Got Bonds? Understanding Interest Rate and Reinvestment Risks

If you have bond investments, then you have interest rate and reinvestment risks. Investors can’t eliminate the risks, but they can seek to mitigate them. Here’s how.

Key Takeaways

The prospect that a bond you hold loses value due to rising interest rates is known as interest rate risk.

Reinvestment risk is the inability to reinvest money into securities that will earn the same or higher rates as your original investment.

Having a mix of bond holdings—different bond types and maturities—can help you manage bond risks.

New investors quickly learn that investing in bonds can help diversify portfolios because bonds are typically less volatile than stocks. And bonds can offer regular income no matter the interest rate environment.

But investing in bonds involves risks, including interest rate and reinvestment risks. These risks can affect individual and professional investors.

Let’s review interest rate risk: how it affects bonds, how it can impact individual and professional investors, how it relates to reinvestment risk and how you can strive to manage bond risks in your portfolio.

What Is Interest Rate Risk?

Current interest rates help determine a new bond’s coupon—that is, how much income you’ll receive from the bond’s regular interest payments. A bond’s coupon is the rate of interest a bond pays annually. So a $1,000 bond with a 3% fixed coupon would pay $30 in interest annually.

While bond issuers set the coupon when they launch the bond, its current yield—the bond’s coupon divided by the current market price—will change as market prices change.

Interest rates and bond prices move in opposite directions. When market interest rates rise, newly issued bonds will offer coupons and yields that align with prevailing interest rates. However, prices on existing bonds generally decline because their yields don’t reflect the higher level of interest rates now available in the market.

Conversely, as interest rates fall, prices of older bonds with higher coupons increase amid rising investor demand for the higher-yielding securities.

Interest rate risk refers to the possibility of a bond losing value due to rising interest rates.

