Are Income Opportunities on the Horizon?

Top of Mind: Higher bond yields may improve the prospects for income-focused investors.

Key Takeaways

Rising interest rates have pushed bond yields to levels not seen in several years.

We think investors now have more alternatives to capture attractive income potential.

Active management helps reveal ideas investors won't get from broad bond indices.

Bonds now offer the greatest income potential in more than a decade, particularly for active investors. Federal Reserve (Fed) interest rate hikes have pushed yields to multiyear highs. The combination of higher yields and attractive credit spreads has generated compelling income opportunities.

Of course, higher rates also mean tighter financial conditions are taking hold. Nevertheless, certain corners of the fixed-income market appear insulated from these risks. For example, select sectors and securities — some not represented in broad market indices — offer investors attractive income potential while featuring strong and resilient credit fundamentals.

Banks Stand Out in Corporate Credit Sector

We believe select large, nationwide U.S. banks are fundamentally sound, exhibiting strong profitability, still-benign asset quality and decent capital levels. Higher short-term interest rates are aiding banks’ net interest income, a trend that should continue amid moderate loan growth.

We expect credit quality to normalize following historically low charge-offs (debts banks have written off as losses because they don’t expect borrowers to repay them). But the banking sector’s healthy profitability and solid capitalization should help mitigate the associated costs.

Furthermore, the new issue supply of bonds from large U.S. banks is likely to decline by 15% to 20% in 2023. This reduced issuance may help buffer some spread volatility as the economy slows. Potential regulatory changes also may help the backdrop for large and select regional banks.

Rising Stars Shine in High-Yield Market

Elsewhere in the corporate sector, we believe higher-rated high-yield securities offer attractive performance potential generally unavailable in portfolios tracking broad investment-grade indices. While below-investment-grade corporates contain notable yield advantages, quality considerations remain pertinent, particularly in today’s economy. That’s why we favor “rising stars,” or BB-rated securities positioned for a likely upgrade into the investment-grade category.

When a borrower’s credit rating rises to investment grade, the bond’s total return typically improves. Investors can benefit from the bond’s income and the price appreciation associated with the credit-rating upgrade. We believe several borrowers that were downgraded from investment grade to high yield in 2020 should make a round trip back to investment grade.

Multifamily Housing Delivers Value in Securitized Sector

Home prices and mortgage rates are notably higher than they were only a year ago. This trend has pushed home ownership out of reach for many Americans, suggesting that demand for rental housing should remain robust. Commercial real estate collateralized loan obligations (CRE CLOs) allow active investors to participate in this trend.

These investment-grade, floating-rate securitized securities offer exposure to portfolios pools of first-lien mortgages that finance multifamily apartment buildings. The mortgages have a loan-to-value at origination of 65% to 70% and a maximum of five years remaining in the contract. The properties are not reappraised during the life of the loan unless a performance issue emerges.

As apartment owners pay off their loans, the CRE CLO is repaid. These securities contain features designed to limit risk:

If the borrower defaults, the CRE CLO forecloses on the property.

Senior-most CRE CLOs, which are the first to pay down, benefit from a relatively low loan-to-value position, which may help insulate investors from loss.

CRE CLO sponsors have significant skin in the game. They retain approximately 15% of the trust’s most subordinated securities, which are junior securities and the first to bear risk of loss. This feature helps align the interests of the sponsor and the security holders.

Aircraft ABS Dominate Opportunities in Structured Credit

China’s recent reversal of COVID-19 restrictions should boost demand for air travel and aircraft. However, the world’s existing aircraft fleet won’t meet future commercial passenger demand, and ongoing supply chain kinks disrupt new aircraft production. These factors should translate into higher values and lease rates for existing aircraft.

Against this backdrop, senior investment-grade asset-backed securities (ABS) offer an opportunity to participate in the bullish dynamic unfolding in the commercial passenger aircraft industry.

Aircraft ABS are fixed-rate, investment-grade bonds with relatively short (two- to four-year) maturities. Last year, China’s zero-COVID policy and the Russian invasion of Ukraine weighed on these securities and drove down their prices. But at today’s discounted pricing, we believe aircraft ABS offer significant income potential for investors.

