The Investor Life Cycle: Where Are You?

An investor’s financial goals and risk profiles change over time. We often divide wealth accumulation into four phases, from early accumulation to living in retirement.

Key Takeaways

Your financial goals and risk tolerance will likely evolve over time, which will require regular reviews and adjustments of your investment strategy.

Planning for major milestones, such as homeownership, education and retirement, might look different depending on your age.

Personalized financial guidance can help you navigate each stage of your journey and make informed decisions to support your changing needs.

Your goals for money depend highly on your age and time to retirement.

Early on, you want your earnings and investments to grow. You want to jump-start your retirement plans and potentially save for a house. Once you retire, you may want to play it a little safer and focus on having your investments last for the remainder of your life.

As you move through the four stages of your investor life cycle, your goals change, and your investment plan should also change to reflect where you are.

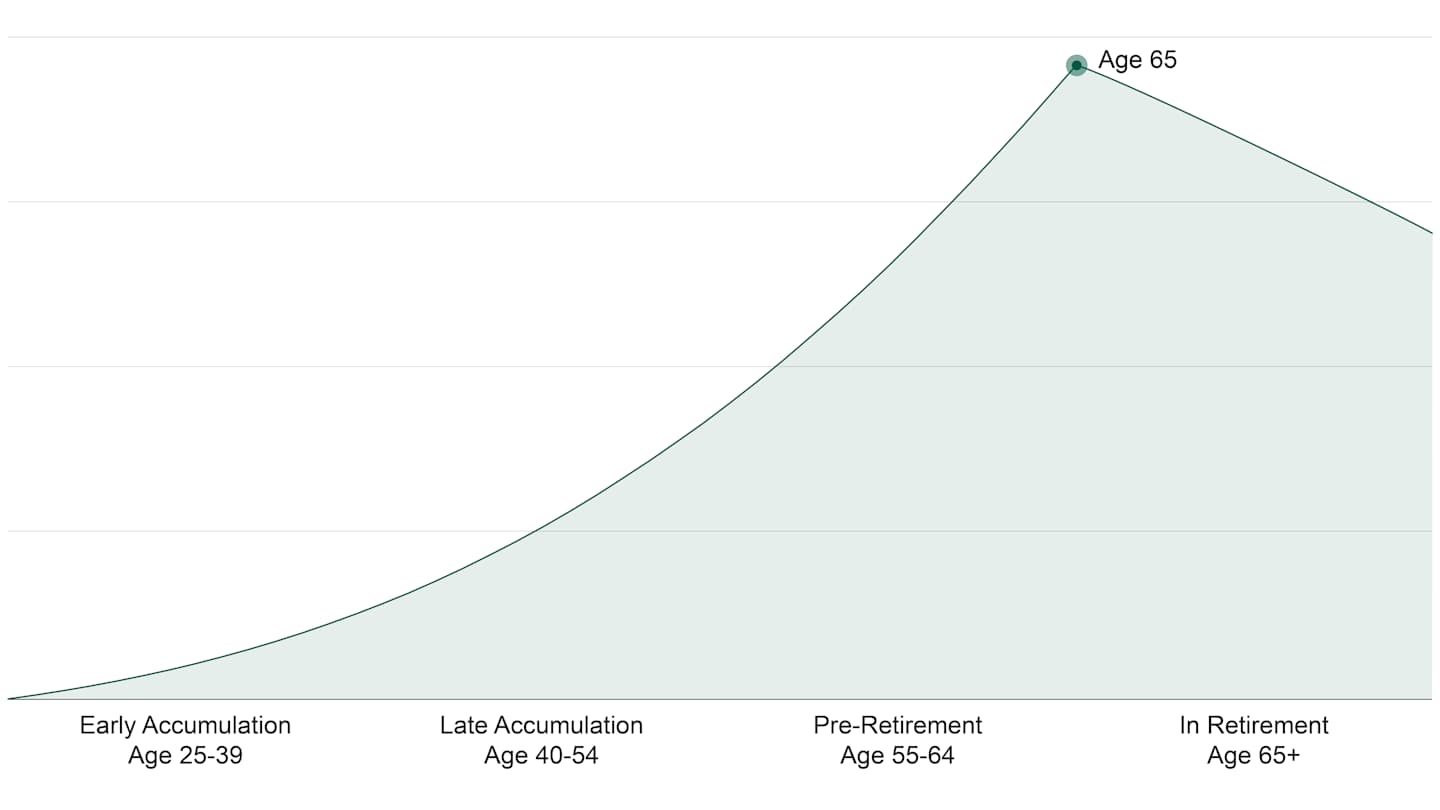

The Investor Life Cycle

Hypothetical Asset Accumulation Over Time

Source: American Century Investments. The illustration demonstrates how investors may have different needs or considerations as they age and as their assets grow.

Let's go over each stage and meet investors seeking guidance relevant to where they are on their paths. See if any of their stories resonate as you create your financial road map.

Choose Your Life Stage

Early Accumulation You’re just starting your career and have more time to add to your investments.

Late Accumulation You may be in your peak earning years at work and are continuing to build wealth.

Pre-Retirement You’re counting down to your last paycheck and making preparations for retirement.

In Retirement You’ve put your plan into action and want to make your money last.

Early Accumulation: Establish Good Investing Habits

The first stage of the investor life cycle is the early accumulation phase. Early accumulators are typically 25 to 39 years old and just starting their careers.

Time is on their side, so these investors can generally take on more risk with investments. If they experience market declines, they have the most time to potentially make up those losses by working, increasing their income and investing.

Early accumulation goals:

Make a budget and track cash flow.

Establish emergency savings.

Create a financial plan, and consider how to manage debt.

Save for children's education.

Save for retirement with a tax-advantaged retirement plan.

Meet Erika

Erika graduated a few years ago and just received a promotion at work. She finally feels like she's making some “real money.” Even so, she’s a bit overwhelmed. Should she pay off her student debt before investing, she wonders? But she wants to save for a house too.

Erika engaged a financial advisor to help her sort through her goals for her first financial plan. Together, they decided how she would pay down debt and save for an emergency and a house.

