How We Spotted the Energy Sector’s Transition to Higher Quality

Historically, energy has underperformed due to executive pay incentives favoring costly exploration and drilling projects. But recent industry shifts have led to better-performing companies.

Key Takeaways

Energy has been one of the worst-performing sectors in the small-cap universe over the long term because management teams have focused on production.

However, the focus has shifted from production to financial productivity, bringing management more in line with creating shareholder value.

A financial productivity focus aids formerly low-quality firms to bolster their quality characteristics, presenting potential investment opportunities.

Historical Underperformance of Small-Cap Energy Companies

American Century’s Small Cap Value team largely avoided small-cap energy stocks for years. Energy companies tended to emphasize oil and gas production — an expensive proposition — rather than investing capital to generate financial returns. The result? Dramatic swings in energy prices translated to volatile cash flows and stock prices.

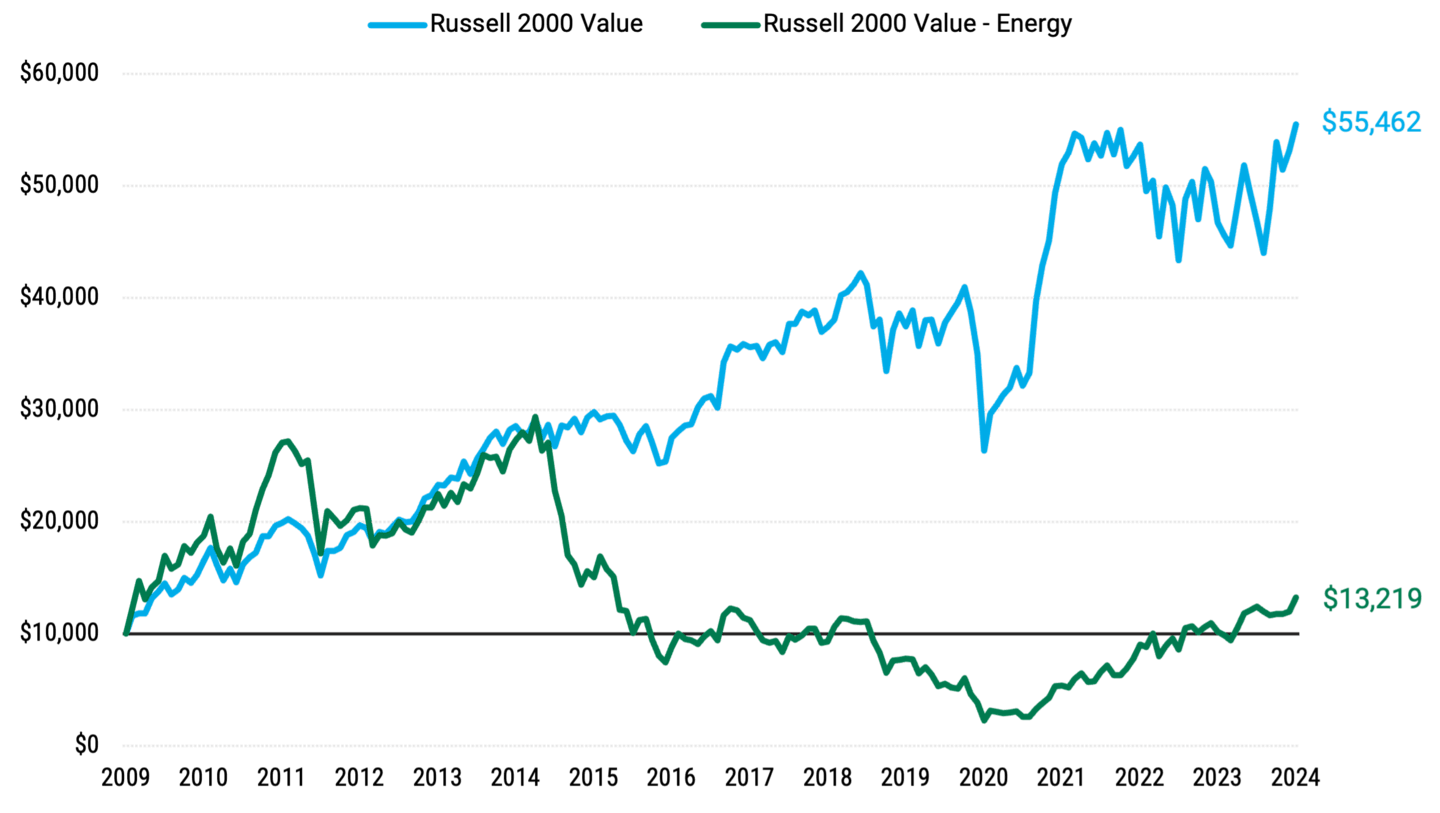

Figure 1 illustrates how poorly small energy companies have performed compared to their broader small-cap value peers.