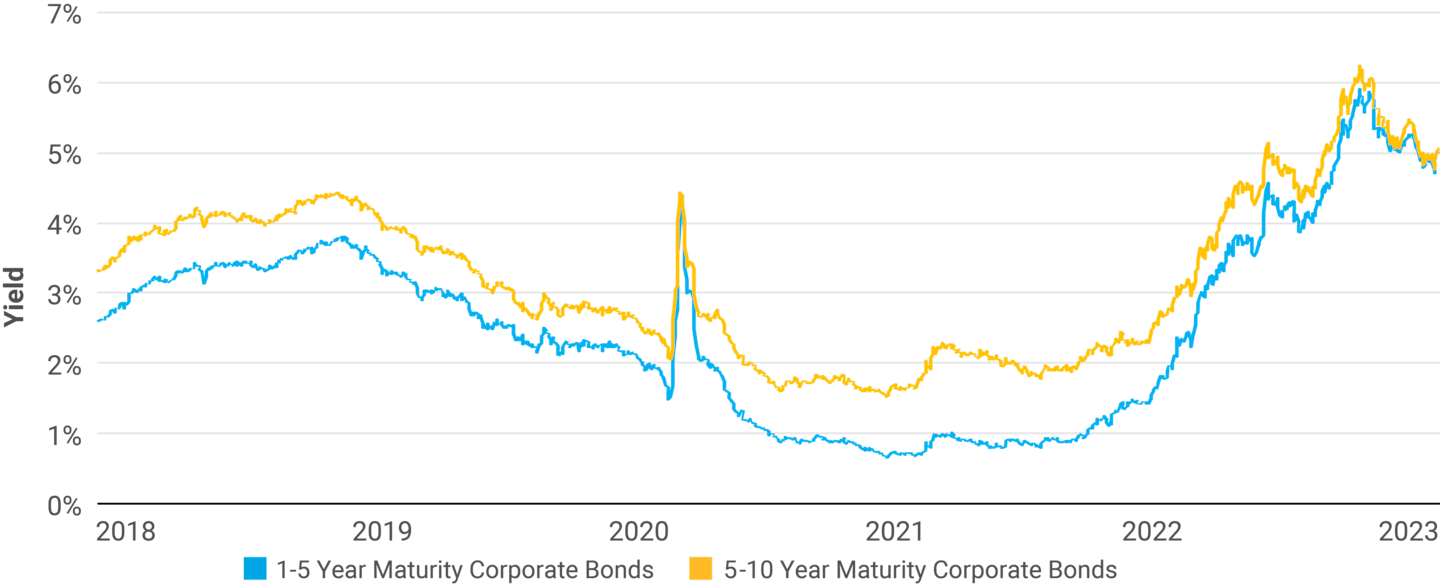

Short-Maturity Focus Highlights Yield Advantages

Ahead of a recession, the U.S. Treasury yield curve often inverts—that is, shorter-maturity securities offer higher yields than longer-maturity securities. As investors position their portfolios for a recession and potential Fed rate cuts, longer-maturity yields tend to fall.

Because of this trend, shorter-maturity corporate bonds offer similar yields as longer-maturity bonds, as Figure 1 demonstrates. At the same time, shorter-maturity bonds also feature less interest rate risk than longer-maturity bonds. In our view, this combination makes shorter-maturity bonds a more attractive alternative in today’s market.

Figure 1 | Yield and Risk Dynamics Favor Shorter-Maturity Bonds

Bloomberg U.S. Corporate Bond Index Component | End of Period Yield* | Minimum Yield for Period | Maximum Yield for Period |

1-5 Year Maturity Corporate Bonds | 4.89% | 0.66% | 5.91% |

5-10 Year Maturity Corporate Bonds | 4.95% | 1.52% | 6.24% |

*Yields reported from 1/1/2018 - 2/8/2023. Source: Bloomberg. The Bloomberg U.S. Corporate Bond Index consists of publicly issued U.S. corporate and specified foreign debentures that are registered with the Securities and Exchange Commission and meet specific maturity, liquidity and quality requirements.

We Think Active Management Is Crucial to Capturing Income

While the rapid and significant tightening of monetary policy has led to heightened recession risk, it also has boosted yield levels. Yields are higher across maturities and credit quality categories, and income potential is plentiful. However, we continue to stress the importance of thoughtful sector allocation and security selection.

These tenets of active management should be important considerations regardless of the economic backdrop. But as the economy slows, we believe they represent crucial components of building portfolios and generating income.

Authors

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

Generally, as interest rates rise, the value of the bonds held in the fund will decline. The opposite is true when interest rates decline.