Why Global Growth Investing Calls for Active Management

We believe a larger global investable universe places a premium on disciplined, active security selection.

Key Takeaways

Global equities span a wide range of markets, industries and economic drivers, creating meaningful dispersion in outcomes.

Index-based portfolios may continue adding to companies without reassessing fundamentals, valuations or earnings durability.

A disciplined, active process can compare companies across markets and allocate capital based on conviction rather than index weight.

Institutional investors have many ways to access global equities. In recent years, many have used passive strategies to achieve broad market exposure efficiently and at low cost. That trend is understandable, particularly in a category as broad and diverse as global equities.

At the same time, the case for a dedicated active global growth allocation remains compelling. In a global opportunity set, leadership shifts across regions, sectors and individual companies over time. These shifts aren’t always captured efficiently by benchmark-driven approaches.

It’s true that active management has fallen out of favor with some investors, particularly as market performance has become concentrated among a narrow group of companies. However, we believe active management remains a valuable investment strategy with the potential to deliver positive results over the longer term.

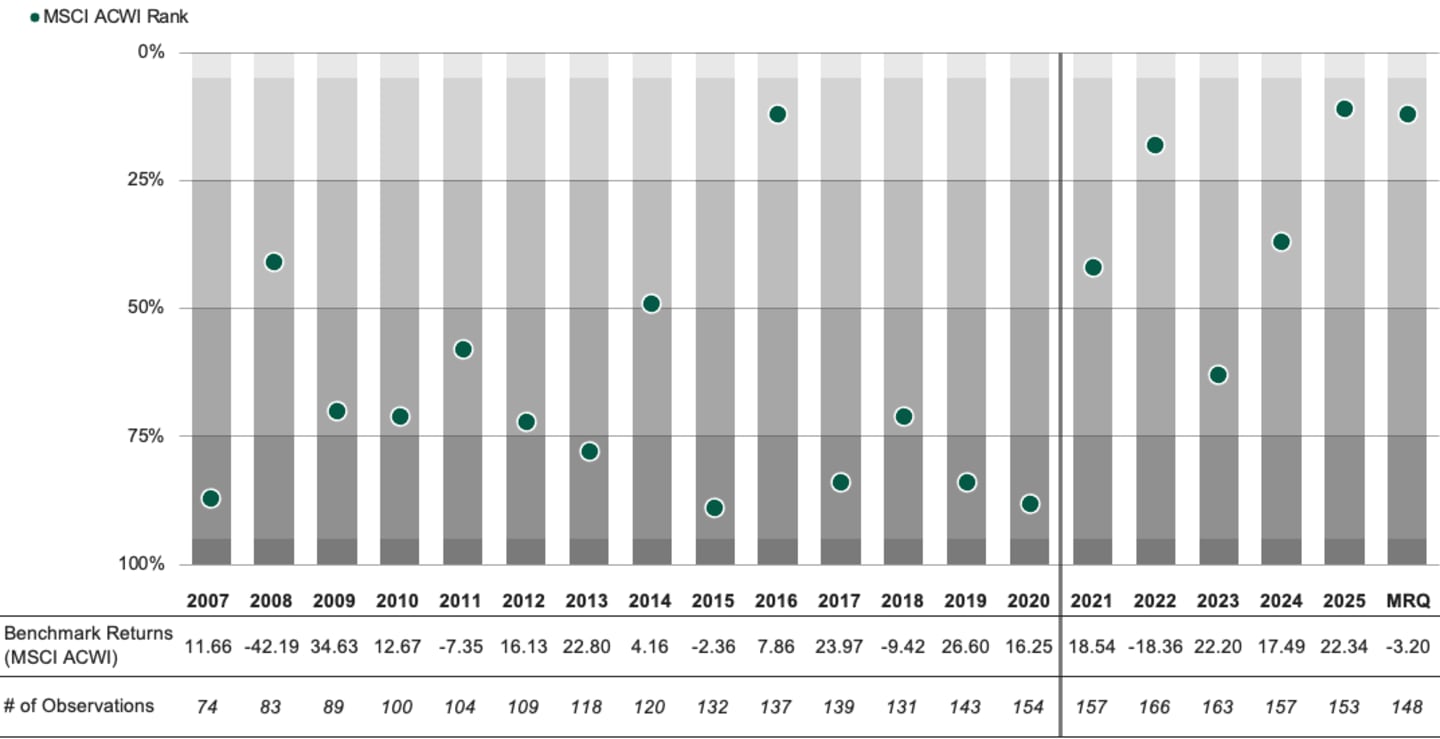

Figure 1 demonstrates how one index — the MSCI ACWI, a benchmark for global funds — has outperformed active management recently. If we take a longer view, however, we observe extended periods when the benchmark lagged the median manager.

