Why Value, and Why Now?

Value stocks have outperformed growth stocks so far in 2025. Here’s why we think value stocks could be compelling in a turbulent market environment.

Key Takeaways

After two years of underperformance, value stocks are leading the market amid economic worries and a rotation away from mega-cap technology stocks.

We believe the valuation gap between value and growth stocks favors value and is important to consider during market volatility.

Given their high valuations, growth stocks may have limited upside price potential. Therefore, we expect dividends to play a crucial role in total returns.

The market is shifting after two years of dominance by the Magnificent Seven, technology stocks fueled by enthusiasm for artificial intelligence (AI). This rotation may favor value stocks.

The Trump administration’s aggressive tariff policy led to a significant decline in stock prices in April, causing the S&P 500® Index to fall into correction territory after a prolonged bull market. This downturn occurred during a period of increased market volatility driven by uncertainty surrounding policy and concerns about substantial investments in AI.

This year, through April 30, the Russell 1000 Value Index has outperformed the Russell 1000 Growth Index. We believe investors can navigate today’s choppy market by maintaining and potentially increasing exposure to value stocks.

Why Value Stocks Are Gaining Attention in 2025

1. Attractive Valuations

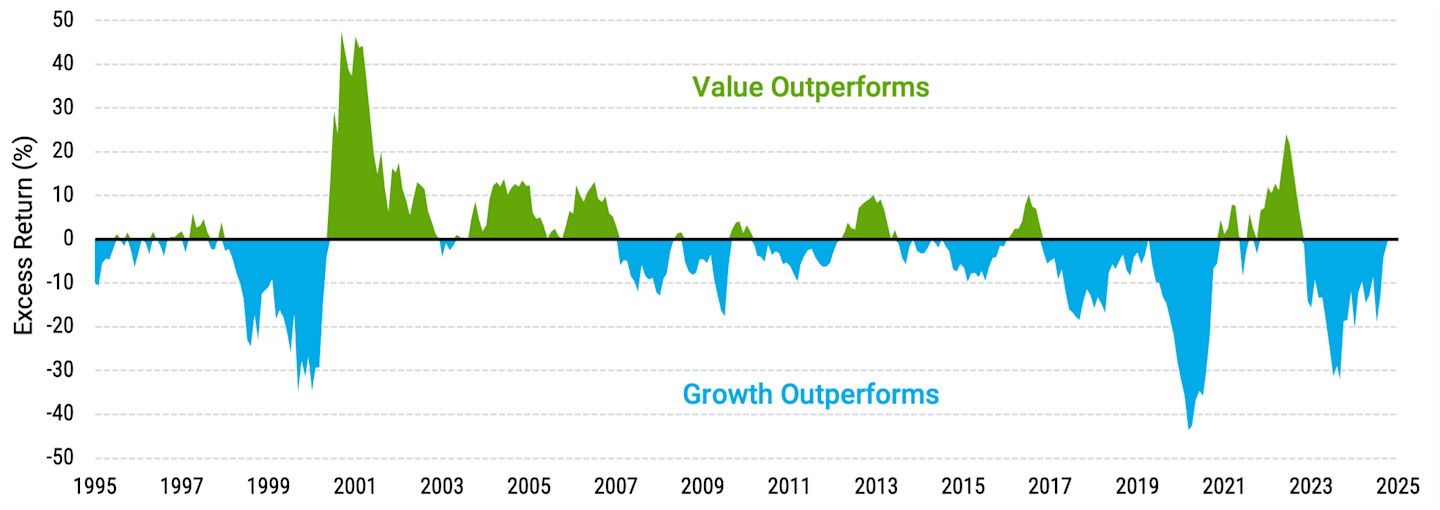

Value stocks have largely underperformed growth stocks since the Great Financial Crisis. As shown in Figure 1 Panel A, the duration and degree of value underperformance are significant, particularly during 2023-2024. This has created a disparity in valuations between value and growth that hasn’t been seen since the late 1990s and early 2000s tech bubble.

