Getting Kids Started With Saving and Budgeting

Budgeting for teens and younger kids? Yes, it’s a thing. Make a positive impact on your kids’ future money habits with our tips on teaching them about saving and managing money.

Key Takeaways

Kids can start building good money habits and learn the trade-offs between spending and saving even before entering grade school.

Teaching kids about the power of compounding can be a strong motivator that may help them reach life’s larger financial goals.

Parents can be their kids’ most influential teachers. Sharing how you worked toward your goals can help them see that their dreams are achievable.

Most parents experience times when it’s quicker and easier to do something themselves than to teach their children how to do it. But with many aspects of raising kids, including financial education, they often learn more by doing.

Actively involving kids in saving and managing money—building on lessons over time and even letting them learn from mistakes (that are inconsequential now)—can set them on a path to financial independence.

Financial literacy lessons have an “overwhelmingly” positive impact on students’ future financial habits, from budgeting and saving to avoiding predatory loans.¹

Here are some tips for teaching kids to save and manage money.

Start Young to Build Good Money Habits

Setting aside money, getting used to delaying gratification and understanding the trade-offs between saving and spending are key concepts behind reaching life’s large financial goals. Kids can start learning these lessons even before they enter grade school.

Go From Piggy Banks to Digital Apps

Are they still getting cash for birthday and holiday gifts? While sometimes people give money for a specific purchase, make it a practice to designate a portion of cash gifts for savings.

Young kids might start with an "old-fashioned” piggy bank or a glass jar that shows how their money accumulates. Once they fill the container or hit a predetermined amount, have them go with you to a bank and deposit the money in a savings account.

When kids have their own savings accounts, it can give them a sense of ownership and responsibility. Another reason to open an account sooner rather than later is to take advantage of the many digital options now available for managing allowances and spending.

Get Them Familiar With How Much Things Cost

Going grocery shopping? Share with kids the decisions you make when making a purchase. The grocery store is great for this because there are usually several different brands and prices of one type of item.

For example, maybe you go to the yogurt aisle and buy more of your favorite brand because it’s on sale. Or maybe there is a cheaper yogurt brand, but you explain that you’re willing to pay more for the healthier option. Teaching kids to discern their choices goes a long way when they’re making their own purchasing decisions.

Show Them the Power of Compounding

As kids get older, introduce them to the power of compounding. Who doesn’t like to see their account balance grow beyond their initial deposit?! Compounding can be a strong motivator that may help them in adulthood to:

Make a down payment on a home.

Save for their own children’s college educations.

Invest to fund their retirement.

Compounding occurs when you earn money on your original investment plus any earnings for that investment. The longer money is invested, the more earnings you may receive and the more compounding may grow your account balance.

Do you have an education savings account for your child? You can lead by example by sharing how compounding is helping you save for them—and how sticking with a financial goal might pay off over time.