Figure 1 | Energy Has Underperformed the Broader Small-Cap Value Market Since 2009

Hypothetical Growth of $10,000

Data from 3/31/2009 – 3/31/2024. Source: FactSet. Past performance is no guarantee of future results. This hypothetical situation contains assumptions that are intended for illustrative purposes only and are not representative of the performance of any security. There is no assurance similar results can be achieved, and this information should not be relied upon as a specific recommendation to buy or sell securities.

The world has changed in many ways in recent years, and energy companies have evolved. These positive changes have opened new opportunities to find high-quality energy stocks in the small-cap space. These stocks include firms with strong balance sheets, higher profitability and more stable cash flows.

What’s changed?

Executive Compensation Changes in Energy Companies

Incentives steer people. So, when cash bonuses for energy company executives included production goals, it made sense that the companies pulled more oil and gas out of the ground. Continuing production made less sense when oversupply pushed prices down and profits diminished.

The result was that energy companies performed poorly, as Figure 1 shows.

Investors responded to this poor performance by engaging with corporate management teams. Their message to energy management teams was that they were less willing to provide capital or participate in initial public offerings unless the companies sought to maximize free cash flow from existing assets rather than continue to increase volumes while demand remained stagnant.

Some companies eliminated production goals from compensation packages altogether. Others deemphasized production and focused instead on cost discipline, returns on capital and free cash flow generation.

Northern Oil and Gas exemplifies a company that has begun shifting its executive incentives away from production goals.

Its 2014 annual bonus structure set a goal to grow production by 15%, an achievement that would account for 24% of the CEO’s bonus.1

The following year, a significant downturn in commodity prices appeared to prompt Northern Oil and Gas to move away from production goals. The company’s 2015 performance goals eliminated production goals and reduced general and administrative expenses.2

The massive drawdown in oil demand brought on by the COVID-19 pandemic put the oversupply in focus for energy companies and accelerated the shift away from production goals.

In 2023, the Northern Oil and Gas short-term incentive plan awarded two-thirds of the annual bonus depending on performance measures, specifically adjusted earnings before interest, depreciation and amortization, and return on capital employed.3 The rest hinged on individual goals for executives.

How Shifting Goals in the Energy Sector Improved Shareholder Value

The result was energy companies that now generated excess free cash flow that could be used for increased dividends and share repurchase programs, efforts that returned value to shareholders.

