From the Cloud to Chips: Inside Big Tech’s AI Spending Surge

AI infrastructure spending is at an all-time high, with potential payoffs varying widely across companies.

Key Takeaways

Companies are investing heavily in AI buildout, but some investors doubt revenue growth can justify the massive spending.

Key differentiators among these companies include spending as a percentage of free cash flow and revenue, as well as balance sheet health.

It’s not just one big “AI trade." Leading companies have end-to-end AI exposure, from chips to models, from the cloud to the customer interface.

Unprecedented AI CapEx

The Manhattan Project, the moon landing, the internet and the transcontinental railroad were landmark infrastructure projects. By comparison, capital expenditures (CapEx) on artificial intelligence (AI) may exceed them all.1

Companies are funding the buildout with their own cash, debt markets and private equity financing. For investors, this matters because spending at this scale threatens corporate profits and balance sheets.

The key question is simple: Will this spending generate enough growth to justify the cost?

Which Hyperscalers Are Driving AI CapEx Spending?

The largest spenders are hyperscalers, cloud computing companies operating at a very large scale. For our context, this includes AI cloud providers such as Alphabet, Amazon.com, Microsoft and Oracle.

Meta Platforms doesn’t offer cloud services. But its massive internal AI infrastructure, AI models, and, above all, its AI CapEx spend, put it squarely alongside the hyperscalers for our analysis.

Finally, we’ve added CoreWeave and Nebius Group. They are “neo-cloud” companies mainly functioning as AI factories, with little differentiation or specialization. In contrast, hyperscalers have deep cloud expertise and can create custom networking solutions and chips.

The neo-cloud companies also differ in balance sheet quality. That’s because the hyperscalers and Meta have exceptionally strong cash flows to fund their AI buildouts. By contrast, CoreWeave and Nebius are funding their investments with debt because they lack other underlying businesses to lean on.

These exist because cloud providers alone can’t fully meet the growing demand for computing power driven by AI. This relentless need for computing resources explains the seemingly endless CapEx spending.