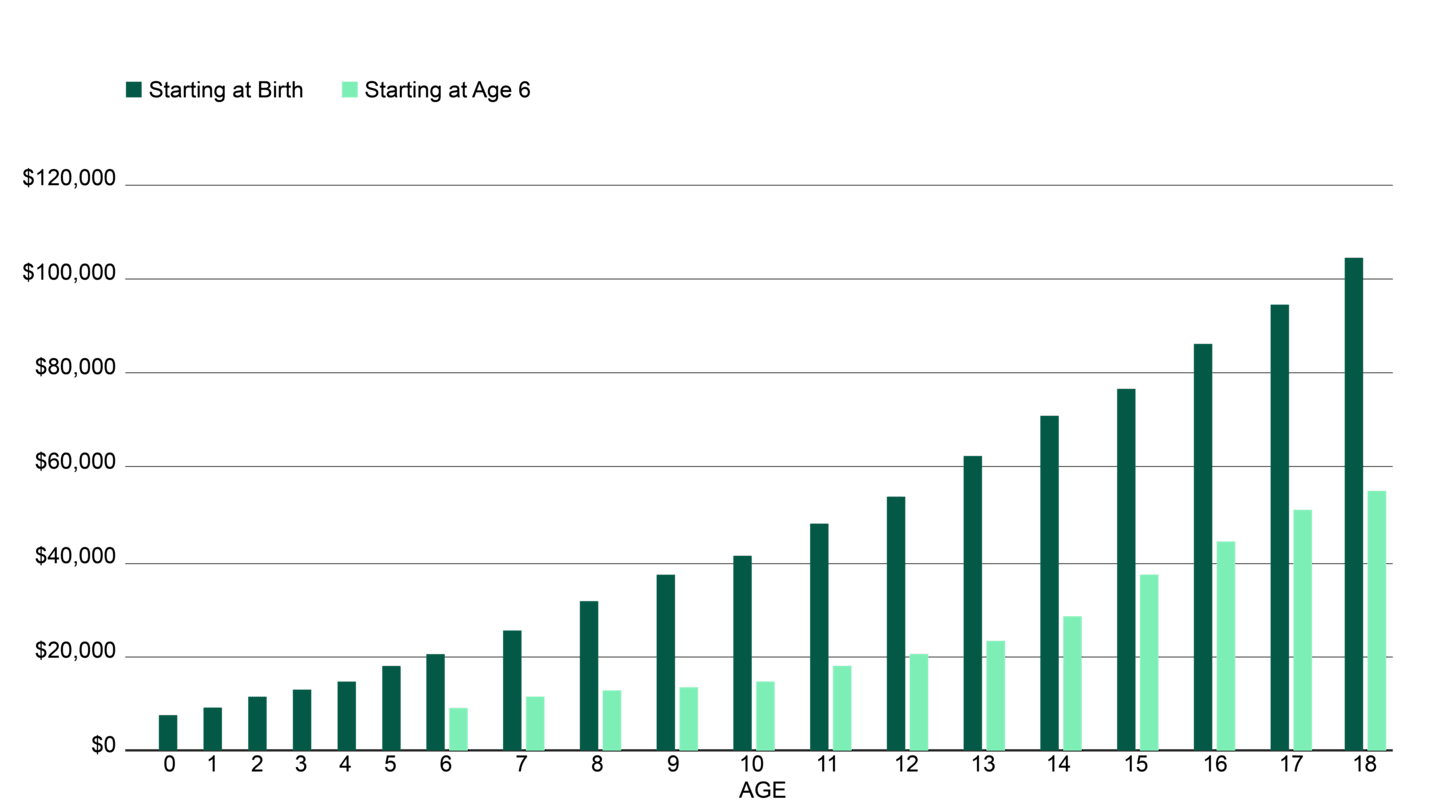

How Time and Compounding Work Together

The earlier a person takes advantage of compounding, the more time money has to grow—and the less money a person may need to contribute to reach a goal.

How Time and Compounding May Help You Save More Money for College

Source: American Century Investments, 2025, Future Value Calculator, dinkytown.net. The hypothetical calculation assumes an initial investment of $2,500 and additional monthly contributions of $250 earning a rate of 6% annually over 12 and 18 years, respectively. It assumes reinvestment of all realized gains, dividends, and interest receipts and does not account for the effects of any added fees, expenses, or taxes that might be incurred. If all taxes, fees, and expenses were reflected, reported portfolio values would be lower. This hypothetical situation contains assumptions that are intended for illustrative purposes only and are not representative of the performance of any security. There is no assurance similar results can be achieved, and this information should not be relied upon as a specific recommendation to buy or sell securities.

But remember, while compounding can lead to exponential growth with positive returns, negative returns can erode capital. And the more a portfolio loses, the more it must gain to get back to even.

Budget for Needs and Wants—Kids Edition

Understanding the difference between needs and wants is another key part of learning to manage money responsibly. It’s OK to spend money on wants, but it shouldn’t mean giving up something you actually need.

You need clothing, but pricey designer labels are a want.

You need a phone but want the latest model with all the bells and whistles.

Have budding fashionistas? Establish a clothing allowance. Give your children a budget of what you will spend on an item and have them decide whether to use their own money for a more expensive version.

Teaching Opportunity Cost

Sticking to a budget means if you decide you want the pricier option, you will sacrifice something else. It’s important to discuss the concept of opportunity costs—what we give up when we make decisions.

Consider letting elementary kids practice budgeting by planning for a family night. They can decide whether the family goes to a nice restaurant or gets a cheaper takeout meal and rents a movie for an evening at home.