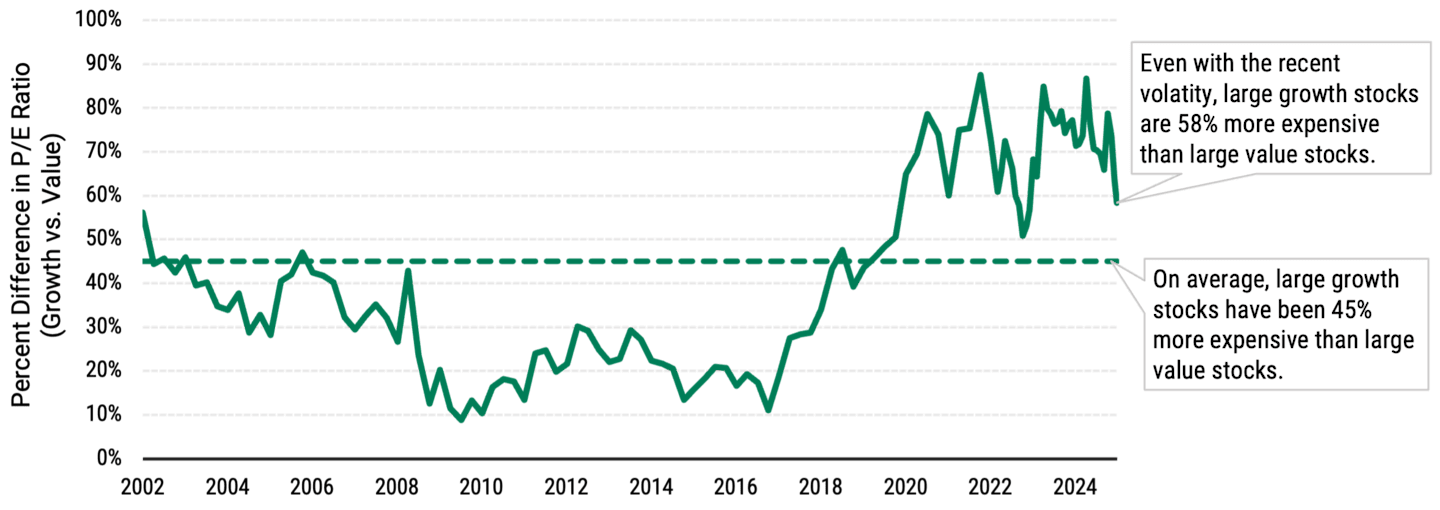

As Figure 1 Panel B shows, there’s still a wide gap in valuations between growth and value stocks. For investors whose equity portfolios have grown overweight in growth stocks, this has created a potentially attractive entry point to rebalance by increasing their value holdings.

Figure 1 | Value Stocks Have Been Significantly Less Expensive Than Their Growth Counterparts

Data from 6/30/1995 - 3/31/2025. Source: FactSet. Returns are in USD and represent the Russell 1000® Value Index vs. Russell 1000® Growth Index. Past performance is no guarantee of future results.

Data from 3/28/2002 - 3/31/2025. Source: FactSet. Past performance is no guarantee of future results.

The valuation gap between value and growth has grown to near 20-year highs, although the spread narrowed somewhat in April as investors fled to value stocks during the market sell-off triggered by Trump’s tariff policies.

We believe valuations, coupled with risk aversion due to the uncertainty and volatility of the current environment, are a potential catalyst for value to come back in favor.

Valuation alone isn’t the only factor we consider when making investment decisions. We go deeper to find companies that we think are high quality because they have historically generated higher and more stable returns on capital, have lower levels of leverage and possess durable business models.

We favor these high-quality companies because they have tended to be less susceptible to market fluctuations, particularly during volatile periods like the current economic environment.