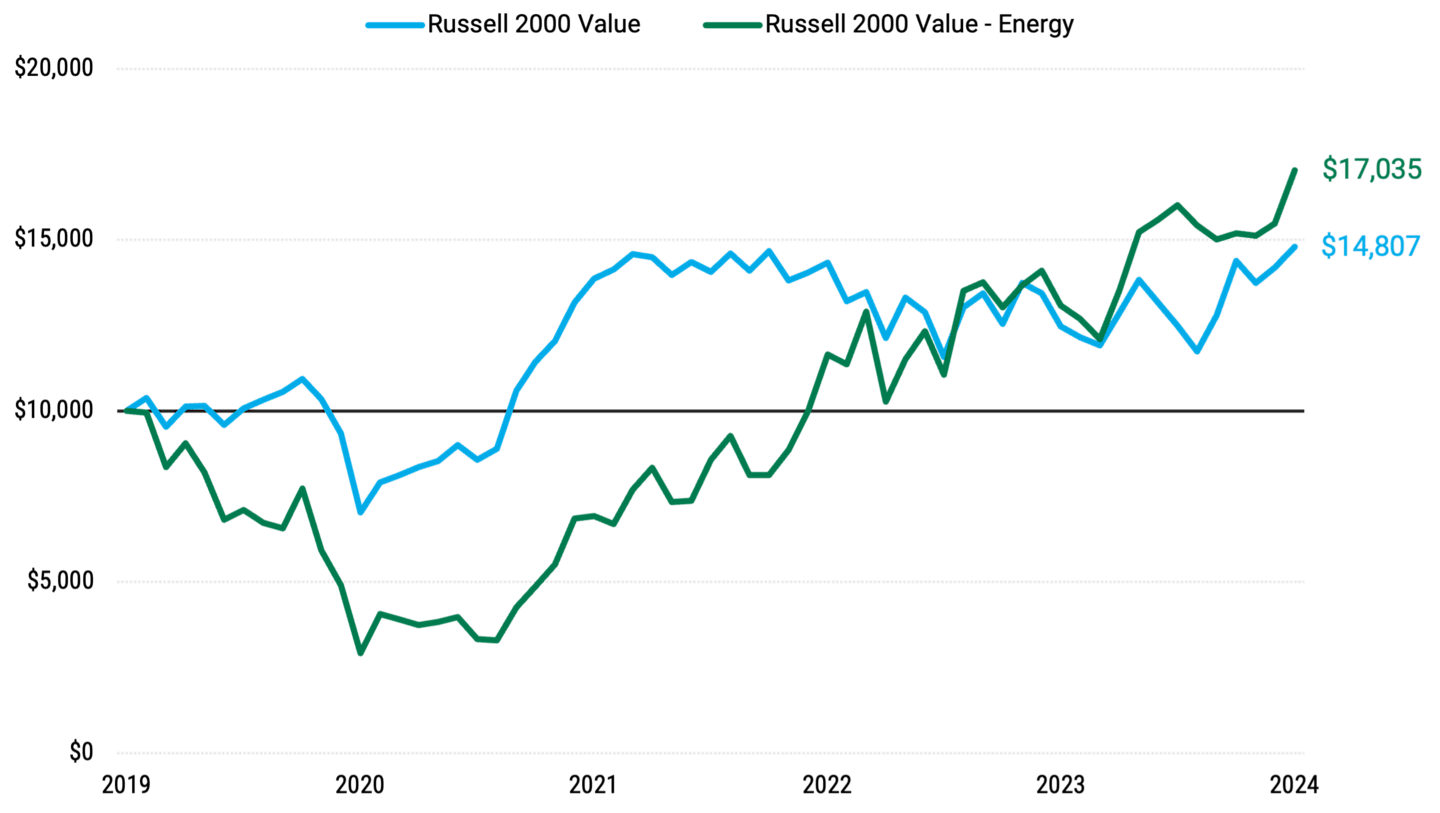

After years of underperforming the broader market, our analysis of energy stocks showed improving quality in the sector, and performance started to improve in 2020. See Figure 2.

Figure 2 | Energy Stocks Began to Rebound in 2020

Hypothetical Growth of $10,000

Data from 3/31/2019 – 3/31/2024. Source: FactSet. Past performance is no guarantee of future results. This hypothetical situation contains assumptions that are intended for illustrative purposes only and are not representative of the performance of any security. There is no assurance similar results can be achieved, and this information should not be relied upon as a specific recommendation to buy or sell securities.

As quality-oriented value managers, we evaluate stocks from three critical perspectives:

Business quality.

Management quality.

Financial quality.

Energy companies typically struggle with business quality because they can’t control the price of the commodities they produce and sell.

However, we have watched energy companies improve management quality by orienting executive compensation away from production to outcomes that are more beneficial to shareholders. We have seen financial quality improve as balance sheets significantly improve due to free cash flow generation and more conservative use of financial leverage.

With improvement to two of our three quality investment pillars and attractive valuations, our outlook for the energy sector is now brighter.

Authors

Senior Client Portfolio Manager

Explore Our Small Cap Value Strategy

Northern Oil and Gas, Inc., Schedule 14A, April 17, 2015, retrieved from SEC EDGAR website.

Northern Oil and Gas, Inc., Schedule 14A, April 22, 2016, retrieved from SEC EDGAR website.

Northern Oil and Gas, Inc., Schedule 14A, April 11, 2024, retrieved from SEC EDGAR website.

Historically, small- and/or mid-cap stocks have been more volatile than the stock of larger, more-established companies. Smaller companies may have limited resources, product lines and markets, and their securities may trade less frequently and in more limited volumes than the securities of larger companies.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and are subject to change without notice.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.