As Fed Rate Hikes Near an End, Reinvestment Risk Rises

Top of Mind: Potential peak in short-term rates highlights bond-buying opportunities for cash-heavy investors.

Key Takeaways

The Fed’s latest quarter-point rate increase may mark an end to the fastest rate-hike cycle in 40 years.

History has demonstrated that once the federal funds rate tops out, recession and rate cuts usually aren’t far behind.

Investors should be wary of reinvestment risk once the Fed shifts into rate-cut mode.

Is the 10th Time the Charm?

Another Federal Reserve (Fed) monetary policy meeting concluded with another Fed interest rate hike. Policymakers announced their 10th consecutive rate increase to tame too-high inflation on May 3. This move pushed up the short-term target lending rate by 0.25 percentage point to a range of 5% to 5.25%, a 16-year high.

While the annual headline inflation rate has moderated from 9.1% in June to 5% in March, it still sits well above the Fed’s comfort zone. Fed Chair Jerome Powell confirmed the economy is slowing, but he also indicated that the central bank will keep its options open regarding future policy action. As we’ve noted previously, the Fed has been more comfortable with the consequences of overtightening than the dangers of persistently high inflation.

It’s important to note that at its current range, the Fed’s short-term rate target is finally higher than the annual headline inflation rate. In hiking cycles dating to 1973, the Fed has never stopped raising rates until the federal funds rate exceeded the inflation rate.

As the Fed’s terminal, or peak, rate comes into focus, investors sitting on large cash balances face growing reinvestment risk. Yields on short-term cash equivalents tend to move in sync with the Fed’s rate target. So, if the Fed eventually cuts rates, yields on savings accounts, Treasury bills, CDs and other cash products likely will fall, too.

Tighter Lending Standards Heighten Recession Risk

The fastest rate-hike campaign in 40 years has contributed to a slumping manufacturing sector, a housing market slowdown and sagging consumer spending. Additionally, rapidly rising interest rates played a role in the recent high-profile bank failures. Consequently, the entire banking industry remains under pressure, posing perhaps the most serious threat to economic growth.

We expect most banks to slash their risk exposure in the coming months and tighten their lending standards. We believe a credit crunch ultimately will snowball through the economy, stifling growth, tempering inflation and triggering a recession.

History Points to a Potential Policy Pivot

If historical trends persist, the federal funds rate target won’t sit at its terminal level for an extended period. In most tightening cycles, the Fed has tended to overtighten, pushing the economy into recession. As a result, the Fed has been forced to pivot off its terminal rate relatively quickly.

