High Interest Rates, Low Jobless Rate: Ordinary or Anomaly?

Market Minute | History suggests this seemingly odd dynamic is not unusual, but likely won't last and may precede potential market opportunities for bond investors.

Key Takeaways

It may seem contradictory, but the unemployment rate historically has improved or remained stable during Federal Reserve (Fed) rate-hike cycles.

Over time, though, higher interest rates have led to rising unemployment, a slowing economy and falling bond yields.

If history repeats, we believe bond investors have an opportunity to capture attractive return potential before the full effects of Fed policy unfold.

Market Minute: High Interest Rates, Low Jobless Rate: Ordinary or Anomaly?

We've Been Here Before

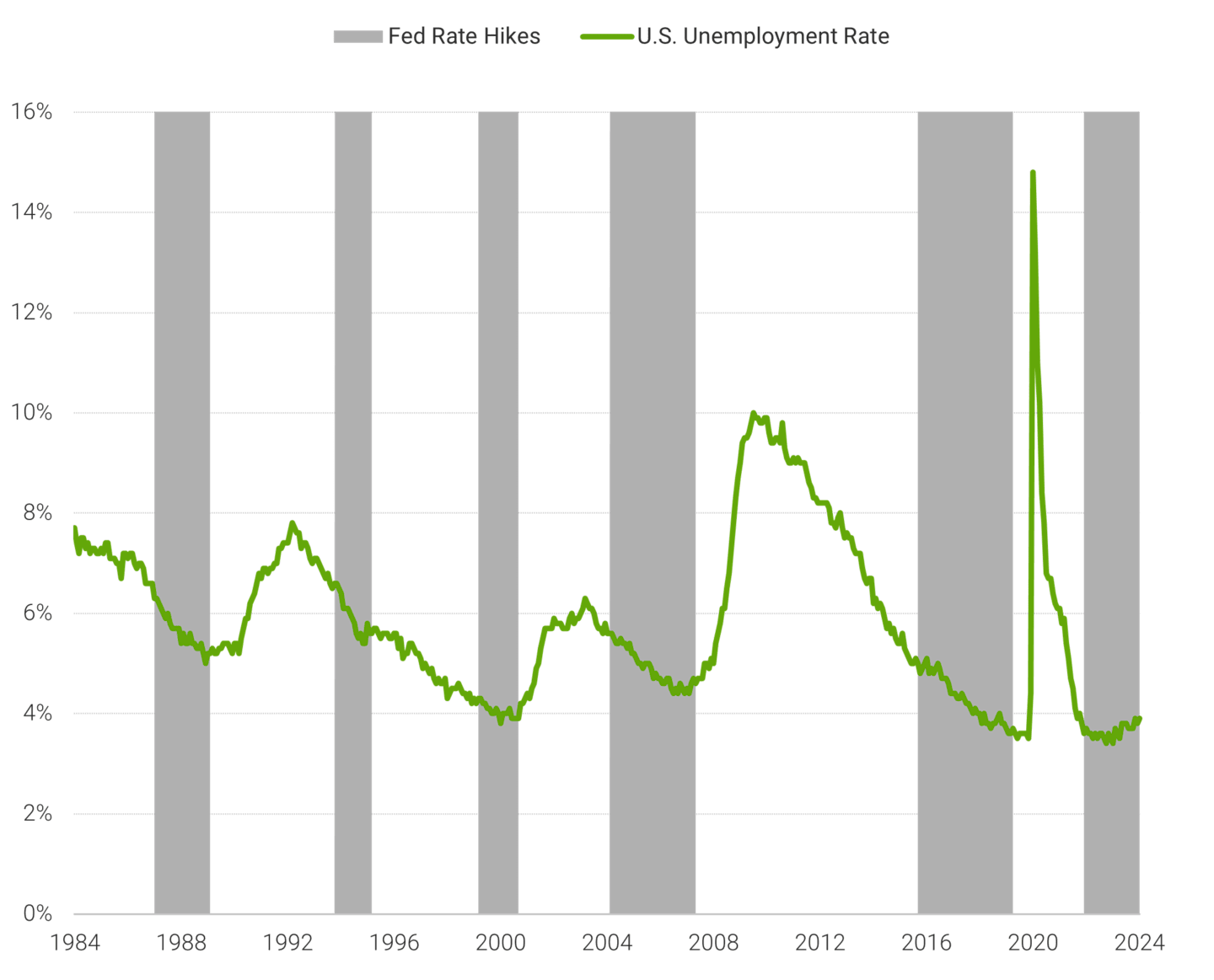

Some claim that today’s low jobless rate is unprecedented, given the Fed’s short-term interest rate target is sitting at a 23-year high. But history disagrees.

The trajectory of the unemployment rate during Fed rate-hike cycles reveals some common characteristics.

As the chart highlights, the unemployment rate declined during prior rate-hike cycles and has changed little during the latest phase.

But following most rate-hike cycles since the 1980s, unemployment generally rose until a slowing economy triggered a downturn.

Unemployment Rate Has Cycled with Fed Rate Hikes

Data from 4/30/1984 – 5/15/2024. Source: FactSet.

