Are Small-Cap Stocks Finally Turning a Corner?

Since sweeping tariffs were announced in 2025, small-cap stocks have outperformed their large-cap peers. We believe several trends in 2026 may continue to favor small-caps.

Key Takeaways

Small-cap stocks have outpaced large-caps since last year’s Liberation Day tariff announcements, with the potential for continued momentum in 2026.

Accelerating earnings, interest rate cuts, tax incentives and reshoring are trends that support small-cap companies.

Regional banks, energy, and biotech stand out as potentially promising small-cap sectors due to strong fundamentals and improving industry dynamics.

Liberation Day – President Donald Trump’s April 2025 announcement of sweeping tariffs – was anything but liberating for small-cap stocks.

Small-caps are particularly sensitive to slowing economic growth and heightened uncertainty, two likely outcomes from tariffs. So small-caps sold off alongside the broader equity and bond markets.

But since then, small-caps have outperformed large-caps by 9% through February 9, 2026, according to FactSet. See Figure 1. This is good news for small-cap investors after several years of underperformance by the asset class. We think the pieces may be in place for a continued small-cap tailwind in 2026.

Figure 1 | Small-Caps Have Outpaced Large-Caps Since Liberation Day

Data from 4/2/2025 – 2/9/2026. Source: FactSet. Small-Caps represented by the Russell 2000® Index. Large-Caps represented by the Russell 1000® Index. Past performance is no guarantee of future results.