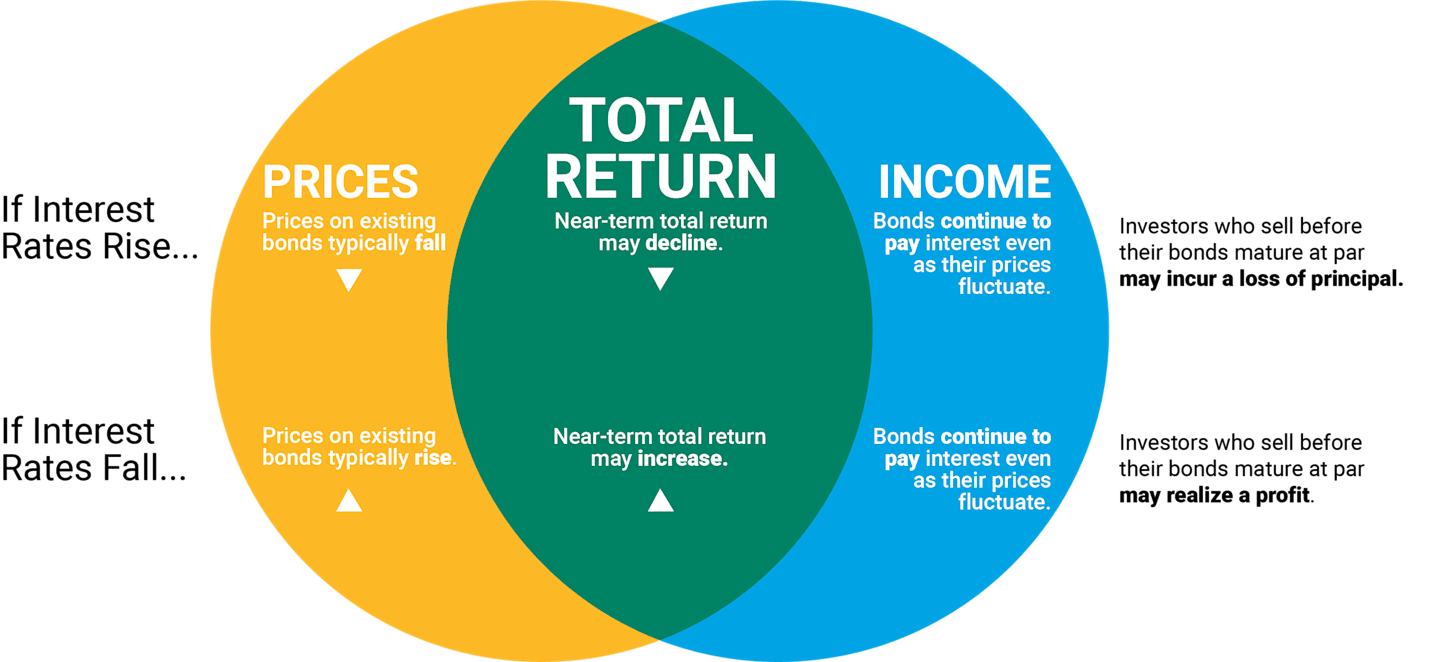

How Changing Interest Rates Impact Bond Investments

If interest rates rise, prices on existing bonds typically fall. Bonds continue to pay interest even as their prices fluctuate, but the near-term total return (price change and yield) may decline.

Examples of Interest Rate Risk Impacting Investors

Individual Investors

Consider a scenario where you buy a bond at a par value of $1,000 with a fixed coupon of 3%.

If market interest rates rise to 4%, newly issued fixed-rate bonds may feature a 4% coupon.

You will have trouble selling your existing bond in the secondary market because newer bonds can provide more attractive yields.

The lower demand will trigger lower prices, and the market value of your 3% coupon bond likely will drop below your $1,000 purchase price. If you sell the bond before it matures, you may incur a loss of principal.

Institutional Investors - Banks

Banks and similar financial institutions must carefully manage bond risks. In addition to making loans, banks may also invest money in bonds and other debt securities for current income to fund customer withdrawals and other business needs.

But even professionals in the banking sector can mismanage interest rate risk. Consider Silicon Valley Bank (SVB).

SVB experienced rapid deposit growth between 2019 and 2022. The bank parked its deposits primarily in longer-maturity, fixed-rate bonds at prevailing interest rates, which were lower in those years. Then the Federal Reserve (Fed) began raising interest rates in early 2022.

As interest rates rapidly rose, the value of the bank’s bond holdings—particularly its longer-duration securities—declined.

The bank needed to pay higher interest rates on its deposits to keep existing account holders and attract new business.

However, SVB’s large venture capital client base wasn’t attracting enough new deposits to offset bank withdrawals.

With withdrawals growing, management had to sell securities to raise cash. But those securities had declined in value, given the rising-rate environment.

Some banks are better than others at managing these risks, and our investment professionals found SVB's downfall to be company-specific. However, the revelation of SVB’s risky business practices led to renewed investor scrutiny of the entire banking sector and the combination of federal, state and regulatory agency oversight.

Measuring Bonds’ Interest Rate Sensitivity With Duration

Although the prices of all bonds are affected by interest rate fluctuations, the magnitude of the change varies. Duration, expressed in years (but is not the same as a bond’s maturity), is a key measure of a bond fund’s sensitivity to interest rate changes.

The longer the duration, the more a bond’s value will rise or fall with changes in market interest rates.

How Duration Can Help You Manage Interest Rate Risk

Investors can’t eliminate interest rate risk, but they can seek to mitigate it by looking at their mix of longer- and shorter-duration bonds.

If investors think interest rates have peaked and will likely move lower:

Focus on Longer-Duration Bonds

Investing in longer-duration, higher yielding bonds or funds when interest rates are high offers price appreciation potential if interest rates fall.

If investors think interest rates have not peaked and will continue to rise:

Focus on Shorter-Duration Bonds

Investing in shorter-duration bonds or funds when interest rates rise may help limit price declines because their prices are less sensitive to changes in interest rates.

Keeping an Eye on Reinvestment Risk

Reinvestment risk is another element to consider. This risk is the inability to reinvest money into securities that will earn the same or higher rates as your original investment.

Going back to our bond example with the 3% fixed coupon, what if interest rates fell to 2%? You would first be a happy investor because your bond’s price likely would rise above your $1,000 purchase price—as interest rates fall, bond prices generally rise. The 3% bond pays more than newly issued bonds at 2%.

However, suppose your bond matures in a year, and you want to purchase another bond. You would reinvest your principal in a lower interest rate environment, and your new bond investments will not earn as much as before.

When it seems that the Fed might cut interest rates, investors may face growing reinvestment risk. Yields on short-maturity bonds and cash equivalents tend to move in sync with the federal funds target rate. So, if the Fed cuts rates, yields on savings accounts, Treasury bills, certificates of deposit and other similar investments likely will fall too.