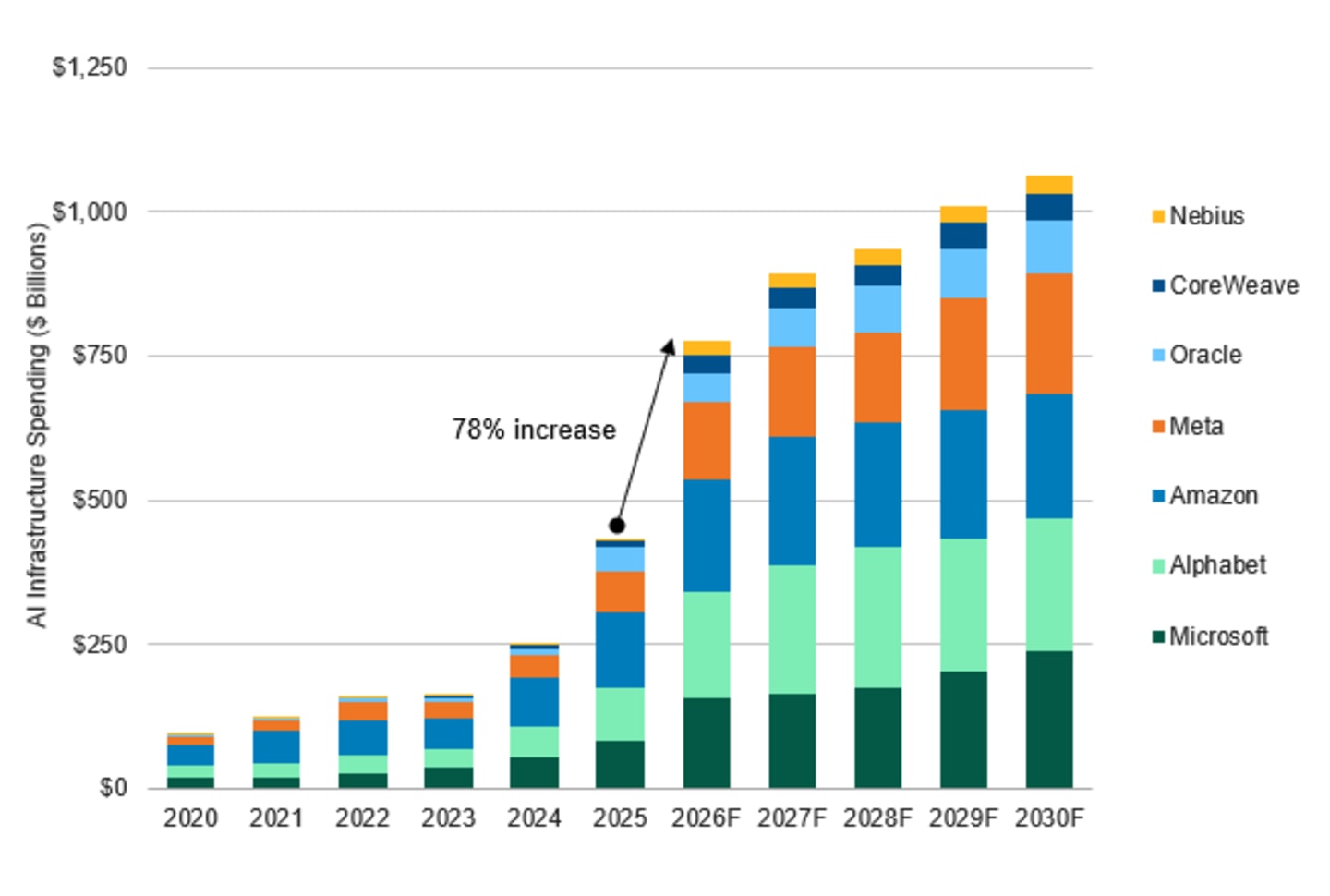

As of May 2026, we estimate that these seven companies will spend approximately $775 billion on AI CapEx for the full year, an increase of 78% versus 2025. (See Figure 1.) Figure 1 also shows that CapEx spending has accelerated since 2023, though growth rates are expected to slow.

Figure 1 | Staggering CapEx for the Foreseeable Future, but Rate of Growth Expected to Slow

Data from 1/1/2020 – 5/22/2026. Forecasts for 2026-2030 as of 5/22/2026. Source: American Century Investment Management analysis. Forecasts based on FactSet data. Forecasts are not reliable indicators of future performance.

Lessons from Previous Tech CapEx Cycles

This level of spending is unprecedented; however, we can learn from past CapEx cycles.

Alphabet essentially doubled its annual CapEx budget from 2017 to 2018. It did so to acquire the chips and the data centers to support the buildout of its Google Cloud business.

The past, as the saying goes, doesn’t repeat, but it rhymes. A $13 billion to $25 billion increase in CapEx spending in 2018 isn’t the same as a $91 billion to $180 billion increase in 2026.

Nonetheless, the context is instructive. Building data center capacity is expensive, requiring investment today to support business tomorrow. And it’s useful to point to a payoff from a similar doubling of CapEx by the same management team over the past decade.

Now let’s consider a counterexample. Meta rebranded from its social media platform, Facebook, to Meta Platforms in 2021. At the same time, two things happened.

First, Meta increased its CapEx budget by two-thirds from 2021 to 2022. Second, the company experienced a significant slowdown in its advertising business.

In that environment, the company generated nearly $30 billion in profit in 2022, but earnings per share were down by almost 40% over the prior year.2

Meta’s experience illustrates the dual dynamic we want to emphasize: Investors will tolerate rising CapEx when they see a credible path to revenue growth. But when spending rises as the core business weakens, that support can quickly disappear. This is what happened at Meta — its stock fell about 75% from peak to trough between late 2021 and late 2022.

The broader point is this: Large technology investments require large revenue prospects to win investor support. When that support fades, stock prices can fall sharply.

Does Revenue Growth Support Today’s AI CapEx?

In the early days of the current AI CapEx cycle, companies were rewarded for spending to accelerate cloud growth. Microsoft, Alphabet and Oracle are good examples of this, as their stocks initially surged after announcing huge CapEx outlays. Nebius and CoreWeave — both of which debuted on the stock market in late 2024 and early 2025, respectively — also saw strong demand for their shares, based on massive CapEx spending plans.