Why Multiple Economic Trends Are Supporting Small-Caps in 2026

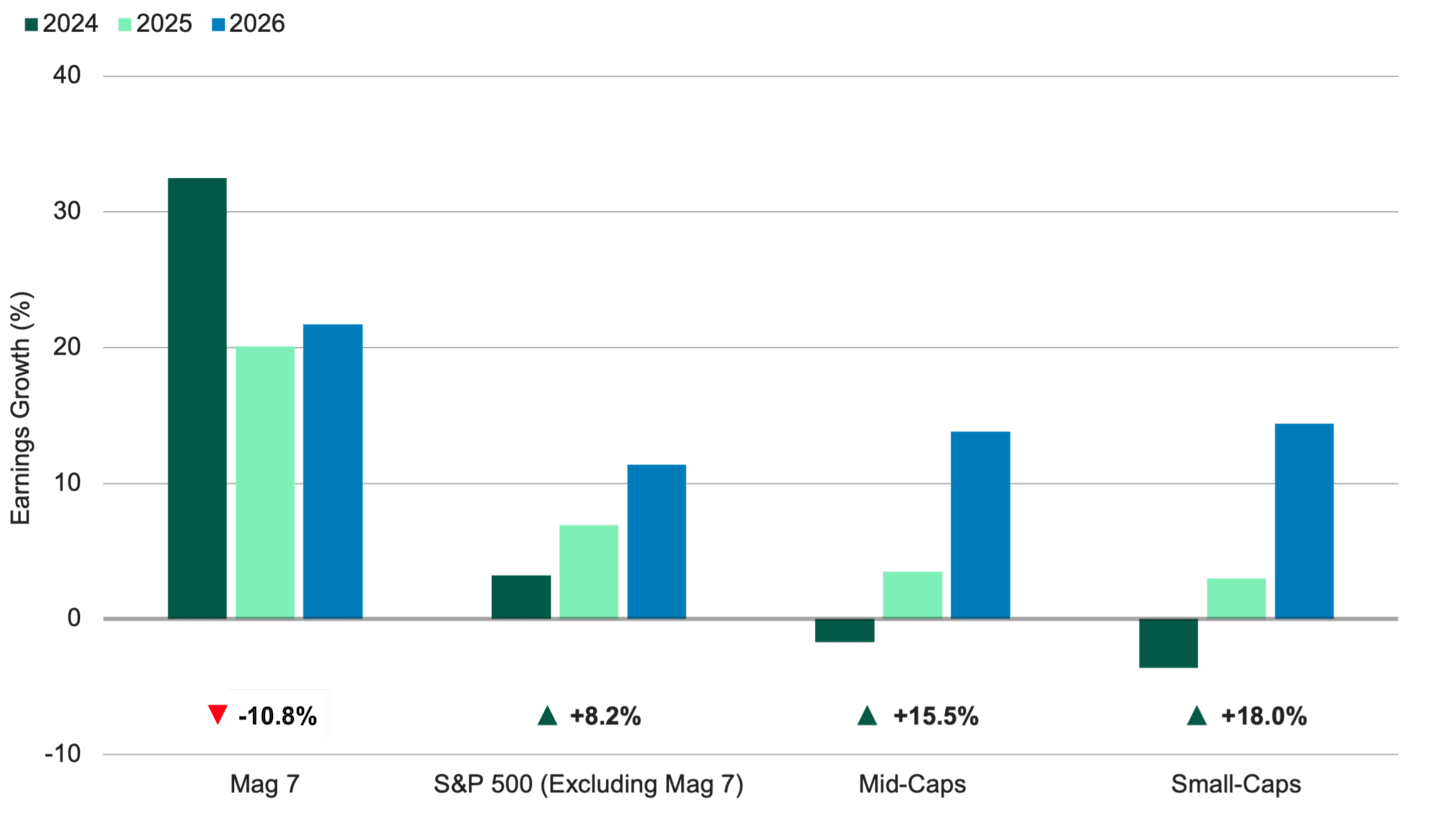

Small-cap earnings growth is expected to accelerate by nearly 20% after three years of stagnation, as shown in Figure 2. Meanwhile, mega-cap earnings growth, as represented by the Magnificent 7 (Mag 7), has shown signs of leveling off and possibly decelerating.1

Figure 2 | Small-Cap Earnings Acceleration Compared to Larger Peers

Data from 1/1/2024 – 12/31/2025. Source: FactSet, Standard & Poor’s, Jefferies. Mid-Caps represented by the Russell Midcap® Index, Small-Caps represented by the S&P SmallCap 600® Index. The S&P 500® Index is defined in our glossary. Past performance is no guarantee of future performance.

The Federal Reserve (Fed) has already cut rates by 175 basis points during this easing cycle, and more cuts may arrive in 2026. Keep in mind that the broader economic effects of rate cuts tend to show up six to 18 months after they occur.

We believe small-cap companies could benefit from the accelerated depreciation of capital expenditures allowed under the One Big Beautiful Bill Act (OBBB). We think this change will incentivize companies to invest in their supply chains, which is a significant driver of small-cap earnings growth.

Small-caps exposed to consumer spending may benefit from larger-than-normal tax refunds expected this tax season, another Easter egg from the OBBB.

Companies last year made nearly $3 trillion worth of pledges to invest in U.S. infrastructure and manufacturing, according to the White House. Even if a smaller fraction of these commitments materializes, the reshoring trend has an outsized upside for small-cap companies, as we’ve discussed before.

Companies are showing a greater appetite to go public or to acquire other companies. This type of capital markets activity has historically benefited small-caps.

U.S. manufacturing activity reported in early February showed the most expansion at any time over the last four years. We view this as an indicator that capital expenditures may accelerate.

From a valuation perspective, small-caps are less expensive than the rest of the U.S. stock market. The S&P SmallCap 600® Index is currently trading 15% below its historic average, offering a potentially attractive entry point to the asset class.2

We believe now may be a good time for investors, especially those concentrated in Mag 7 or artificial intelligence (AI)-related stocks, to consider diversifying into asset classes that show earnings acceleration and offer attractive valuations.

How Sector Dynamics Are Evolving for Small-Caps

Regional banks: These banks could benefit from lower interest rates, which tend to make borrowing more attractive. Analysts expect earnings to improve over the next two years, and bank balance sheets remain solid. Nonetheless, many investors have overlooked this sector or remain cautious about its prospects.

Energy: Small-cap energy companies have struggled with weak investor sentiment, but recent geopolitical tensions in the Middle East have refocused attention on global supply risks and energy security. While oil prices remain volatile, we believe peak oil demand is still at least a decade away. Importantly, today’s energy companies are better capitalized, more disciplined and trade at discounted valuations. Any sustained pickup in U.S. economic activity could position small-cap energy firms as meaningful beneficiaries.

Biotechnology: After four years of underperformance, we’re taking a closer look at the biotech industry. The clinical pipeline of new drugs and treatments currently under development is the strongest it’s been in years. Additionally, large pharmaceutical companies face a patent cliff — when the patents on their best-selling drugs expire, leading to decreased sales as generics enter the market. As a result, they will likely scour small-cap biotechnology firms to acquire their most promising innovations.

Industrials: The reshoring of manufacturing to the U.S. continues to gain momentum. This trend has mostly benefited small-cap companies whose services, especially in the industrials sector, support domestic manufacturing. For example, Construction Partners, a road construction and repair company, has mentioned that new factories are driving investments in access roads and the highway infrastructure to reach them. The company’s CEO said that boosted infrastructure spending for public and private projects provides a strong and steady tailwind in its key markets.

A Shifting Environment for Small-Cap Stocks

It has been a tough climate for small-cap stocks in recent years. But a confluence of factors — deregulation, new tax and accounting rules, reshoring and interest rates — has supported this beaten-down asset class since Liberation Day.

In our view, investors seeking a more diverse portfolio may benefit from the potentially more promising outlook for small-cap stocks.

Authors

Senior Investment Director

Explore Our Small-Cap Capabilities

Magnificent 7 (Mag 7) refers to seven stocks that have been high-performing in the technology sector — Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla.

Standard & Poor’s. Data as of 2/9/2026.

Historically, small- and/or mid-cap stocks have been more volatile than the stock of larger, more-established companies. Smaller companies may have limited resources, product lines and markets, and their securities may trade less frequently and in more limited volumes than the securities of larger companies.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.