Reinvestment risk is heightened when the yield curve is inverted; that is, when shorter-maturity yields are higher than longer-maturity yields. As the yield curve shifts to its normal upward slope—typically when the Fed starts cutting rates—shorter-maturity yields will lose their relative attractiveness. (Learn more about what the shape of the yield curve can tell investors.)

Having some longer-maturity bonds or bond funds may help mitigate reinvestment risk in this situation. Adding duration with longer maturity holdings may help generate capital appreciation when rates fall. However, if rates have not yet peaked, this move would increase your interest rate risk.

As Rates Move, Risk Exposures Change

Some Ways to Help Manage Bond Risks

Diversify Holdings With Higher-Yielding Bonds

Corporate bonds or mortgage-backed bonds are typically less sensitive to interest rate changes than Treasuries and thus can diversify high-quality bond portfolios. But keep in mind that these bonds are typically riskier than Treasuries and add exposure to another risk—credit risk.

Spread Out Bond Maturities With Bond Laddering

Bond laddering is a strategic approach that many active managers of diversified fixed-income portfolios use to manage interest rate risk. It involves having bonds with different maturities so you have smaller amounts to reinvest over time.

For instance, if investors have $50,000 to invest, they might divide that into equal parts and put $10,000 each in bonds that mature in one, two, three, four and five years. When the one-year bond matures, investors use the proceeds to buy a new five-year bond at the prevailing market rate.

If interest rates have risen, investors have the opportunity to buy a bond offering a higher yield.

If interest rates have fallen, the investor may still buy a new five-year bond to keep the bond ladder in place. However, the other bonds in the portfolio may continue to yield returns more elevated than the current market rates for new bonds.

Why Investors May Benefit from Actively Managed Bond Funds

Interest rate and reinvestment risks are just two of many aspects to consider when investing in bonds. Economic, sector- and issuer-specific issues and more can affect bond returns. If managing it all on your own seems daunting, you might look into a professionally managed fund.

The investment professionals on our actively managed funds have the flexibility to adjust portfolios as market risks and opportunities shift, which gives them the potential to outperform.

And when interest rates are rising, a bond fund will reinvest the coupon payments and maturing securities in its portfolio at the new, higher rate, so the fund typically will reflect the increase in prevailing yields faster than many investors buying individual bonds on their own.

Match Duration With Your Time Frame?

The nearer you are to your goal, and/or the more sensitive you are to potential changes in the value of your portfolio, the shorter your duration likely should be.

If Your Time Horizon Is Approximately 3 Years

Consider our shorter-duration investments:

If Your Time Horizon Is Longer Than 3 Years

You may be willing to accept a higher degree of interest rate risk for higher potential rewards. However, if your goals are more long term, we believe intermediate-term, core diversified fixed-income holdings may be a good option.

We offer several funds with an intermediate duration. You may want to consider:

Look at Your Entire Portfolio

One of the best ways to prepare for all market conditions is to have a fully diversified portfolio. For example, stocks generally are less sensitive to changes in interest rates than bonds.

You can remove the guesswork from choosing investments with one of our asset allocation portfolios.

Our time-based and risk-based portfolios combine stock, bond and short-term investments in a single fund—and include a mix of investments that help mitigate interest rate risk.

More Resources for You

What about inflation risk? Learn about staying ahead of inflation.

Get the latest views on interest rates and the bond market from our fixed-income team.

We Have Your Interests at Heart

Let’s talk about the impact of changing interest rates on your portfolio.

The target date in a fund's name is the approximate year when investors plan to retire or start withdrawing their money. The principal value of the investment is not guaranteed at any time, including at the target date.

Each target-date fund seeks the highest total return consistent with American Century Investments' proprietary asset mix. Over time, the asset mix and weightings are adjusted to be more conservative. In general, as the target year approaches, the portfolio's allocation becomes more conservative by decreasing the allocation to stocks and increasing the allocation to bonds and cash equivalents.

Generally, as interest rates rise, the value of the bonds held in the fund will decline. The opposite is true when interest rates decline.

Fund shares are not guaranteed by the U.S. Government.

The prospectus contains very important information about the characteristics of the underlying security and potential tax implications of owning this fund.

As with all investments, there are risks of fluctuating prices, uncertainty of dividends, rates of return and yields. Current and future holdings are subject to market risk and will fluctuate in value.

Investments in fixed income securities are subject to the risks associated with debt securities including credit, price and interest rate risk.

Diversification does not assure a profit nor does it protect against loss of principal.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.