Navigating Turbulence: The Airline Industry’s Resurgence

Jet makers scramble to meet order backlogs amid pandemic fallout.

Key Takeaways

The post-pandemic air travel rebound is fueling backlogs for new aircraft.

Global middle-class growth is set to drive increased air travel demand, indicating sustained high aircraft production levels beyond existing backlogs.

Aircraft manufacturers depend on diverse suppliers for materials, systems and crucial parts for initial construction and ongoing maintenance.

The pandemic turned the global air travel industry upside down.

Business shutdowns and border closures worldwide severely restricted air travel, and outright fear of the coronavirus further slashed passenger traffic. Even before the pandemic, manufacturing giants Boeing and Airbus couldn’t keep up with the demand for new jets. They fell further behind amid supply-chain disruptions that dragged on for months.

Four years later, supply chain pressures have eased, and the rebound in global air travel has spurred renewed demand for aircraft. Consequently, jet manufacturers still trying to fulfill pre-pandemic orders face even more significant production challenges.

Backlogs and Challenges in Aircraft Production

Worldwide passenger traffic fell by two-thirds in 2020 as the pandemic decimated air travel.1 The U.S. government provided billions of dollars in grants and loan guarantees to keep airlines afloat.2 Nevertheless, the airlines amassed $180 billion of debt in one year as their collective revenue plunged 40%. Meanwhile, aircraft lease rates fell by a third — even more in some cases.3

The industry’s pandemic-era landscape marked a stark departure from earlier years when strong travel demand and cheap financing buoyed airlines’ demand for new aircraft. When the pandemic hit, Boeing and Airbus faced a combined $800 billion backlog of orders. The ensuing breakdown in global supply chains only exacerbated production delays, and backlogs mounted even more as new orders increased.4