2. Dividend Contributions

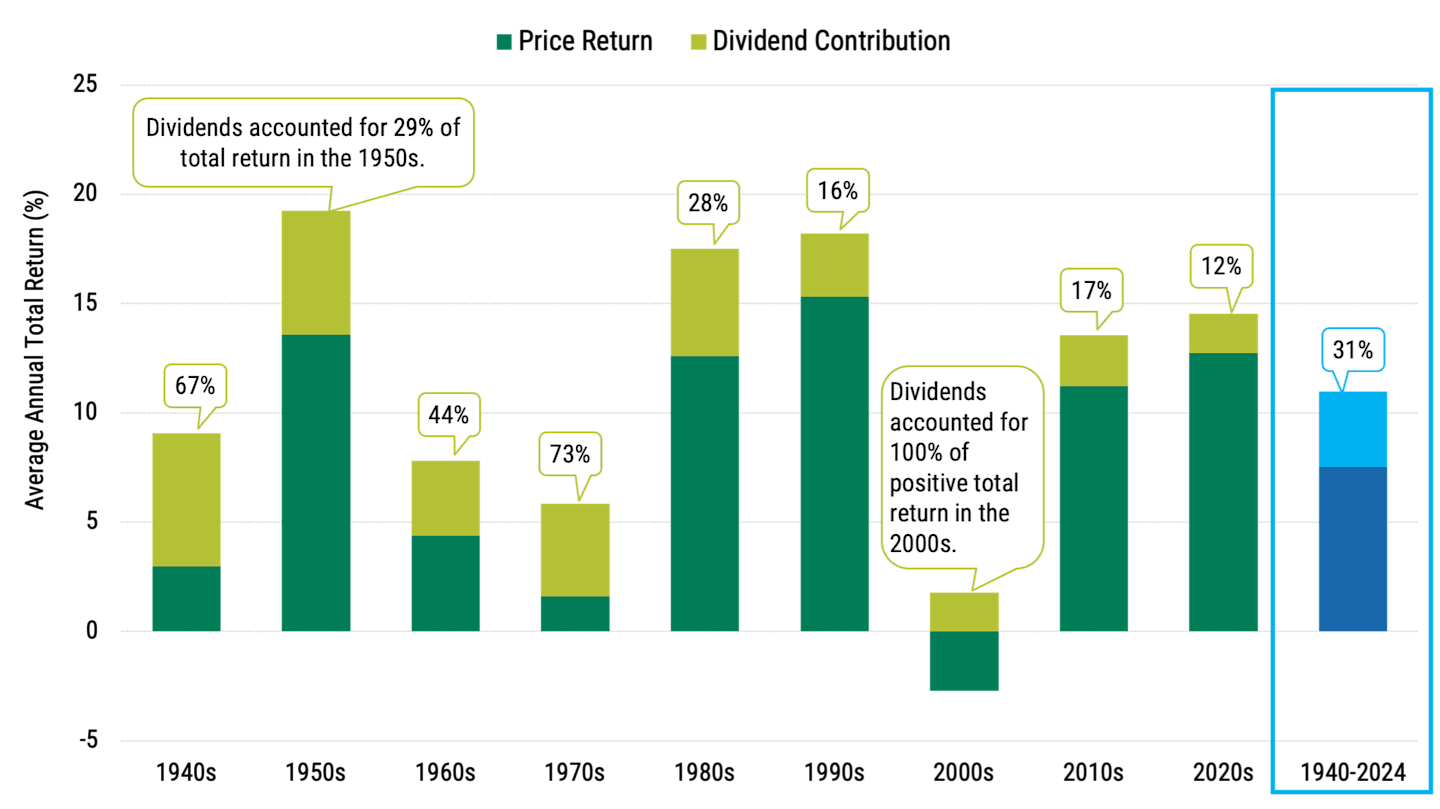

As Figure 2 shows, dividends have represented 31% of S&P 500® Index total returns over the last 80 years.

Figure 2 | Dividends Have Represented a Large Portion of the S&P 500’s Total Returns

Data from 1/1/1940 - 12/31/2024. Source: Morningstar.

During decades of lower price returns, such as the inflation-soaked 1970s when interest rates surged or the early 2000s after the tech bubble burst, dividends helped offset weakness and manage risk when price returns were stagnant or negative. As the chart illustrates, dividends made up most or all of the market’s returns during these periods.

During periods of market turbulence, when price appreciation is in question, dividends may offer investors a potential return on their investment. Value stocks have tended to be a more significant source of dividends than their growth counterparts.

Continued uncertainty about the path of inflation and the Federal Reserve’s decision-making on interest rates could result in a higher cost of capital. This, along with already high valuations, could diminish future price returns. As a result, we believe sustainable dividend income may be vital in the effort to achieving consistent returns.

3. Defense Wins Championships

Downside protection can help manage risk and build wealth over time, particularly during periods of market upheaval.

