Tee Up a Smart Strategy: Investing for the Long Term

While many are seeking quick results, investing for the long term may be a better approach for life’s most important goals.

Key Takeaways

Long-term investing can help keep you on track by rewarding patience, discipline and a steady focus beyond short-term market swings.

Choosing investments built for a long-term strategy—and resisting the pull of short-term trends—can make a meaningful difference over time.

Some common hazards can throw investors off course, but planning, diversification and professional guidance can help.

Like golf, making investment decisions for your future can seem challenging and even intimidating when you first start. But that’s not where the similarities end. Both require careful decision-making, strategies to avoid hazards, a focus on the long game—and the discipline to stick with it. In fact, it’s how our investment teams manage their portfolios.

How does it apply to you? Financial consultants Amy Alley, Rowland Pepito and Jennifer Simmons provide insight into why your long game is so important.

The American Century® Championship celebrity golf tournament raises money for medical research aimed at defeating life-threatening diseases. Each July, we welcome sports and entertainment celebrities who join compete for a cause that touches everyone.

Is Long-Term Investing Worth It?

Holding an investment over time is often cited as the most important strategy in investing, but it takes patience and discipline.

In golf, the long game gets you down the fairway. Investing follows a similar pattern—long-term discipline drives progress, while short-term decisions should support, not derail, that broader path. Focusing too much on day-to-day market movement can be like overthinking every putt instead of trusting your overall game plan.

“Let’s look at one of the world’s most famous investors, Warren Buffett,” says Rowland. Buffett reportedly bought his first stock at age 11 and has been investing for more than 80 years. His strategy of holding stocks for long periods has brought him success and made him a legend in the investment world.¹

Our future value calculator is a good way to see how a long-term investment can add up over 30 or 40 years.

Time is a huge factor for any investor and focusing too much on the short term can agitate you more than help—especially during volatile markets. “Investors often want quick results, but it could end up hurting their portfolio,” says Jennifer.

Plus, it can be hard to make up for lost time later, and some people try to catch up by adding riskier investments. “But that can add too much risk,” she says. “Why go 90 mph to your destination when you could start earlier and go 60 mph at a steadier, less risky pace? It’s all in the planning.”

What’s Wrong With Testing Out an Investment for a Short Time?

Testing a long-term investment for a short period will likely not give you a realistic picture of that investment’s future potential for your portfolio. It’s a bit like judging your golf game based on a single hole. A great drive or a bad putt doesn’t define your round—just as a few months of market performance don’t determine the value of a long-term strategy.

When you’ve been investing a while, you start to understand how powerful long-term investing can be—and you don’t sweat the day-to-day market activity.

“Some of my clients with the most money rarely look at their statements,” says Amy. “Those clients have removed their emotions from the equation. But it’s not always easy to look away. If it was, everyone would stay invested!”

Additionally, investors can feel more comfortable about their long-term strategy by understanding how compounding works. They are more confident riding out volatility and know the stock market’s history of performance over several years.

Does It Matter What I Invest In?

Yes. Long-term investing means seeking investments that are designed to grow. Stocks, in particular, are a main driver of portfolio growth over time.

“I see too many people investing for years in products that are better suited for short-term saving, like cash equivalents,” says Rowland. That’s not to say you don’t need short-term investments for short-term goals. It just shouldn’t be your only focus, especially when you have a goal like retirement.

Saving means putting aside money and seeking to preserve it by using accessible, low-risk accounts. Investing means accepting the risk inherent in investment markets to potentially grow your money over time.

Too much focus on short-term results can cause you to invest in a trend that may not play out or in a product that was never meant to be a long-term investment. For the latter, much of that could be because people don’t like risk. They’d rather play it in a way they perceive to be safer.

“When you focus on short-term volatility, it may put you in a position to take on too much risk or not take enough,” says Jennifer. Investing in short-term investments with a long-term approach doesn’t typically work. The short-term investment will likely not keep up with your growth needs, or with inflation, especially now. Yes, you may take on more risk with a stock fund, but with a long-term view of risk management, you have the luxury of time to help overcome downturns.

