Why Higher Risk Doesn’t Always Mean Higher Returns

A low-volatility portfolio has the potential to outperform while exposing investors to less risk.

Key Takeaways

Though many investors believe they should take a high-risk approach to generate higher returns, academic research shows that’s not necessarily true.

Simple math provides a compelling argument against a high-risk strategy: The farther an investment falls, the steeper its climb to break even.

Low-volatility portfolios have the potential to advance in rising markets and may provide a buffer during declines.

Conventional investment wisdom says there is a direct relationship between risk and return. In other words, you must be willing to accept more risk to receive a greater reward. But is that true?

Not necessarily. Academic research demonstrates that low-risk stocks have historically delivered higher returns than high-risk stocks. This observation is known as the “low-volatility anomaly.”¹

How the Low-Volatility Anomaly Defies Conventional Wisdom

Historical data indicates low-risk stocks have outperformed high-risk stocks on a risk-adjusted basis over time.² Risk-adjusted simply refers to an investment’s gain or loss relative to its risk. So, if two stocks perform the same during a given period, the one with lower risk has a better risk-adjusted return.

This isn’t a new concept. In 1972, economists Robert Haugen and James Heins provided evidence of the low-volatility anomaly. Based on data from 1926 to 1971, they concluded that “over the long run stock portfolios with lesser variance [volatility] in monthly returns have experienced greater average returns than their ‘riskier’ counterparts.”³

Numerous other studies of U.S. and international stock markets have come to similar conclusions.

Can You Win by Not Losing?

Suppose you invested $1,000 and it grew by $100 in Year 1. If you reinvested your $100 gain, you would begin Year 2 with $1,100. You would have the potential to gain (or lose) from this higher base. This is what we mean by compounding, and it helps illustrate why compounding can be an investor’s best friend.

Of course, it’s possible to lose money when investing. And large losses diminish the power of compounding. That’s because a volatile investment’s outperformance when the market is rising can be offset by significant underperformance when the market is declining.

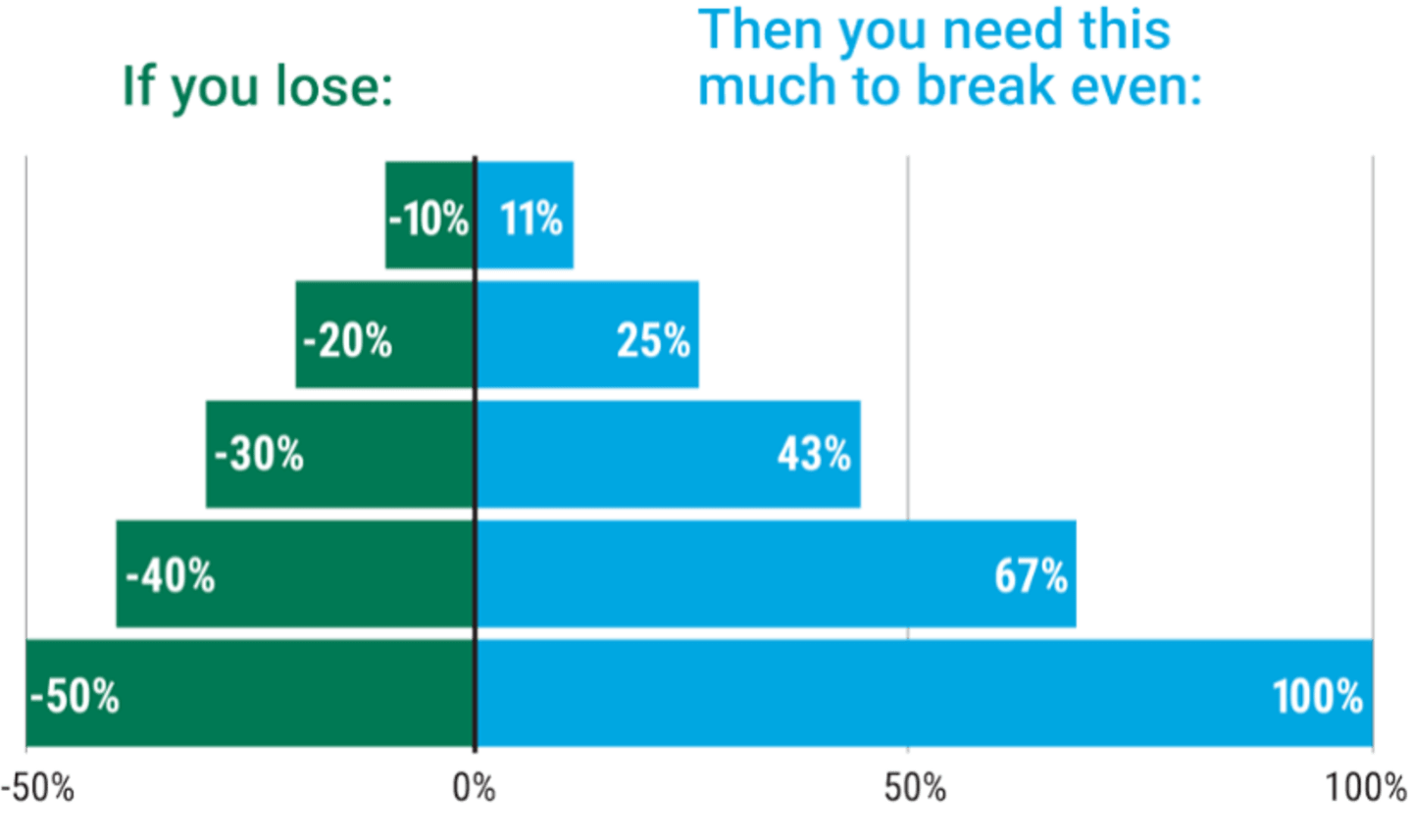

You can see the cruel math behind this in Figure 1. The more a stock or portfolio falls, the more it must gain to get back to even. Therefore, it’s best to try to avoid large losses because they are hard to recoup.

Figure 1 | The Cruel Math of Losses

Source: American Century Investments.

Past performance is no guarantee of future results. Investment returns will fluctuate and it is possible to lose money.

This hypothetical situation contains assumptions that are intended for illustrative purposes only and are not representative of the performance of any security. There is no assurance similar results can be achieved, and this information should not be relied upon as a specific recommendation to buy or sell securities.

Seek a Smoother Ride

We believe investors may experience less volatility and improved returns by managing risk at the portfolio level. A low-volatility portfolio can potentially keep pace with rising markets and offer a buffer during declines and severe market drawdowns.

Authors

Senior Client Portfolio Manager

Explore More Insights

Read our latest articles and market perspectives.

Robert Haugen and James Heins, “On the Evidence Supporting the Existence of Risk Premiums in the Capital Market,” December 1, 1972.

High- and low-risk stocks were identified by using the Sharpe Ratio to evaluate Russell 1000 Index data from 1/1/1993 – 3/31/2021

Haugen and Heins.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

Non-FDIC Insured | May Lose Value | No Bank Guarantee