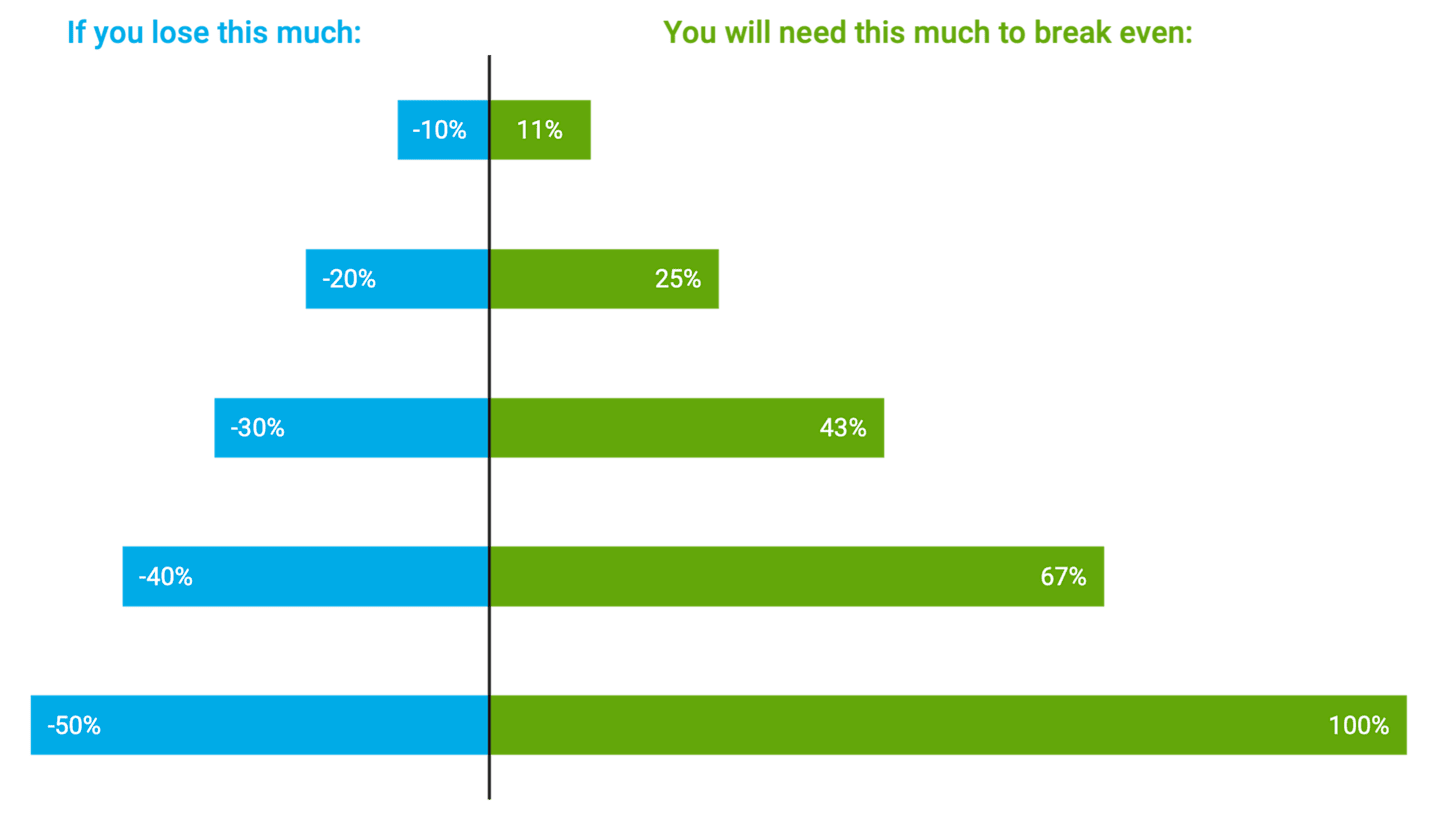

Consider the unforgiving nature of investment losses: A 10% loss requires an 11% gain to break even, and a 50% loss requires a 100% gain to break even. See Figure 3. Given the performance required to overcome a significant loss, we think limiting these losses in the first place is sensible.

Figure 3 | The Cruel Math of Losses

Source: American Century Investments. The relationship between an investment loss and the required gain to recover isn’t linear. For example, a 20% loss requires a 25% gain. Calculating it would be [1/(1-0.20)] - 1 = 0.25 or 25%.