Figure 1 | Active and Passive Management Trade Market Leadership

Data from 1/1/2007 – 3/31/2026. Source: eVestment. Benchmark returns are in U.S. dollars, gross of fees. MRQ denotes the Most Recent Quarter. Past performance is no guarantee of future results.

For investors seeking growth across global markets, the question isn’t simply whether to allocate actively or passively. It is whether their portfolio’s structure provides enough flexibility to identify emerging opportunities, respond to shifting fundamentals and manage the trade-offs inherent in cap-weighted benchmarks.

Why Does Global Growth Investing Create More Dispersion?

Global growth equities offer a broader and more diverse opportunity set than any single market. They span a wide range of countries, industries, business models and economic drivers. This breadth can improve diversification, but it also increases the range of possible outcomes across regions and companies.

Differences in economic cycles, policy environments, capital markets and consumer demand frequently lead to meaningful dispersion in both earnings growth and valuations. As a result, performance can vary significantly not only by region, but also by company within the same region or industry.

The depth and quality of information available to investors also vary across markets. Uneven analyst coverage and differing levels of market efficiency may contribute to pricing discrepancies, particularly in less widely followed segments of the global equity universe.

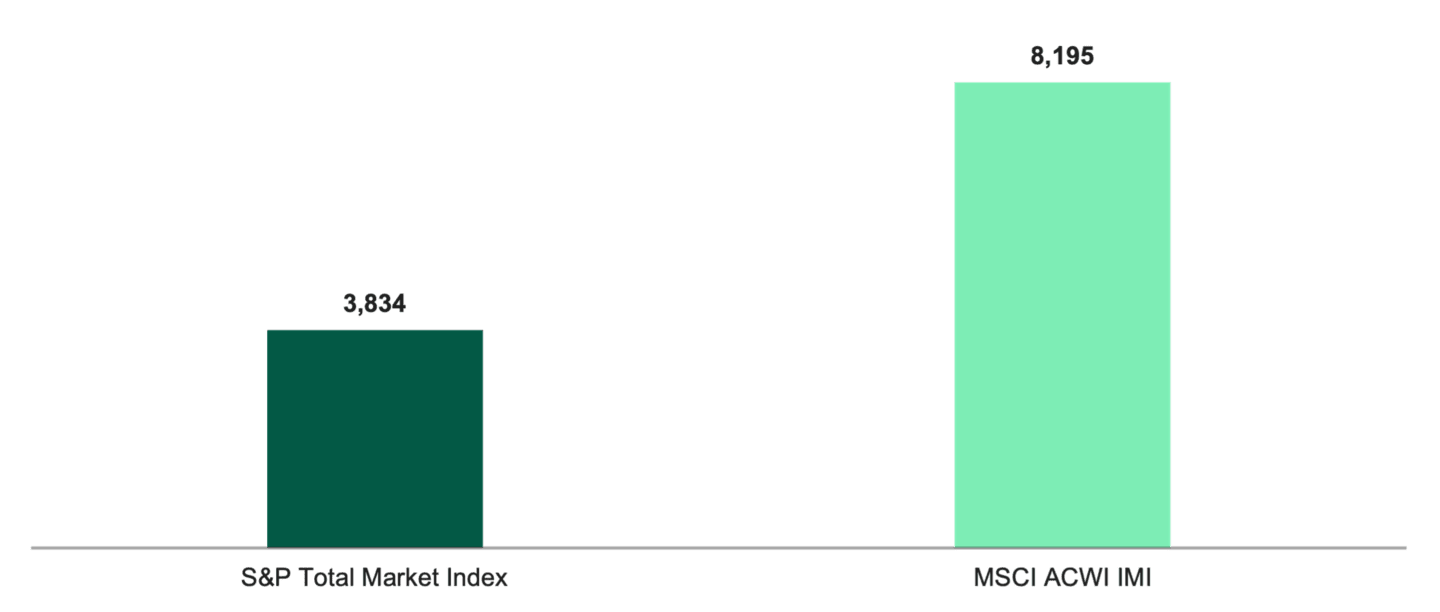

This breadth is one of the defining advantages of global investing, as shown in Figure 2. It also means that implementation matters. A larger universe offers more potential sources of return, but it also requires a disciplined process for consistently evaluating opportunities across markets.

Figure 2 | Global Equity Index Holds Twice the Companies of a U.S.-Only Index

Data as of 6/30/2026. Sources: S&P Global, MSCI.

What Are the Structural Trade-Offs of Passive Global Equity Exposure?

Passive strategies have traditionally played an important role in institutional portfolios. They can offer cost-efficient access to broad market segments and may simplify governance for allocators seeking benchmark-based exposure.