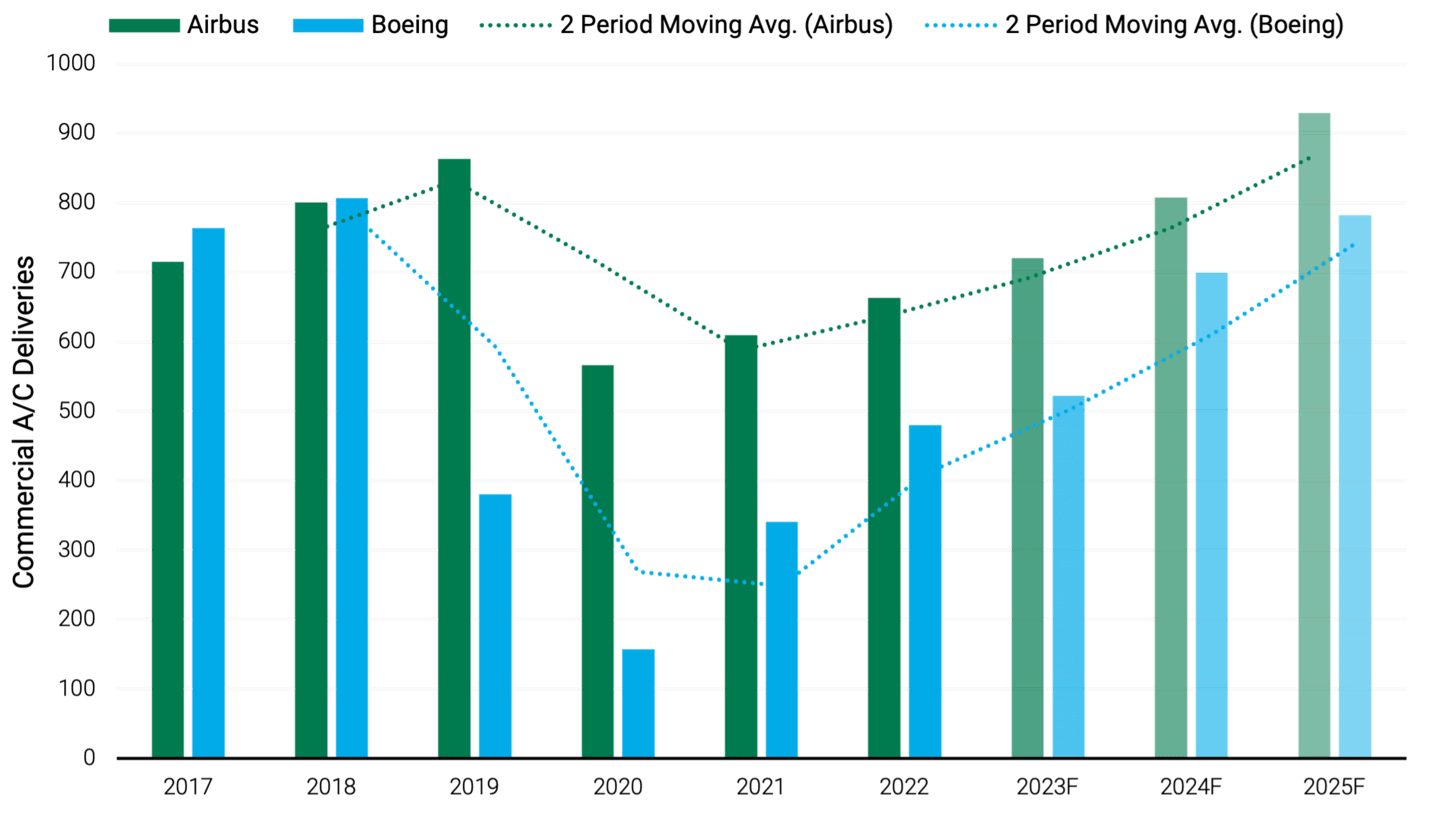

Today, the two aircraft behemoths have production schedules booked into the 2030s. In October 2023, Airbus said its order book totaled 8,000 airplanes, which it estimates will take 11 years to fulfill.5 Both companies have aggressively accelerated production to increase deliveries to airlines. See Figure 1. They have also indicated they don’t plan changes to their product lineups, prioritizing meeting existing demand instead.

However, additional demand beckons. Airline industry seat capacity has declined to pre-pandemic levels, even as passenger traffic has surpassed pre-pandemic demand. Business travel has recovered more slowly, but a Morgan Stanley survey shows corporate travel budgets will likely rise by 8% in 2024 after an 11% increase last year, finally exceeding pre-pandemic spending.6

Furthermore, airlines are attracted to new planes because the latest models can lower fuel costs by 15%-20% compared to older aircraft. This translates to significant savings on a considerable expense that can account for up to a quarter of airlines’ operating costs.7

Looking ahead, the growth in the middle class worldwide, especially in emerging markets, will likely underpin additional passenger demand. The International Air Transport Association estimates current demand for air travel will double by 2040. If so, Boeing and Airbus must sustain ramped-up production long after they work through their current orders.

Figure 1 | Aircraft Production Is Accelerating

Data from 1/1/2017 – 10/31/2023. Source: FactSet. Data for 2023 – 2025 are projections.

Aerospace Suppliers Play Critical Roles in New Aircraft Ramp-Up

Aircraft manufacturers’ ability to meet the ramp-up challenge relies on a top-performing supply chain for parts and components, including companies in the metal forging market. Key players in this space include Pennsylvania-based Howmet Aerospace, Russia-based VSMPO-AVISMA and Oregon-based Precision Castparts.

VSMPO-AVISMA was the primary supplier of titanium to the aerospace industry until the Russia-Ukraine war. However, economic sanctions brought by NATO and its allies against Russia forced the company to stop all exports to the U.S. and Western Europe. These sanctions have led to what investment analysts deem a secular loss in market share to Howmet.