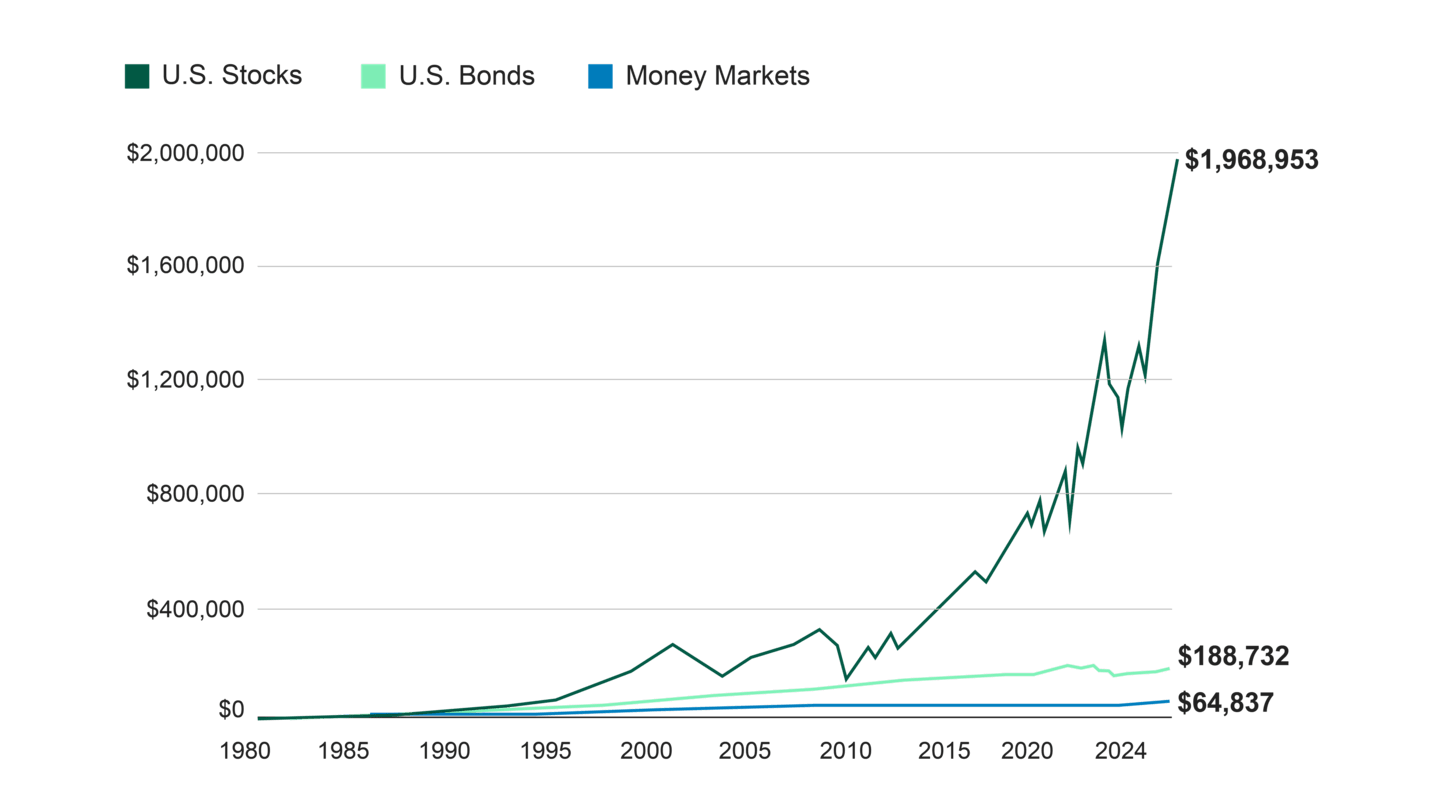

Historically, stocks have helped investors with growth. Bonds and cash equivalents, like money markets, have their place in a diversified portfolio but they may not help build the wealth most investors are looking for, as shown in the chart.

Stock Investments Have Historically Been the Main Driver of Growth

Hypothetical Growth of $10,000

Note that the hypothetical chart reflects a one-time investment of $10,000. Adding consistent investments over time would considerably change the results.

Source: American Century Investments, FactSet. Hypothetical value of $10,000 invested at the beginning of 1980 and ending September 30, 2025. Assumes reinvestment of income and no transaction costs or taxes. This is for illustrative purposes only and not indicative of any investment. An investment cannot be made directly into an index. Past performance is no guarantee of future results.

U.S. stocks are represented by the S&P 500® Index. U.S. bonds are represented by the Bloomberg U.S. Aggregate Bond Index. Treasury bills are represented by the FTSE 3-Month U.S. T Bill Index, which is often used as a benchmark for money market investments.

Keeping a Long-Term Focus: What Are the Hazards?