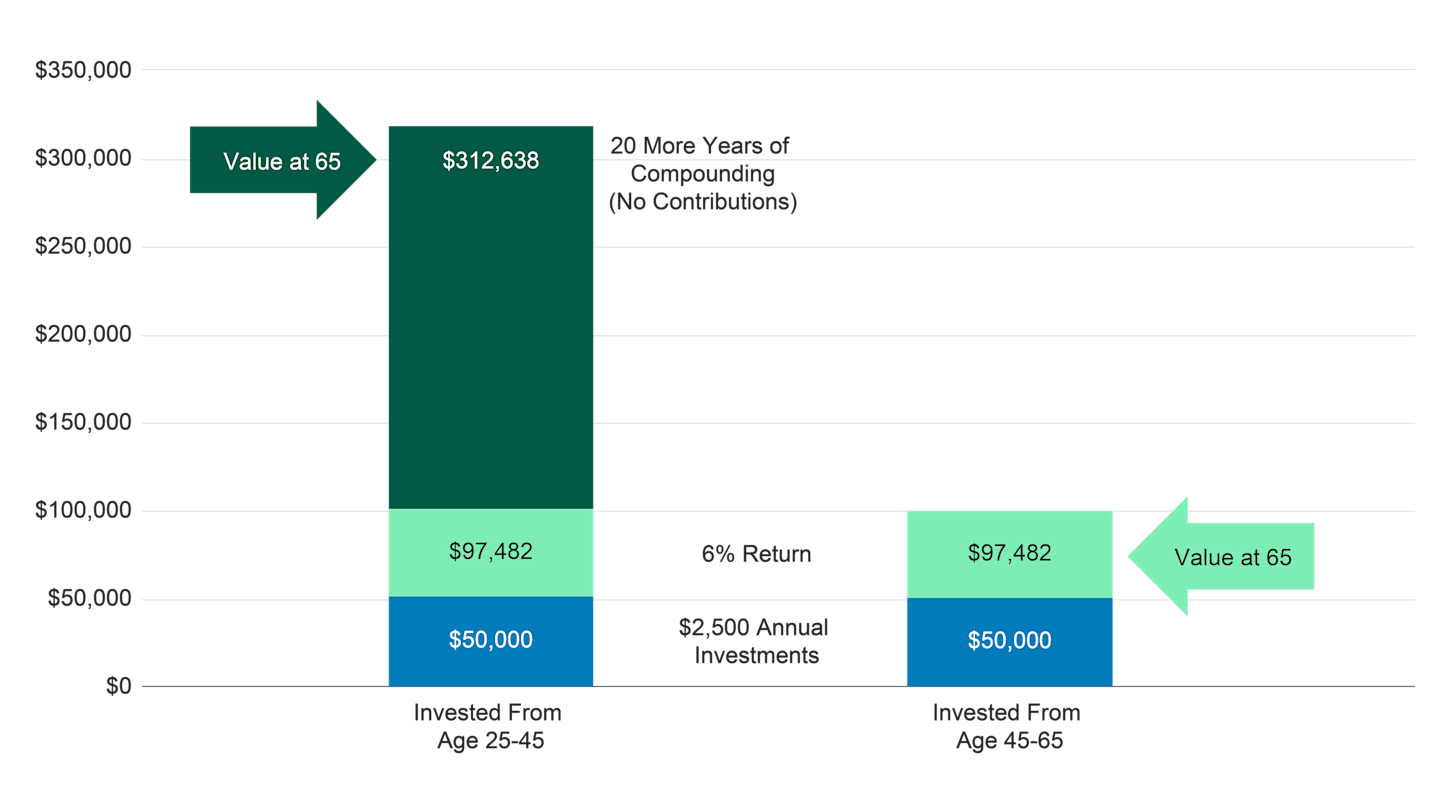

Being in the first financial stage, Erika benefits the most from compounding interest on her investments. If she invests for 20 years starting at age 25 versus starting at age 45, she has the potential to earn three times as much by the time she’s 65. The additional years of compounding make all the difference. (While compounding can lead to exponential growth with positive returns, negative returns can also erode capital over time.)

The Benefits of Starting Early

Source: American Century Investments, Investment Rate of Return Calculator. The hypothetical calculation assumes an annual contribution of $2,500, earning a rate of 6% annually over 20 years, plus an additional 20 years at 6% with no additional contributions. It assumes reinvestment of all realized gains, dividends, and interest receipts and does not account for the effects of any added fees, expenses, or taxes that might be incurred. If all taxes, fees, and expenses were reflected, reported portfolio values would be lower. This hypothetical situation contains assumptions that are intended for illustrative purposes only and are not representative of the performance of any security. There is no assurance similar results can be achieved, and this information should not be relied upon as a specific recommendation to buy or sell securities.

Financial Calculators from Dinkytown.net

Financial Calculators ©1998–2025 KJE Computer Solutions, LLC

It's no guarantee, but starting early may allow Erika to build a solid foundation for her wealth and future retirement.

Erika feels good that she's now on a path to investing for all her goals.

Late Accumulation Stage: Make Use of Peak Earnings

The second stage of the financial life cycle is the late accumulation phase. Late accumulators are generally ages 40 to 54 and are in their peak earning years at work.

Many have lived through a recession or two and understand the need to keep building wealth to protect against life’s uncertainties. These investors are generally still investing for growth but may move toward more of a balanced approach between stocks, bonds, real estate, etc., as they age.

Late accumulation goals:

Fund children’s education.

Balance debt payments and retirement goals.

Max out tax-advantaged retirement accounts.

Grow non-retirement wealth.

