The Retirement Conversation Is Changing

Our 11th Annual Retirement Survey

In American Century’s 11th annual national survey of retirement plan participants and sponsors, we found heightened interest in protecting savings from market volatility and converting those savings into reliable income. How does that change the focus your sponsor clients have for their plans?

Equally important, how do retirement advisors change the conversation to help sponsors rethink their goals? The survey results can inform client discussions—our representatives can help, too.

Let Us Help You Change the Conversation About Plan Goals

Review Full Survey Findings

2024 Participant Survey

2024 Plan Sponsor Survey

Asset Protection and Retirement Income: Rethinking Plan Goals

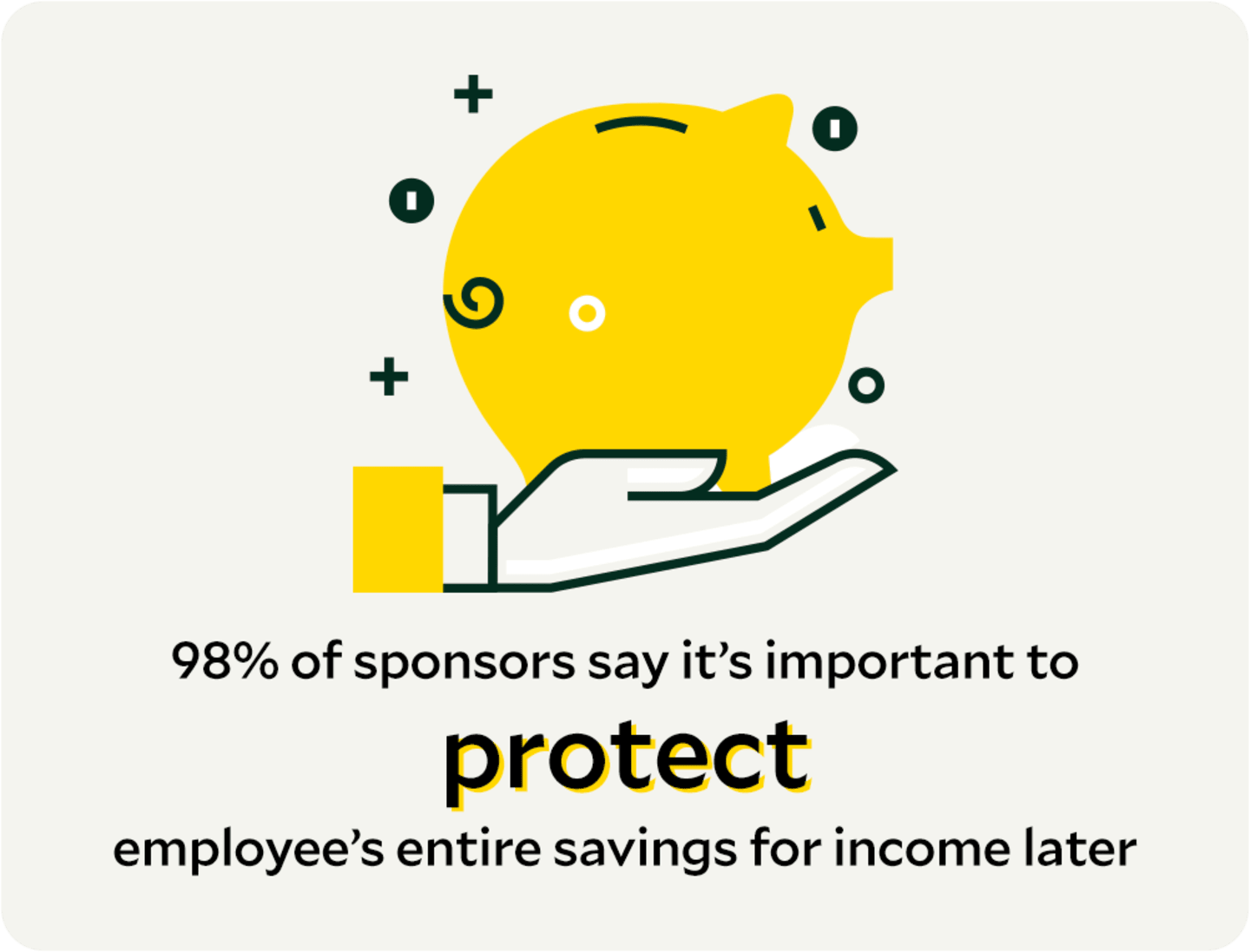

Plan sponsors and participants believe asset protection and giving participants control and flexibility with their accounts after retirement are crucial. Both may need education on income options, participants may need to better understand TDFs. Here’s what sponsors and participants said.