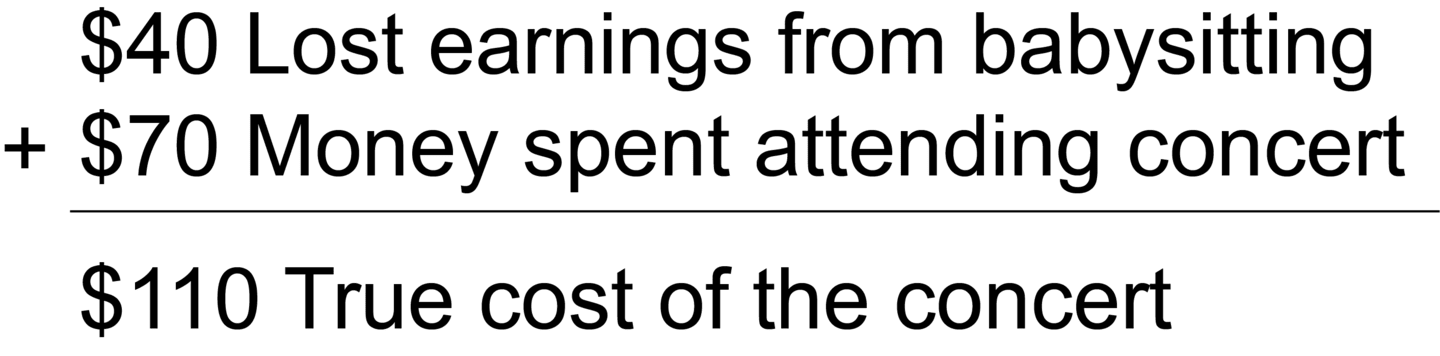

There is also a cost when deciding what to do with our time. Let's say your teenager trades a night of earning money babysitting to attend a concert with friends. The opportunity cost includes the money they forfeited.

How to Encourage Kids to Save

Instill a Habit of Financial Goal Setting

Goal setting is the heart of every financial plan. Encourage kids to save for something that excites them, whether it’s a new toy, tablet, skateboard, concert tickets or something else. By working toward a specific goal, they will develop the discipline needed to achieve larger savings goals as they mature.

Help them figure out how much money they will need, how much they can save each week and how long it will take to reach their goal. Then, they can track their progress over time.

If they don’t have something specific they want to save up for, set a monetary goal instead. The amount should be realistic but also high enough that they can feel a sense of accomplishment at reaching that goal.

And talk to your kids about how you have worked toward your own goals—such as repaying student loans, purchasing a house or funding your retirement—and the trade-offs you’ve made along the way. Your examples can help them see that goals are achievable.

Help Them Stretch Their Dollars

Saving money also means making smart purchases so money goes further. Before they make a purchase, show them how to comparison shop and look for coupons.

You can also challenge teens to find low-cost or free alternatives to some of the items on their wish lists. Do they need to buy everything they want, or can they borrow it? Many public libraries offer a selection of current movies and video games cardholders can use for free.

Make a Matching Contribution

Just as some employers offer a match on funds invested in the company’s retirement plan, you could offer to match money your kids put into their savings accounts to reinforce this habit and help their money grow.

You could also offer rewards for maintaining a certain balance in their checking accounts so they aren’t tempted to spend that money. That said, allowing your teens to spend money and experience buyer’s remorse can be a helpful (if a bit painful) lesson for them to learn.

It’s Important to Have the Money Talk

Money conversations may not be easy, but they are necessary. You'd much rather your child make a minor mistake—with birthday money from Uncle Bill—than a whopper of a mistake when the stakes are higher as adults.

Make financial literacy a part of your children’s education—even the youngest children can learn the value of a dollar. With your help, they’ll be empowered to make better financial decisions and have a better chance to build a stable financial future.

Authors

Is Your Child Ready for the Markets?

Help teens understand the basics of investing.

Leonard, Daniel. Teaching Kids to Manage Money Yields Big Returns, Research Says, www.edutopia.org. August 20, 2024.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

You could lose money by investing in a mutual fund, even if through your employer's plan or an IRA. An investment in a mutual fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.