2026 Global Fixed Income Outlook

Third Quarter

Key Takeaways

Steady growth should propel the U.S. economy through a mix of strong headwinds from the conflict in Iran, inflation and more.

Recent fiscal policy effects, including larger-than-usual income tax refunds and solid jobs data, have helped keep the economy growing.

Nevertheless, the risk potential on the upside and downside is growing, underscoring the importance of active, measured fixed-income positioning.

Why Does Active Fixed-Income Management Matter in 2026?

In a somewhat surprising turn of events, recent economic shocks, particularly from rising oil prices, haven't derailed U.S. economic growth. But these disruptions have amplified the potential risks in the markets, underscoring the importance of active fixed-income management.

This approach may help highlight compelling investment opportunities and enable investors to rotate portfolio exposures as those opportunities shift. In our experience, maintaining portfolio agility often delivers solid long-term performance potential.

What Do GDP and Jobs Data Suggest About Economic Growth?

The U.S. economy remained remarkably resilient in the first half of 2026 despite several challenges, including:

The Iran war, which has stoked inflation, pushed interest rates higher and likely squashed hopes for Federal Reserve (Fed) rate cuts this year.

A crisis of confidence in private credit amid rapid growth and high-profile defaults.

Ongoing uncertainties about artificial intelligence’s (AI’s) effects on traditional economic sectors and the labor market.

Despite these pressures, steady economic growth has prevailed. Annualized gross domestic product (GDP) improved to 1.6% in the first quarter, compared with 0.5% in the prior quarter. As of June 1, the Federal Reserve Bank of Atlanta estimated that second-quarter growth may jump to 3%.

Additionally, U.S. manufacturing in May logged its 10th straight monthly expansion. This marked the strongest growth rate since May 2022, fueled by sharp production gains and robust new orders. Meanwhile, recent strong job gains and a steady unemployment rate underscore labor market resiliency.

Tax Refunds Help Keep Consumer Spending on Track

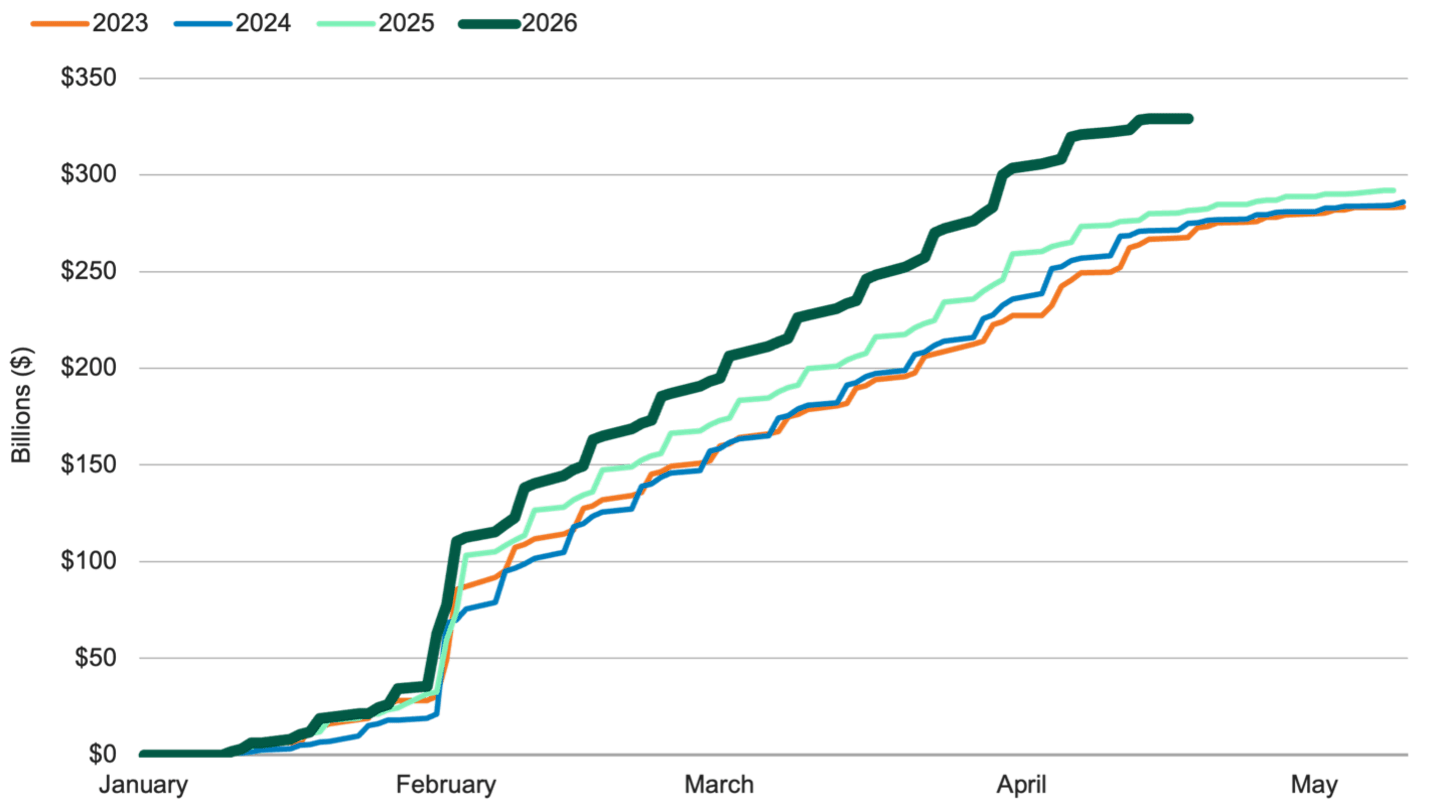

Supportive fiscal policies, including provisions in last year’s One Big Beautiful Bill Act, have also helped. Consumer spending has been a main driver, as U.S. households received larger-than-usual tax refunds this year. See Figure 1.