Rates Could Be Lower by Year-End

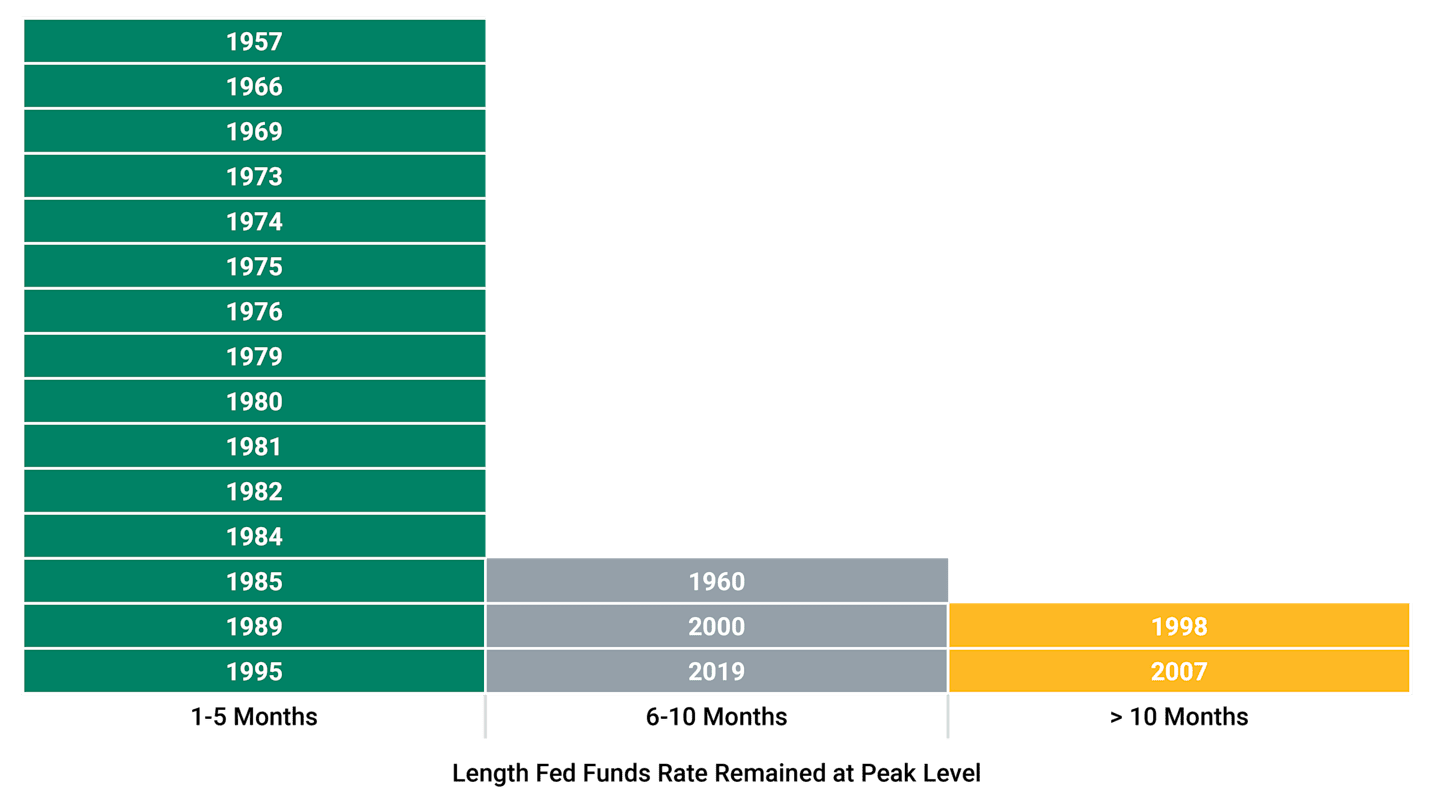

Looking at the 20 Fed tightening patterns from 1956 through 2019, the rate target remained at its peak level for an average of 4.2 months. In most periods, the terminal rate persisted for no more than five months. See Figure 1.

What’s more, our research indicates that six months after reaching its top rate, the Fed had cut rates an average of 1.8 percentage points.

Figure 1 | Peak Rates Have Been Short-Lived

Years When Federal Funds Rate Sat at a Terminal Level

Data from 8/31/1956 – 12/31/2019. Source: FactSet.

In the two outlier periods, March 1997 to September 1998 and June 2006 to July 2007, the terminal rate remained in place for more than a year. In both cases, severe recessions ultimately materialized. We don’t believe today’s economy mimics the environments of those anomaly periods.

However, given the unusual combination of factors tugging at today’s economy, we believe the potential for rate cuts is increasing. We expect market pricing to further reflect this. The timing and magnitude of Fed easing largely will depend on inflation’s trajectory and the effects tighter lending standards have on the economy.