Competing financial priorities, current trends or events and even fear can also distract investors from their long-term goals. But understanding obstacles (and your own reactions to them) may help you avoid them on your own investing journey.

1. Emergencies

“One of the sand traps I see is not planning for emergencies,” says Amy. “When you don’t have an emergency fund, you could be tempted to dip into your long-term investments to cover the crisis at hand.”

2. Narrow Focus

Another hazard is being over-invested in a single stock or investment type, called concentration risk. You might enjoy short-term performance, but any change in the value can have an outsized impact on your portfolio.

When thinking about golf, you don’t take just one club to the course; it won’t meet all your needs or help you overcome the obstacles. Instead, you need a full set to play the game properly. It’s the same with investing—and it’s called diversification.

“Diversification can help your portfolio weather the market volatility many people want to avoid,” says Jennifer. “With a long-term portfolio, it’s not about focusing on that one stock. Instead, focus on your goals—all of them.”

3. Current Events

Another trap is recency bias—or overemphasizing recent market activity—good and bad. “If you’re just hearing about a hot investing trend on the news, you probably already missed the time to get in,” says Jennifer. “You have to think longer term.” She often tells clients to look at different time periods.

4. Fear of Risk

Still, Rowland says, one of the biggest obstacles may be negative investing behaviors, such as market timing or trying to avoid risk completely. “While helping clients overcome these behaviors is one of the biggest challenges, it’s also the thing that may move the needle and help them the most.”

Understanding your values about money may help you overcome the obstacles in your way. We all have a history with money, whether from our parents or on our own, so it’s important to understand yourself. Talking to a financial professional is a good way to see where you may be able to avoid any sand traps along the way.

How Do Other Investors Manage a Long-Term Strategy?

Long-term investors make a choice: to invest and then see what it can do for them. Seasoned golfers know that improvement doesn’t come from one perfect round; it’s built over time through steady practice and commitment. Investors who succeed long term often take the same approach, trusting the process and letting consistency—not quick wins—drive results.

And while past performance is no guarantee of future results, our financial consultants have seen the diligence and commitment of a long-term approach work.

Rowland tells about a client who received an investment gift from her father in 1990. “He told her to invest whatever she could monthly. She decided to put away $1,000 a month and did so faithfully.” If she was between jobs, she’d bartend so she wouldn’t miss a month.

The goal was to use time in the market, compounding returns and additional contributions to build up her balance to where it is today.

Amy has a client who started an investment 40 years ago with $10,000. Over the years, she put in a sum here and there and never touched it. Not once, through all the market's ups and downs.

“She started with smaller chunks and let it ride,” says Amy. “But it doesn’t have to be $10,000. People don’t think $25 a week can go anywhere, but they may be surprised how it can add up.” Setting up an automatic monthly investment plan is a great way to stay committed to long-term goals.

For every story we have about clients who’ve succeeded as long-term investors, there are those who learned the hard way that a short-term approach doesn't work. Many are the result of market downturns that have caused people to fear the swings.

Many investors were scared during the 2008 financial crisis and made snap decisions about their investments. That short-term perspective can often lead to bad decisions that can cost you in penalties, taxes and a smaller nest egg.

We’re Here to Help

If you’re tempted to make decisions based on short-term market activity, our financial consultants say, call a financial professional first. Working with a professional can provide perspective—helping you stay focused on your long-term goals while making thoughtful short-term decisions along the way.

“We’re here to help you make the best decision for your long term and avoid knee-jerk reactions,” says Jennifer. “Being reactive rather than proactive can be a real cost to you in terms of your goals—fewer vacations or more years until you can retire. A long-term approach is a game plan for your finances and can help you ride out bad markets. Investing can feel much scarier without it.”

Authors

Financial Consultant

Financial Consultant

Financial Consultant

Need Help With a Long-Term Strategy?

A financial plan can get you on the right path. Consider a few sessions with one of our Certified Financial Planners to create or revisit your plan.

“Who Is Warren Buffett? How Did He Make His Fortune?” Investopedia, January 29, 2026.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

Diversification does not assure a profit nor does it protect against loss of principal.

American Century's advisory services are provided by American Century Investments Private Client Group, Inc., a registered investment advisor. These advisory services provide discretionary investment management for a fee. The amount of the fee and how it is charged depend on the advisory service you select. American Century’s financial consultants do not receive a portion or a range of the advisory fee paid. Contact us to learn more about the different advisory services. All investing involves the risk of losing money.