Meanwhile, Precision Castparts Corp. has had production challenges after aggressive pandemic layoffs.8

Case Study: Why We Think Howmet Aerospace Is a Firm Worth Watching

Howmet’s heritage dates to 1886, when Charles Martin Hull developed the modern process for producing aluminum. Hull founded Alcoa Corp. two years later, which grew exponentially for the next 130 years. Alcoa spun off Arconic, a maker of engineered metal products, in 2016. Howmet Aerospace was formed due to Arconic’s 2020 split into two firms.9

Howmet operates through four segments: engine products, fastening systems, engineered structures and forged wheels. Its primary business makes components used in aircraft engines. In addition, it produces titanium ingots, forged nickel and aluminum alloys and components and assemblies for aerospace and defense applications. Furthermore, its forged aluminum wheels unit supplies the heavy truck and commercial transportation sectors.10

According to Howmet, buyers in the commercial aerospace industry compose more than half of the company’s sales, and defense contractors provide an additional 20%-25%. Howmet’s biggest customers include jet engine makers General Electric, Pratt & Whitney and Rolls-Royce. It’s also a key supplier to Safran, the second-largest global producer of aircraft landing gear, wheels and brakes.

These Howmet customers are vital to helping Boeing and Airbus address their backlogs. In turn, they’ll require accelerated parts deliveries from Howmet to keep pace with their engine and equipment production.

Anticipated production levels over the next several years have necessitated long-term supply agreements. Such agreements account for 60%-90% of annual revenue in the company’s respective aerospace-focused business lines.11

Meanwhile, the company commands a 75% market share of the U.S. aluminum wheel market. It has a 90% share of this market in Europe, whose heavy-duty trucks are trying to catch up to the U.S. in switching to more efficient aluminum wheels from steel.12

Howmet’s Restructuring Efforts and Profitability Growth

Howmet isn’t relying on structural marketplace demand for its growth. For the past 2.5 years, management has restructured operations to reduce the debt on the company’s balance sheet and the associated costs of that debt.

These efforts have already borne fruit. While 2023 revenue remained 7% below pre-pandemic levels, earnings rose 47% from 2019.13

The firm’s profitability benefits from its ability to pass 95% of its raw material costs to customers via contractual arrangements.14 Meanwhile, high barriers to entry limit new competition because production operations like Howmet’s require vast amounts of upfront capital.

Howmet has negotiated price increases from its customers well into 2024, and its annual price increases have expanded since 2022. CEO John Plant says that strong demand for Howmet products has aided its ability to secure favorable contract terms.15

In our view, Howmet is likely poised to become an indispensable cog in the U.S. aviation industry.

Authors

Senior Portfolio Manager

Senior Client Portfolio Manager

Check Out Our Global Growth Capabilities

Designed to capture growth early and drive alpha through stock selection.

Felix Richter, “Aviation Industry Suffers ‘Worst Year in History’ as COVID-19 Grounds International Travel,” World Economic Forum, February 18, 2021.

Michael Laris and Lori Aratani, “Taxpayers Spent Billions Bailing Out Airlines. Did the Industry Hold Up Its End of the Deal?” Washington Post, December 14, 2021.

Jaap Bower, Steve Saxon, and Nina Wittkamp, “Back to the Future? Airline Sector Poised for Change Post-COVID-19,” McKinsey & Co., April 2, 2021.

Leslie Josephs, “The Boom in Airplane Orders Is Over for Boeing and Airbus,” CNBC, December 15, 2019.

Dawit Habtemariam, “Airbus Is Filling an 8,000 Airplane Backlog Amid Strong Demand,” Skift, November 1, 2023.

Callum Keown, “Business Travel Is About to Pick Up. 4 Stocks to Catch the Comeback,” Barron’s, November 23, 2023.

International Air Transport Association, “Net Zero 2050: New Aircraft,” Fact Sheet, December 2023.

Mike Rogaway, “Precision Castparts Eliminates 10,000 Jobs as Aerospace Work Collapses,” The Oregonian, August 10, 2020.

Arconic, “About Us – History,” accessed March 20, 2024.

Yahoo Finance, “Howmet Aerospace Inc. (HWM) Company Profile & Facts,” accessed March 22, 2024.

American Century Research, July 2023.

American Century Research, July 2023.

American Century Research, July 2023.

American Century Research, July 2023.

American Century Research, July 2023.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.

No offer of any security is made hereby. This material is provided for informational purposes only and does not constitute a recommendation of any investment strategy or product described herein. This material is directed to professional/institutional clients only and should not be relied upon by retail investors or the public. The content of this document has not been reviewed by any regulatory authority.