Short-Term Yields Have Moved in Sync

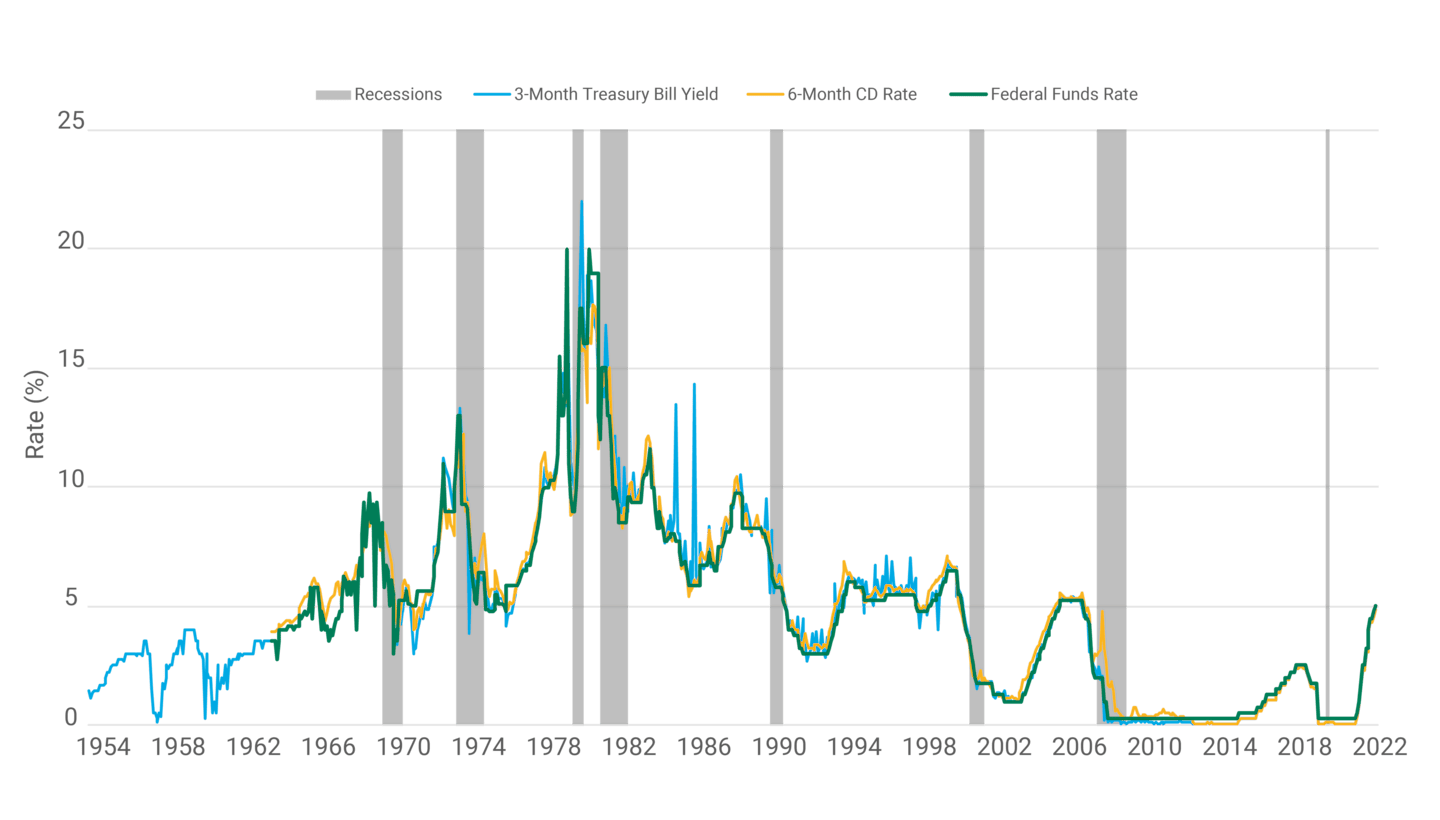

It’s important to remember that rates on Treasury bills, savings accounts, CDs and other cash equivalents typically move in tandem with the federal funds rate. Figure 2 shows the nearly identical historical paths of the federal funds rate and the three-month Treasury bill yield. It also indicates a similar pattern for three-month CD rates.

The chart also shows the relationship between rates and recessions. As you can see, short-term rates historically have topped out right before the economy tips into recession.

Figure 2 | Rates Have Reached Their Maximum Levels Ahead of Recessions

Data from 9/30/1954 - 3/31/2023. Sources: FactSet, Bankrate, Bloomberg.

Rising Reinvestment Risk: How Investors Can Respond

The dynamic between historical short-term rates and recessions suggests that investors holding cash equivalents still have time to potentially manage reinvestment risk. This refers to the inability to reinvest cash flows at a rate comparable to your current rate of return.

For cash-heavy investors, this risk rises when shorter-maturity rates fall more than longer-maturity rates, reversing the currently inverted yield curve. This phenomenon of yield-curve steepening typically happens when the Fed starts cutting rates.

If the Fed starts cutting rates later this year, yields on Treasury bills, CDs and similar products likely will drop, too. Reinvesting in these vehicles won’t provide the same returns they’re offering today.

In our view, investors have a limited window to confront reinvestment risk before the Fed changes course. One way to mitigate reinvestment risk is by moving out on the yield curve. This can help by:

Locking in higher rates.

Adding duration, which can generate capital appreciation when rates fall.

Our Fixed-Income managers believe higher-quality bonds with attractive yields, including U.S. Treasuries and higher-credit-quality corporate and securitized bonds, may help investors weather a recession.

Stay True to Your Investment Plan

As in all periods of market uncertainty, we encourage you to remain disciplined and focused on your carefully crafted investment plan. Investing across multiple asset classes and focusing on risk management may be prudent in the current market climate.

It’s also important to remember that attractive investment opportunities often emerge during market unrest. We suggest investing with experienced professionals with the insights and discipline to recognize and potentially capitalize on such prospects.

Authors

Past performance is no guarantee of future results. Investment returns will fluctuate and it is possible to lose money.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments' portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

In certain interest rate environments, such as when real interest rates are rising faster than nominal interest rates, inflation-protected securities with similar durations may experience greater losses than other fixed income securities. Interest payments on inflation-protected debt securities will fluctuate as the principal and/or interest is adjusted for inflation and can be unpredictable.

Generally, as interest rates rise, the value of the bonds held in the fund will decline. The opposite is true when interest rates decline.

Diversification does not assure a profit nor does it protect against loss of principal.