But beginning in late 2025, the market’s attitude appeared to shift. Investors now seem more concerned about the level of CapEx than they are impressed by the acceleration. Oracle’s stock decline from September 2025 through early April 2026 is a clear example of this changing investor view.

You can also see this dynamic at work in the market's reaction to first-quarter 2026 earnings reports. Meta grew revenues by a third year over year, but it also added another $10 billion to $20 billion to its CapEx plans. The stock fell. A year or two ago, investors would likely have cheered these numbers.

Meanwhile, Alphabet boosted its 2026 AI CapEx forecast by $10 billion, raising it from $180 billion to $190 billion. Amazon reaffirmed its earlier $200 billion spending plan. During the same period, Alphabet’s cloud revenue grew by 60% year over year through March 31, and its backlog doubled. The stock price surged.

Similarly, Amazon’s cloud business enjoyed its best growth in years during the first quarter, prompting numerous analyst upgrades and a rise in its stock price.

For Alphabet and Amazon, the spending directly supports their rapidly expanding cloud businesses. Meta’s revenue growth, however, was slower, and the company doesn’t have a cloud component.

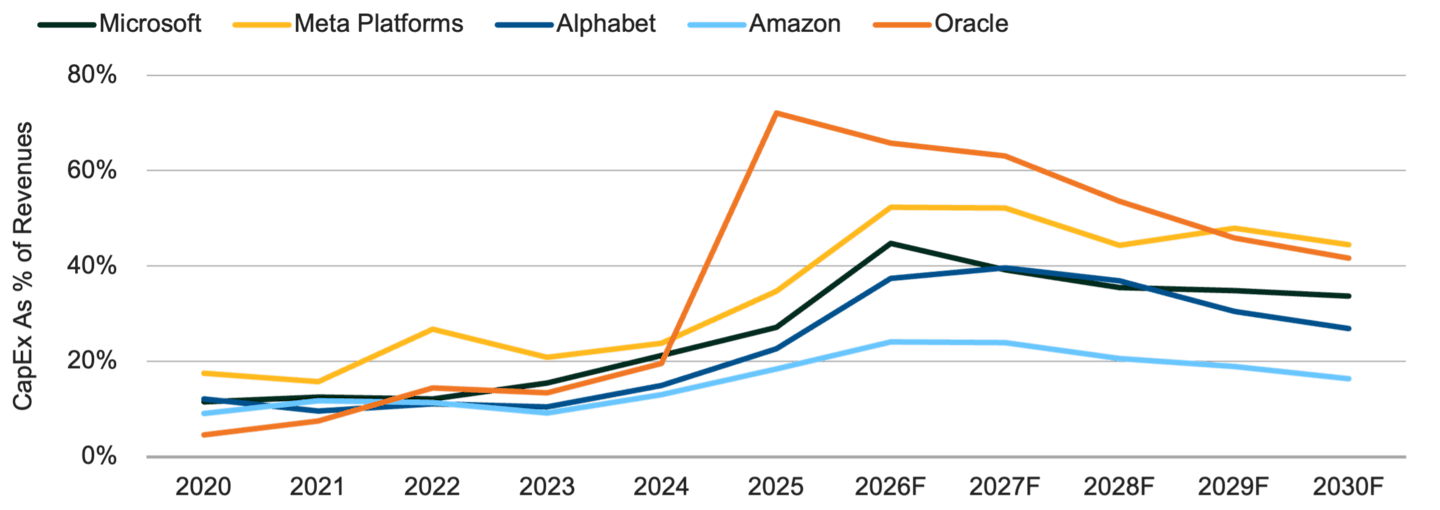

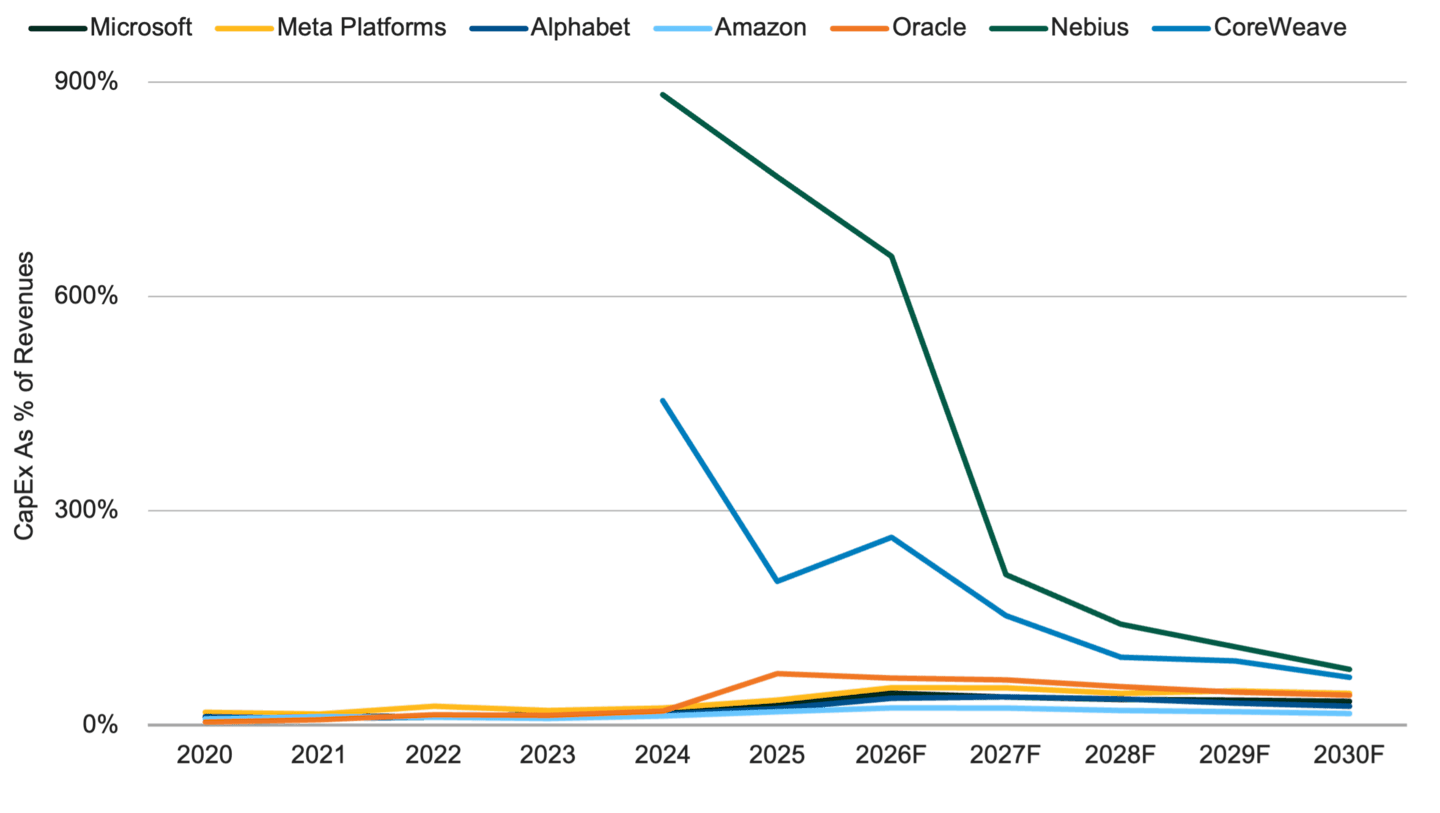

Now look at Figure 2, Panels A and B. These show CapEx spend relative to revenue generation from an historical perspective for the biggest players. This is a useful way to think about the sustainability and desirability of current AI CapEx spend.

Figure 2 | CapEx as a Proportion of Revenues Varies Greatly by Company

Data from 1/1/2020 – 5/22/2026. Forecasts for 2026-2030 as of 5/22/2026. Source: American Century Investment Management analysis. Forecasts based on FactSet data. Forecasts are not reliable indicators of future performance.

This chart also does a good job showing just how different the spend for each company. Alphabet and Amazon, for example, show only modest increases in the intensity of spending since 2023. At the other end of the spectrum, Panel B shows just how extreme the spending commitment as a percentage of revenue for Nebius and CoreWeave relative to the true hyperscalers.

How AI Spending Exposure Differs by Company

This brings us to company-specific perspectives on current AI risks and opportunities.