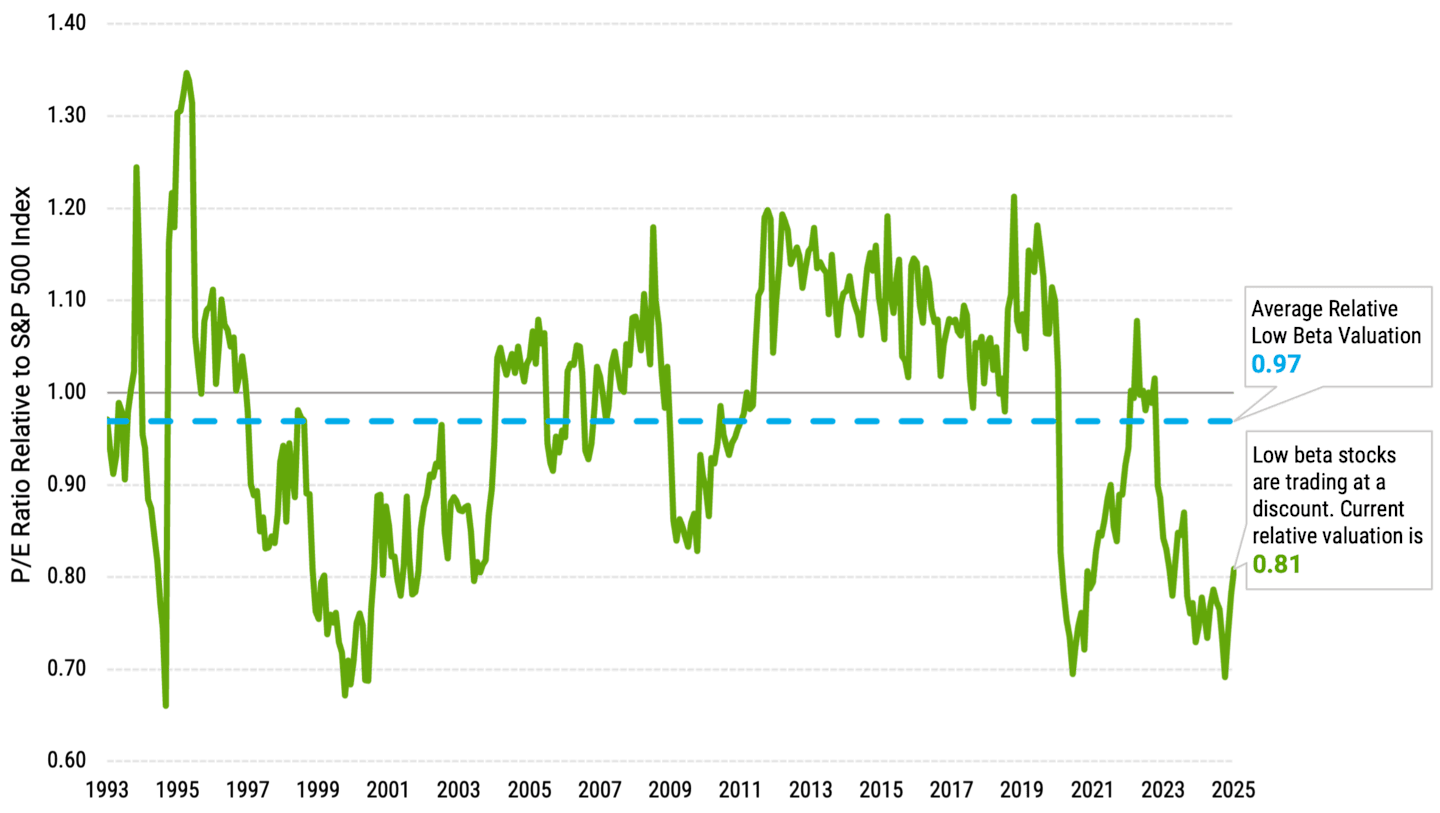

As value investors, we tend to find stocks in sectors like consumer staples and utilities that have offered downside protection and dividends during volatile and recessionary periods. While companies in these sectors may not be flashy, many offer stable business models and are less sensitive to economic fluctuations. And they’re often cheap. As Figure 4 shows, low-beta stocks, or stocks that don’t move much or differ from broader stock market movements, are trading at a discount.

Figure 4 | Stocks That Exhibit Less Volatility Have Traded at a Discount

Data from 3/31/1993 - 3/31/2025. Source: FactSet. Market is represented by the S&P 500 Index. Past performance is no guarantee of future results.

Given the elevated risks in today’s market, we find these characteristics attractive. Interest rates, inflation, tariffs and increasing caution about investments in AI represent several risks investors face.

After an extended bull market, investors and economists are worrying about the possibility of a recession. We believe defensive holdings and lower volatility will likely be critical to navigating this challenging environment.