Figure 1 | 2026 Tax Refunds Considerably Higher Than Previous Years

Cumulative Individual Income Tax Refunds Issued During Tax Season

Data from 1/22 – 5/31 for 2023-2025. Data for 2026 is from 1/22 – 5/11. Source: U.S. Treasury.

How Can Active Management Address Various Market Scenarios?

We believe steady economic growth remains the most likely course ahead. However, the upside and downside tails of that outlook have grown fatter:

In the upside tail, energy prices recede to reveal a cyclical upswing in the U.S. economy. While this outcome would be positive for growth, volatility would rise as Fed tightening moves from a risk to a reality.

In the downside tail, the Strait of Hormuz remains closed or constrained, global oil inventories reach critical levels, and prices spike. Demand destruction takes hold, ultimately hitting global growth when there’s little room to adjust monetary or fiscal policy.

In our view, financial markets aren’t pricing enough risk premiums for either scenario. Accordingly, our active fixed-income approach highlights what we believe is middle-of-the-road risk/reward exposure in our portfolios while seeking security- and sector-specific opportunities.

We believe this dynamic strategy should help us respond if markets shift to the upside or downside, or if broad risk premiums become attractive again.

U.S. Government Bonds

We expect the yield curve to remain relatively stable. With the Fed on an extended pause, short-maturity Treasury yields should stay fairly steady. Amid ongoing inflation and concerns about federal debt, we expect the 10-year Treasury yield to trade between 4.25% and 4.75%.

Persistent inflation may periodically cause markets to price in Fed rate hikes, creating opportunities to add duration, particularly if the two-year yield exceeds 4.25%.

U.S. Securitized Assets

In today’s dynamic markets, we remain selective, focusing on disciplined security selection and strategic sector rotation. Among asset-backed securities (ABS), this rotation has led to shorter-duration, higher-yield positioning, largely within consumer subsectors. We also believe pockets of the non-agency mortgage-backed securities (MBS) sector offer relative value.

Municipal Bonds

Municipal credit fundamentals are beginning to normalize following a period of exceptional strength. As revenue growth lags rising expenses and federal support declines, elevated reserves continue to provide a cushion. We expect fiscal pressures, particularly tied to health care and social programs, to build and contribute to greater dispersion across issuers and sectors.

Valuations remain tight, reinforcing the importance of selectivity. Strong demand for capital, driven by infrastructure investment, housing needs and refinancing activity, should support elevated issuance. Demand dynamics and reinvestment flow are supporting the market’s technical backdrop.

We continue to find value in sectors such as energy prepays, multifamily housing and development districts. A shifting credit environment and steady technical backdrop should continue to favor disciplined, high-quality positioning.

U.S. and Non-U.S. Corporate Bonds

Corporate credit fundamentals have generally remained solid, and default rates have stayed low. But higher interest rates and geopolitical risks are driving increased dispersion across sectors, ratings categories and regions, underscoring the importance of thoughtful security selection.

M&A, rising stars* and issuer-specific catalysts continue to create opportunities that we think could be attractive. We currently prefer investment-grade securities over lower-quality credit, where we remain cautious.

In Europe, we still favor financial sector subordinated bonds, remaining disciplined on securities’ structure and pricing.

Money Markets

We believe money market assets may keep realizing new highs for the second half of 2026. Recently, spreads between Treasury coupons and Treasury bills have remained at record levels. We expect to pivot into this rare opportunity, which persists due to the market’s expectations for interest rate hikes. But, unlike the market, we’re not convinced the Fed will tighten this year. Instead, we expect a longer pause in interest rates under the new Fed chair, Kevin Warsh. This backdrop should provide opportunities for us to extend maturities and rotate out of bank risk via commercial paper.

In the municipal money market, diversification remains our ongoing focus amid slowly declining assets and very limited supply.

Emerging Markets (EM)

Despite sharp spread tightening in April, we expect a more challenging outlook ahead due to weaker fundamentals, particularly from oil importers, and expensive valuations. An extended period of high oil prices could shift investor concerns from inflation to sagging global growth and financial conditions. This mix could lead to de-risking from the asset class.

Given this view, we seek bonds offering value due to improving credit trends, multilateral support and a commitment to structural reforms. We prefer idiosyncratic stories offering moderate correlation with global macro risks.

Countries exhibiting these features include Colombia, Argentina and Ecuador. Our local rates exposure favors Latin America, a commodity exporter region offering some of the market’s highest yields. We’re generally avoiding Asia due to its low yields and its status as an energy importer.

*Lower-quality bonds expected to achieve a credit-rating upgrade from high yield to investment grade.

Explore Our Global Fixed Income Capabilities

The letter ratings indicate the credit worthiness of the underlying bonds in the portfolio and generally range from AAA (highest) to D (lowest).

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.

International investing involves special risks, such as political instability and currency fluctuations. Investing in emerging markets may accentuate these risks.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

Historically, small- and/or mid-cap stocks have been more volatile than the stock of larger, more-established companies. Smaller companies may have limited resources, product lines and markets, and their securities may trade less frequently and in more limited volumes than the securities of larger companies.

Diversification does not assure a profit nor does it protect against loss of principal.

Generally, as interest rates rise, bond prices fall. The opposite is true when interest rates decline.

Past performance is no guarantee of future results. Investment returns will fluctuate and it is possible to lose money.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

©2026 Morningstar, Inc. All Rights Reserved. Certain information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.