Alphabet (GOOG)

Alphabet is arguably the most compelling story among the hyperscalers today due to its AI-specific chips, a leading AI model (Gemini), a global cloud platform, and a massive product footprint in search, YouTube and advertising.

Crucially, its core advertising business is already benefiting from AI implementation, driving strong revenue growth. This “full-stack” positioning helps explain why investors remain more forgiving of its spending.

Amazon.com (AMZN)

Amazon, too, is in a strong competitive position. It produces its own AI Trainium chips and employs a sophisticated hybrid AI model. It has also integrated its own AI models into internal processes and product offerings, boosting financial results. Furthermore, Amazon Web Services (AWS) is the top cloud provider globally and is expanding quickly.

Meta (META)

Meta’s role is that of a giant AI consumer. Its own models lag behind those of its well-known competitors, though relative model rankings can change rapidly. In addition, the company lacks its own chips and cloud services. However, Meta has very successfully used AI to improve the quality of its product offerings, significantly boosting revenues.

Nevertheless, its experience with the metaverse may offer a potential roadmap for hyperscalers. When Meta committed to rationalizing spending after its foray into the metaverse, the stock re-rated sharply higher. Past performance can’t dictate future results, but a return to CapEx discipline could be beneficial.

Microsoft (MSFT)

In our view, Microsoft is in a relatively uncomfortable strategic position. It’s spending aggressively on AI infrastructure with uncertain near-term returns, lacks a fully owned leading model, and remains deeply tied to OpenAI through a complex partnership.

If its AI investments fail to deliver rapid growth, Microsoft will appear to have overspent. If AI succeeds spectacularly, it risks accelerating the disruption of its high-margin Microsoft Office franchise. This dynamic helps explain why investors remain cautious despite accelerating cloud growth.

Oracle (ORCL)

Oracle has unexpectedly become a beneficiary of AI infrastructure, securing deals between hyperscalers and attracting large commitments from OpenAI.

Oracle’s challenge has been to convince investors it has sufficient funding to achieve its lofty goals. This overhang is now lifting. Oracle laid out a clear financing plan of $45 billion to $50 billion through 2026, split roughly evenly between debt and equity, with minimal dilution to existing shareholders. With capital allocation questions increasingly resolved, investors have shifted their focus to Oracle’s execution and cloud share gains.

CoreWeave and Nebius

These two companies recently completed initial public offerings, raising capital to support their data center builds. But their financing needs are so demanding that they have borrowed heavily to acquire cutting-edge AI chips.

Reports that financing fell through for a $4 billion CoreWeave data center underscore how sensitive the ecosystem is to capital availability. Unlike the true hyperscalers, these companies lack revenue diversification and balance-sheet resilience.

AI Isn’t “All One Trade”

The media often claims that “AI is all one trade,” but we believe this is far from accurate. While AI CapEx is so substantial that it impacts the entire stock market and the broader U.S. economy, we have highlighted the distinct risk exposures, as well as the strengths and weaknesses, of the companies engaged in this trade.

At a high level, the gap between AI cloud spending and revenue growth has become uncomfortably wide for many investors. The industry appears headed for a binary outcome: Either AI usage scales profitably and justifies today’s investment, or CapEx must be meaningfully reduced.

The true hyperscalers may emerge stronger either way. In the event of a retrenchment in spending, they would still own the latest chips and AI infrastructure, along with their other lines of business. But even within this group, their competitive positions vary widely.

Elsewhere, we believe a real risk lies with the neo-cloud providers and with those whose survival depends on this extraordinary spending cycle continuing unabated.

In our view, this underscores the importance of deep, fundamental research on a company-by-company basis. Companies in the same industry serving the same market can have very different prospects for success. And with an unprecedented amount of capital at work, the stakes have never been higher.

Authors

Senior Investment Analyst

Investment Analyst

Client Portfolio Manager

Explore Our Large-Cap Growth Capabilities

Meghan Bobrowsky, Drew An-Pham, and Alana Pipe, “Big Tech’s AI Push Is Costing a Lot More Than the Moon Landing,” Wall Street Journal, February 7, 2026.

PR Newswire, “Meta Reports Fourth Quarter and Full Year 2022 Results,” February 1, 2023.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.