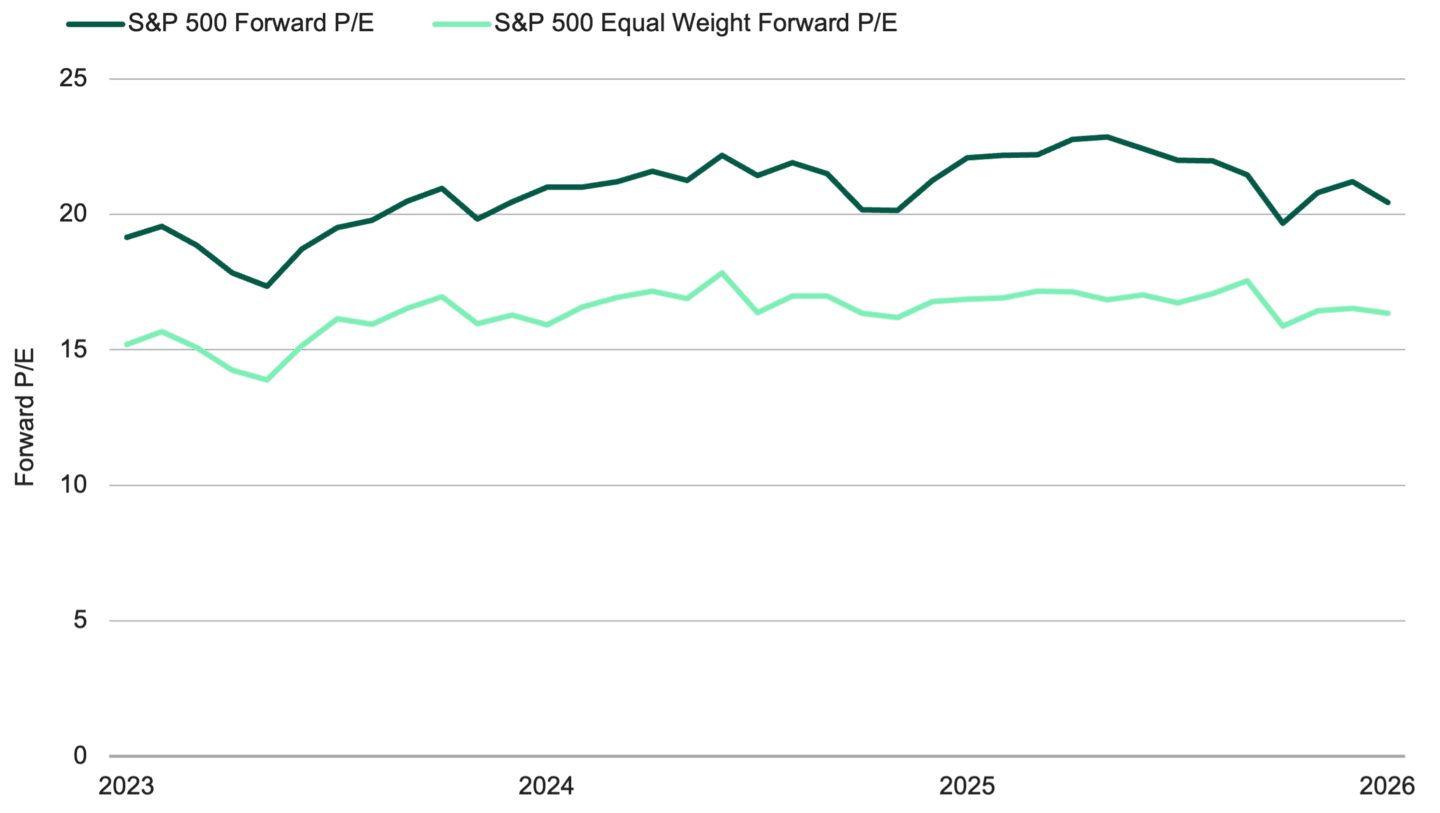

However, these strategies are shaped by the structure of the indices they track. Most follow market capitalization-weighted benchmarks, which allocate more capital to companies as their market values rise. That can lead to situations where the market-weighted index carries a valuation premium above its equal-weighted version. See Figure 3.

Figure 3 | Market-Weighted Indices Can Trade at a Premium

Data from 6/30/2023 - 6/30/2026. Source: FactSet.

While market prices reflect investor expectations, index construction doesn’t involve an explicit reassessment of whether a company’s fundamentals or valuation continue to justify its growing weight in the portfolio.

That distinction matters. In periods when market leadership narrows, cap-weighted benchmarks can become increasingly concentrated in a relatively small number of companies. Over the last five years, for example, the Magnificent Seven stocks have accounted for roughly 33% of MSCI ACWI performance.1 In the MSCI EM Index, just three stocks — TSMC, Samsung and SK Hynix — represent roughly 30% of the benchmark.2

Over time, this can result in a portfolio that is driven more by index mechanics than by an active view of earnings durability, valuation or business quality.

