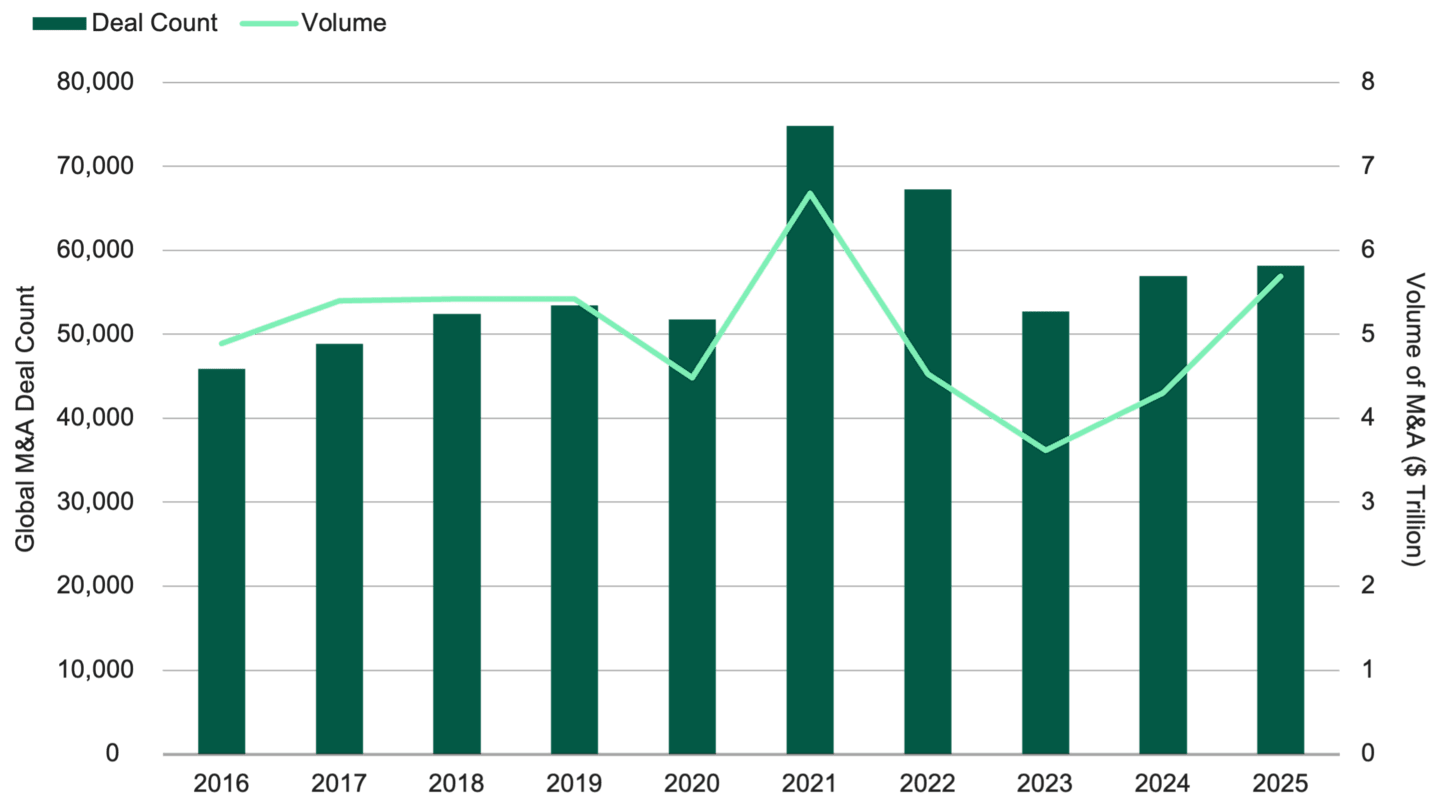

Robust M&A activity has represented a key source of recent bond-buying opportunities. The number of global M&A deals has soared since 2023, and the dollar volume of M&A climbed to $5.7 trillion in 2025, as Figure 1 illustrates. Announced M&A activity through the first two months of 2026 totaled more than $1.5 trillion on 12,192 deals, according to Bloomberg.

Figure 1 | M&A on the Rise

Data from 1/1/2016 – 12/31/2025. Source: Bloomberg.

The barrage of M&A-related debt has created a crowded marketplace, with issuers competing for investor dollars. And when multiple corporate bond issuers compete for buyers, pricing becomes the focus.

Meanwhile, heightened market volatility has increased uncertainty, a risk for which investors typically demand higher compensation.

When many companies issue bonds simultaneously, they’re competing for buyers. To stand out, an issuer may offer a pricing concession. This means the new bond may offer a modestly higher yield (at a lower price) than comparable bonds already trading in the market.

Pricing concessions provide incentives for bond fund managers to redirect investments from secondary holdings to new issues.

This dynamic has played out recently, as several transactions offered new issue discounts of 10 basis points (bps) to 20 bps. While seemingly small, these pricing concessions immediately provide a potential return advantage over comparable-maturity U.S. Treasuries.

Our research has identified a variety of corporate bond issuers offering such concessions recently, including:

Keurig Dr Pepper, a beverage company

Abbott Laboratories, a medical device and health care company

Honeywell Aerospace, an aircraft engine and avionics systems manufacturer

Eaton, a power management company

How Active Managers Evaluate New Opportunities

New issues remain an important source of potential value for active fixed-income managers. Unlike passive index-tracking portfolios, actively managed bond funds can monitor offerings in real time. If a new issue’s price, yield, maturity, risk profile and structure appear attractive compared to existing bonds, active managers can buy that bond right away.

Meanwhile, passive bond funds don’t have that flexibility. Because they track a market index, passive funds don’t have exposure to new issues until those issues enter the index. And this generally doesn’t happen until the end of the bond’s issuance month.

Active managers can often take advantage of issuers’ pricing concessions, a potential benefit typically out of reach for passive portfolios.

Pricing Concessions: A Key Theme Supporting Our Process

Identifying theme-driven sources of outperformance potential is a core component of our active management strategy. Amid elevated volatility and uncertainty, and an increase in bond-financed M&A, pricing concessions remain a key theme that we’re pursuing.

We believe capturing pricing concessions from select new issues remains a key advantage over passive strategies. Backed by sound research and risk-management processes, we view this theme as a compelling and repeatable source of value for corporate bond portfolios.

Authors

Mindset Built for Opportunity

We aim to provide the diversity, steady income and risk management that asset allocators seek from their fixed-income portfolios.

SIFMA, U.S. Corporate Bond Statistics, March 19, 2026.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

Investments in fixed income securities are subject to the risks associated with debt securities including credit, price and interest rate risk.

Generally, as interest rates rise, the value of the bonds held in the fund will decline. The opposite is true when interest rates decline.

Diversification does not assure a profit nor does it protect against loss of principal.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.