4. History and Academic Research

Nobel Prize-winning research from Eugene Fama and Kenneth French proved that value stocks have historically outperformed and created more wealth over time than growth stocks. Additionally, academic research shows that quality securities outperformed the market over time. We find the combination of quality and value to be remarkably powerful.1

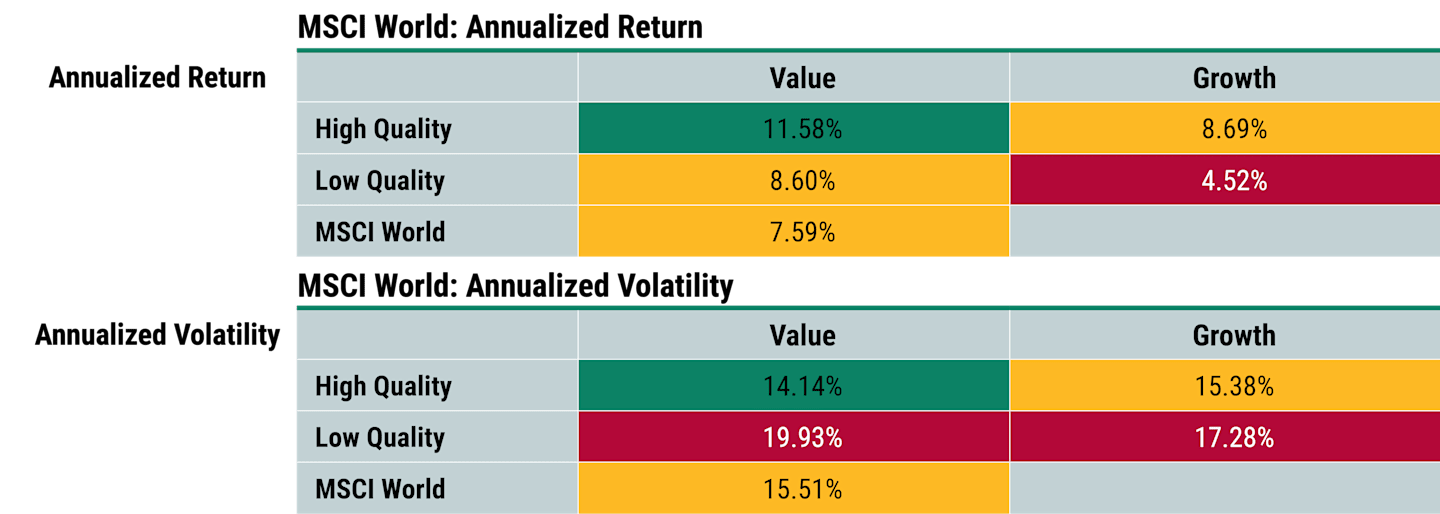

For nearly 30 years, even including the decade of growth’s dominance, high-quality value has been the style with the highest returns and the lowest risk, as Figure 5 shows.

Empirical evidence shows that quality has been one of the best-performing factors in growth and value during recessions and stagflation.

Figure 5 | High-Quality Value Has Outperformed with Lower Risk

Data from 1/1/1996 - 12/31/2024. Source: American Century Investments, FactSet. Universe: MSCI World Index. Past performance is no guarantee of future results.

Why Value Stocks Are Crucial During Market Volatility

Value stocks have played second fiddle to growth stocks for the last two years, so recent investor skepticism of the asset class is understandable. However, if investors think about the optimism of the stock market coming into 2025 and the volatility that has transpired due to unforeseen events, a diversified portfolio that considers value stocks could offset some of the effects of market turbulence.

Authors

Senior Client Portfolio Manager

Explore Our Global Value Capabilities

Jean-Philippe Bouchard, Stefano Ciliberti, and Augustin Landier, et al., “The Excess Returns of ‘Quality’ Stocks: A Behavioral Anomaly,” HEC Paris Research Paper No. FIN-2016-1134, February 11, 2016. Available at SSRN.

Past performance is no guarantee of future results. Investment returns will fluctuate and it is possible to lose money.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

Diversification does not assure a profit nor does it protect against loss of principal.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.

No offer of any security is made hereby. This material is provided for informational purposes only and does not constitute a recommendation of any investment strategy or product described herein. This material is directed to professional/institutional clients only and should not be relied upon by retail investors or the public. The content of this document has not been reviewed by any regulatory authority.