Today's Job Market Tracks History

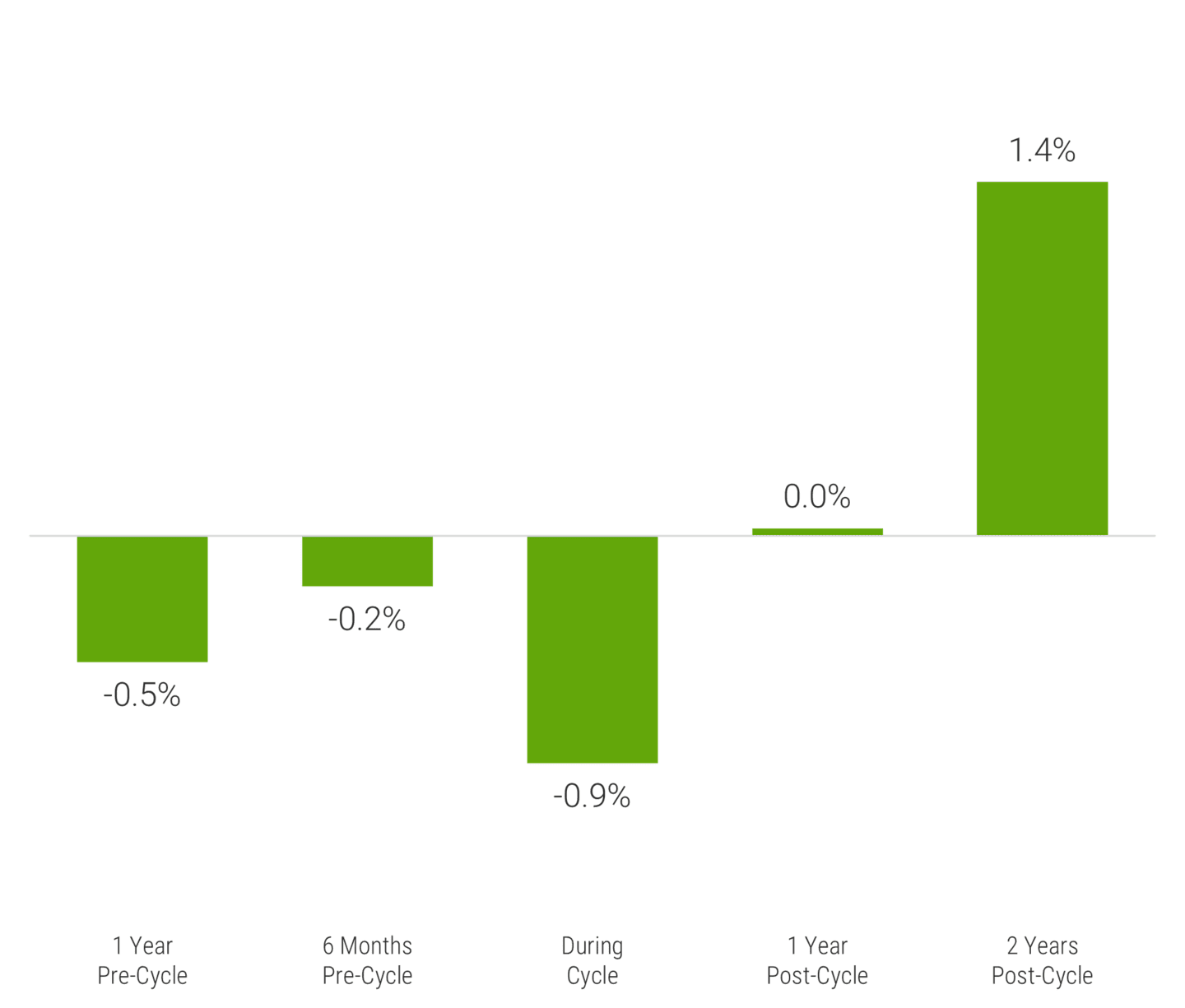

Unemployment Fell When Fed Raised Rates, Increased Two Years Later

Average Percentage Point Change in Unemployment Rate, Last Four Rate-Hike Cycles

Source: Macrobond. Fed rate-hike cycles: 2/4/1994 – 2/1/1995; 6/30/1999 – 5/16/2000; 6/30/2004 – 6/29/2006; 12/17/2015 – 12/20/2018.

None of the Fed rate hike cycles of the past 40 years triggered a rapid rise in unemployment. In fact, during the last four rate-hike cycles, the unemployment rate improved by nearly 1 percentage point.

What happened after the Fed stopped hiking rates?

Initially, not much. In prior cycles, unemployment was stable one year after Fed tightening ended. But by the second year, the unemployment rate was notably higher.

Recent trends are tracking history. The last rate hike was in July 2023, when the jobless rate was 3.5%. It reached 4% by May 2024.1

We expect the lagging effects of Fed rate hikes to meaningfully affect unemployment by next summer.