Meet Lainey

Lainey is a busy business owner in her mid-40s. Since her divorce, Lainey now finds herself in charge of her finances. She wants to make sure she can afford to send her two kids, ages 8 and 10, to college but can't ignore the fact that she must consider her retirement. Lainey is looking for someone to help her reestablish goals for her new life.

Lainey found a financial advisor who will work with her, meeting Lainey at her business and according to her availability. The advisor first helped Lainey understand what divorce meant for her finances and what her assets and liabilities look like now.

Regarding retirement, Lainey is nervous that she’s “behind.” Still, there are plenty of opportunities for her to catch up. The advisor helped her review her budget and find ways to make more tax-deferred elections toward retirement. In several years, when she turns 50, she can begin making catch-up contributions to her IRA. Lainey also felt better after seeing the various options for paying for college.

Lainey is relieved to have a plan that is mindful of her and her kids’ needs. She and her advisor scheduled a follow-up meeting to check in and see how the new budget and plan are going.

Pre-retirement Phase: Focus on Planning

The pre-retirement stage occurs during the years before retirement. Household expenses are stable, children are self-sufficient or are beginning to be self-sufficient, and the investor's savings rate is the highest.

Investments will generally shift toward higher percentage allocations of lower-risk assets—like investment-grade bonds—with the objective of preserving wealth and creating income.

Pre-retirement goals:

Prepare for your retirement transition.

Make catch-up contributions in retirement accounts.

Max out your 401(k) or other retirement plan.

Work on your estate plan.

Meet Pete

Pete is an empty nester and in pre-retirement. The countdown is on for him and his wife as they dream about their upcoming retirement. He has retirement accounts but wants a financial quarterback to help ensure their nest egg lasts through retirement.

Pete’s advisor walks him through a retirement readiness exercise. Together, they discuss Pete’s income sources and likely expenses in retirement. The math will help him as he and his advisor develop a retirement income plan, an insurance plan, a tax plan and an estate plan. Being prepared with a financial picture of retirement will help Pete determine retirement timing and how much he may want to leave to his children.

Retirement: Make Your Money Last

In the fourth stage of the financial life cycle, individuals may stop earning active income and depend on Social Security, investment earnings and savings.

Assets may be invested conservatively—with a mix of dividend stocks and bonds—to seek to preserve the investor’s nest egg while allowing for growth and income.

Goals in retirement:

Create an income strategy.

Cover medical expenses.

Finalize your estate plan and share it with family.

Meet Roger

Roger enjoys an active retirement with his wife. They live in Florida but love traveling and visiting family in the Northeast. Roger is a do-it-yourselfer when it comes to investments. Still, given the recent losses he's experienced in the turbulent market, he’s feeling unsettled that his nest egg won’t last. He wants an expert set of eyes as he navigates through retirement, trying to ensure that his money lasts.

Roger finds an advisor happy to help him revisit his financials. The advisor thinks Roger would greatly benefit from employing a retirement income strategy that adjusts spending—and withdrawals—when the market experiences losses.

Roger feels better that he has a plan to adjust to challenging markets. He’ll meet with the advisor again next year to check in.

Putting It Together

Did you recognize elements of yourself and your situation in any of these hypothetical investors?

Early-accumulation Erika needed guidance organizing her first wealth plan. Late-accumulation Lainey received help with her new circumstances and kids’ college planning. Pre-retirement Pete has done a fine job building wealth but needed a game plan for when and how to retire. And Retired Roger is working on budgeting and withdrawal strategies to find a way to make his retirement savings last through a down market.

With a bit of help, all of these investors now have plans well positioned to pursue the goals in their financial life cycle stages. Are your finances positioned for where you are—and where you want to go—on your journey?

Get Help From a Consultant

Our Investment Consultants are available to help guide you through retirement planning, now and when you make the transition.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

Diversification does not assure a profit nor does it protect against loss of principal.

You could lose money by investing in a mutual fund, even if through your employer's plan or an IRA. An investment in a mutual fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.