Index-based strategies can also be slower to adapt as conditions change. Benchmark composition evolves through scheduled reconstitutions, which means passive portfolios may be slower to incorporate emerging companies that are not yet fully represented in the index. At the same time, they may continue to hold companies whose fundamentals or earnings outlooks have deteriorated.

These features may be particularly relevant in a global context. Economic cycles, policy decisions and geopolitical developments don’t affect all regions, sectors or companies equally. When trade regimes shift, capital spending trends change, or political risks rise, the effects can be highly uneven across the global equity universe.

In those environments, passive portfolios continue to allocate primarily based on benchmark rules and market capitalization. That may preserve broad exposure, but it can also limit responsiveness when investors seek more selectivity.

How Can an Active Global Approach Add Value?

An active global growth strategy approaches the market differently. Rather than treating geography as a set of fixed buckets, it views global equities as a single, integrated opportunity set across markets.

This matters because many of the most attractive growth opportunities aren’t neatly aligned with index weights, regional classifications or incumbent market leadership. A bottom-up process allows investors to compare companies across markets on a consistent basis and allocate capital according to conviction rather than benchmark size.

Active global managers can also reassess holdings as conditions evolve. This includes assessing whether earnings trajectories remain intact, whether competitive advantages are strengthening or weakening, and whether valuation continues to support the investment case. In other words, active management can reevaluate positions in a way that index construction doesn’t.

This flexibility can be especially valuable during periods of rapid change. Technological innovations, shifts in public policy and changes in corporate investment cycles can alter company-level fundamentals before those changes are reflected in benchmark composition.

Consider the wave of investment tied to artificial intelligence (AI). It has created opportunities across semiconductors, infrastructure, software and related industries. It has also introduced risks tied to capital spending intensity, supply chains and the possibility of overinvestment.

An active manager can participate in those opportunities while calibrating exposure as the outlook evolves.

A More Integrated View of Portfolio Construction

Active global management isn’t only about security selection. It is also about seeing the portfolio as a whole.

When allocations are made region by region or country by country, it’s possible to make sound decisions within individual sleeves while still creating unintended concentrations at the total portfolio level. For example, separate decisions to add exposure in two different regions may each be justified on fundamental grounds. Yet together, they may result in an outsized position in a single sector or growth theme.

A global investment process can help address that problem by evaluating region, sector and company exposures simultaneously. It allows portfolio construction decisions to reflect the interaction between holdings, rather than assessing each segment in isolation.

That is particularly relevant in growth investing, where many of the most important drivers of return cut across borders. Supply chains, platform businesses, industrial automation, health care innovation and digital infrastructure aren’t confined to one region. Understanding these linkages can improve both idea generation and risk management.

For institutional investors, this more integrated approach may offer an important advantage. It can help ensure that position-level decisions align with overall portfolio objectives, rather than simply reflecting separate regional calls.

How Can an Active Growth Strategy Complement Passive Core Exposure?

For many institutions, the most practical role for an active global growth strategy isn’t as a wholesale replacement for passive exposure, but as a complement to it.

Passive strategies can continue to serve as efficient core holdings. A dedicated active global growth allocation can sit alongside that core, expanding the opportunity set beyond what benchmark-driven construction and timing allow. It can provide access to companies that may not yet be meaningfully represented in indices, while introducing greater selectivity around valuation, earnings quality and business durability.

This framing is often more consistent with how institutional portfolios are built. Many allocators already combine passive market exposure with active strategies that target differentiated sources of return. In that context, a global growth sleeve can play a specific role: providing a benchmark-aware yet more selective expression of growth exposure.

For institutions seeking a stand-alone active global equity allocation, the case can also be compelling. A single strategy with a disciplined process and a broad global remit may provide a more cohesive way to access growth opportunities across markets than a collection of regional exposures managed in isolation.

What Defines a Disciplined Global Growth Process?

Global growth investing isn’t simply about owning more companies in more places. It’s about making informed decisions across a broader and more uneven opportunity set.

We believe this requires research, judgment and an investment framework that can distinguish between durable growth and temporary enthusiasm. It also requires the flexibility to adjust when valuations become stretched, when fundamentals inflect, or when market leadership changes.

Passive strategies remain useful tools for broad market access. But in our view, a disciplined, active global growth approach can offer meaningful advantages in a category defined by breadth, dispersion and change.

For investors building global equity exposure today, that distinction may matter more than ever.

Authors

Senior Portfolio Manager

Senior Client Portfolio Manager

Explore Our Global Growth Equity Capabilities

MSCI ACWI, as of 6/30/2026.

MSCI Emerging Markets Index, as of 5/29/2026.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

Diversification does not assure a profit nor does it protect against loss of principal.

Historically, small- and/or mid-cap stocks have been more volatile than the stock of larger, more-established companies. Smaller companies may have limited resources, product lines and markets, and their securities may trade less frequently and in more limited volumes than the securities of larger companies.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.