Hiring Slowdown Supports Our View

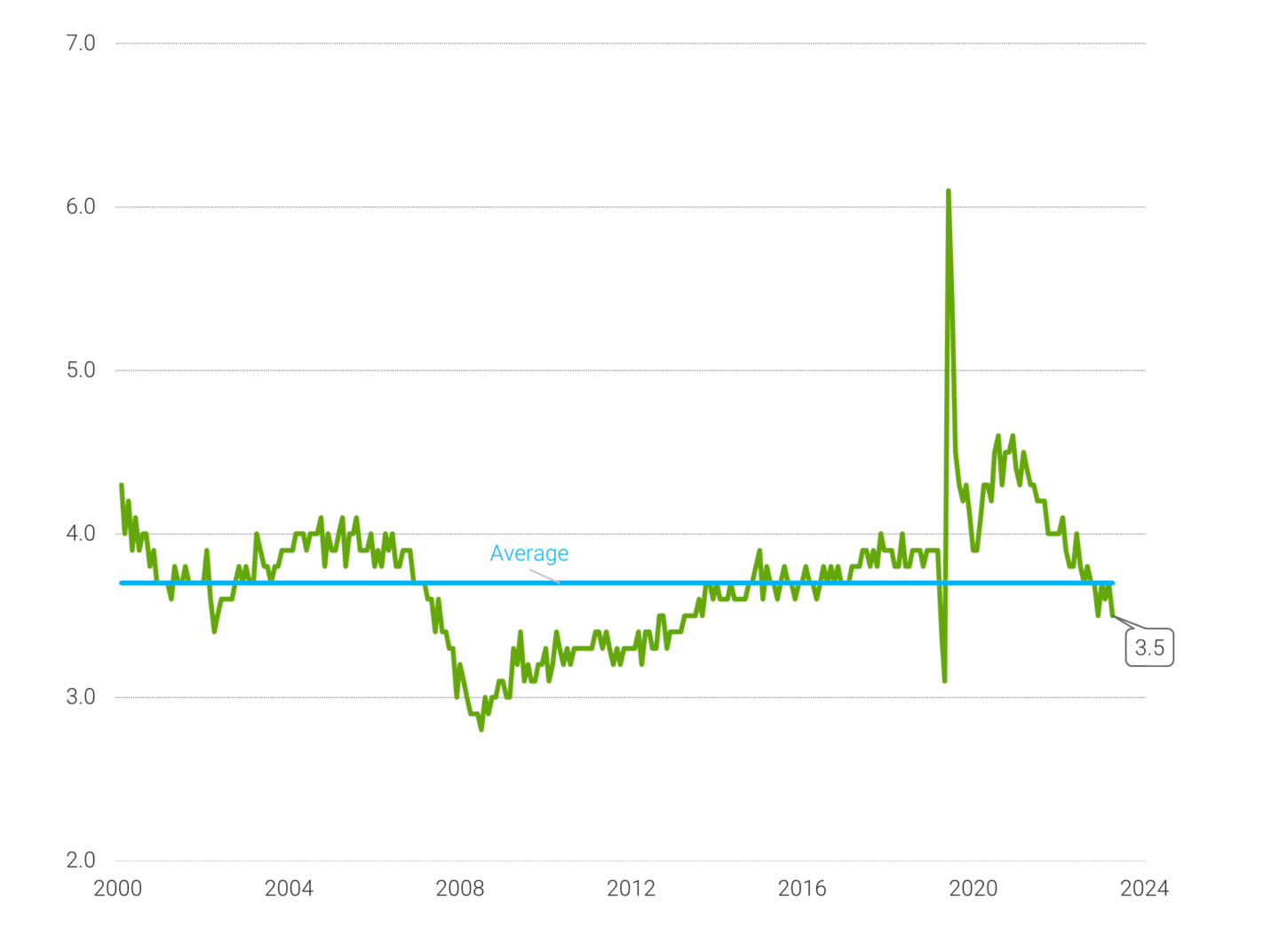

In addition to the jobless rate’s historical patterns, current hiring trends support our outlook for unemployment to rise.

The pace of hiring has been on a steady downward path for more than two years. The hiring rate landed at 3.5% at the end of March, below the 21st century average of 3.7%.

The Pace of Hiring Has Been Declining

Hiring Rate (%)

Data from 12/31/2000 – 3/31/2024. Source: U.S. Bureau of Labor Statistics. Hiring rate = non-farm hires/labor force.

Learning From the Past

We expect history to repeat, or at least rhyme, over the next several months.

In our view, the cumulative effects of the Fed’s latest tightening cycle will weigh on employment and the broader economy.

We believe this scenario should push bond yields lower, generating attractive total return potential for bond investors.

The past does not repeat itself, but it rhymes.

Opportunities for Bond Investors

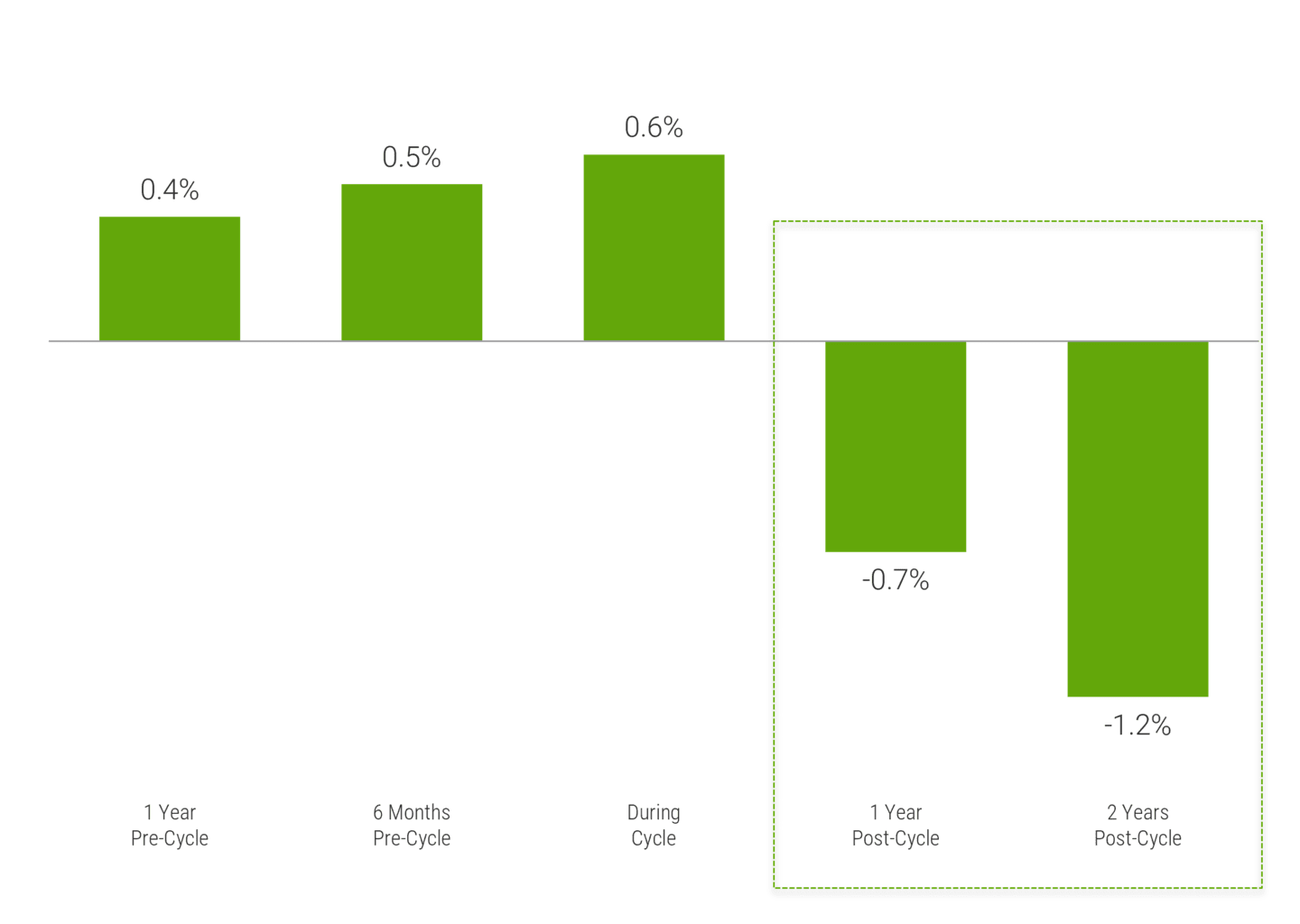

Yields Declined After Fed Ended Rate-Hike Campaigns

Average Percentage Point Change in 10-Year Treasury Yield, Last Four Rate-Hike Cycles

Source: Macrobond. Fed rate-hike cycles: 2/4/1994 – 2/1/1995; 6/30/1999 – 5/16/2000; 6/30/2004 – 6/29/2006; 12/17/2015 – 12/20/2018.

Looking again to the previous four Fed tightening cycles, bond yields generally declined in the two-year period after the Fed stopped raising rates.

By the two-year mark, the yield on the 10-year U.S. Treasury note dropped an average of 1.2 percentage points.

And when bond yields decline, bond prices typically rise.

These trends drive our preference for investing in high-quality, longer-duration bonds ahead of a broad shift in yields.

Authors

Check Out More of Our Market Minute Articles

Investment insights for savvy investors.

Source: U.S. Bureau of Labor Statistics

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.