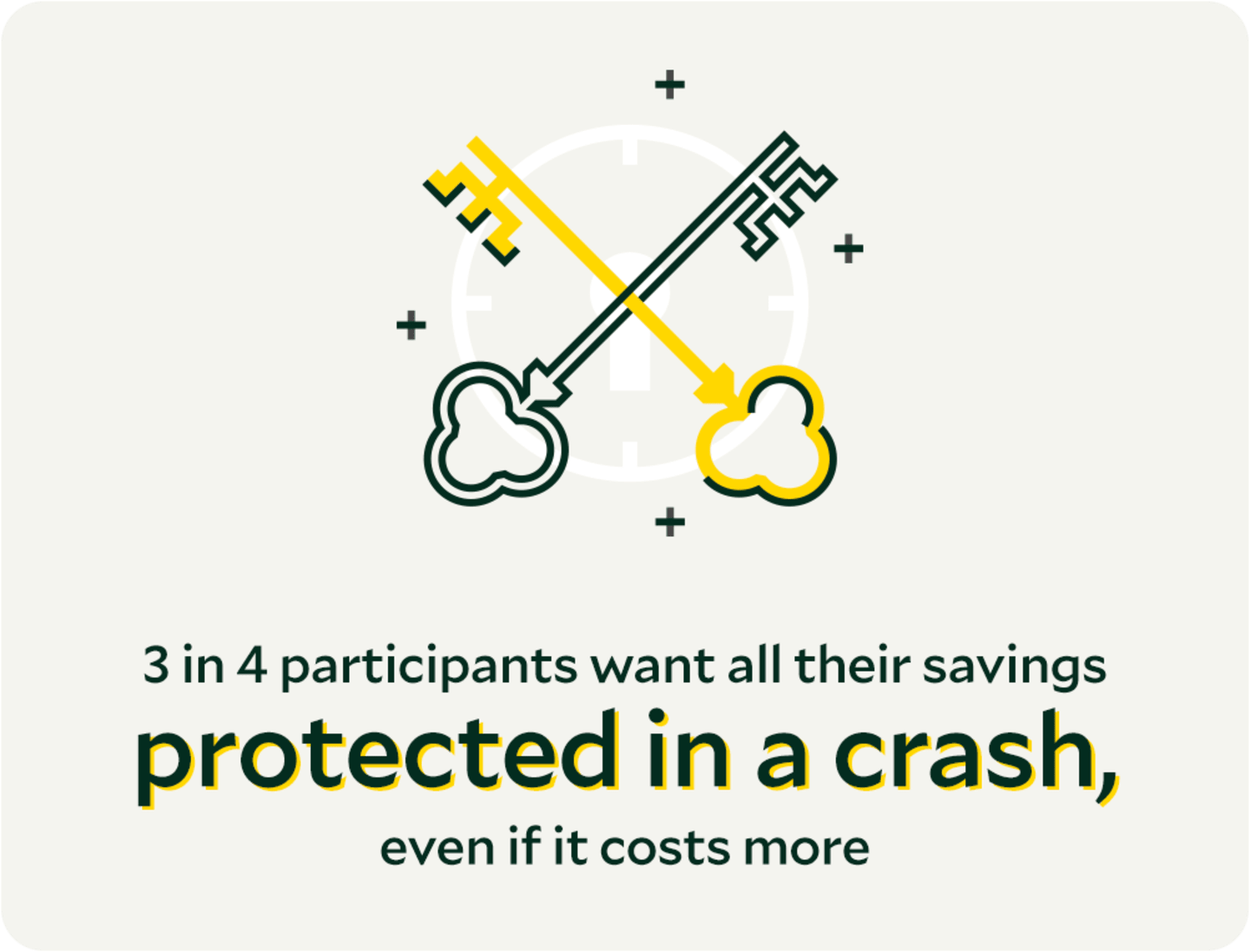

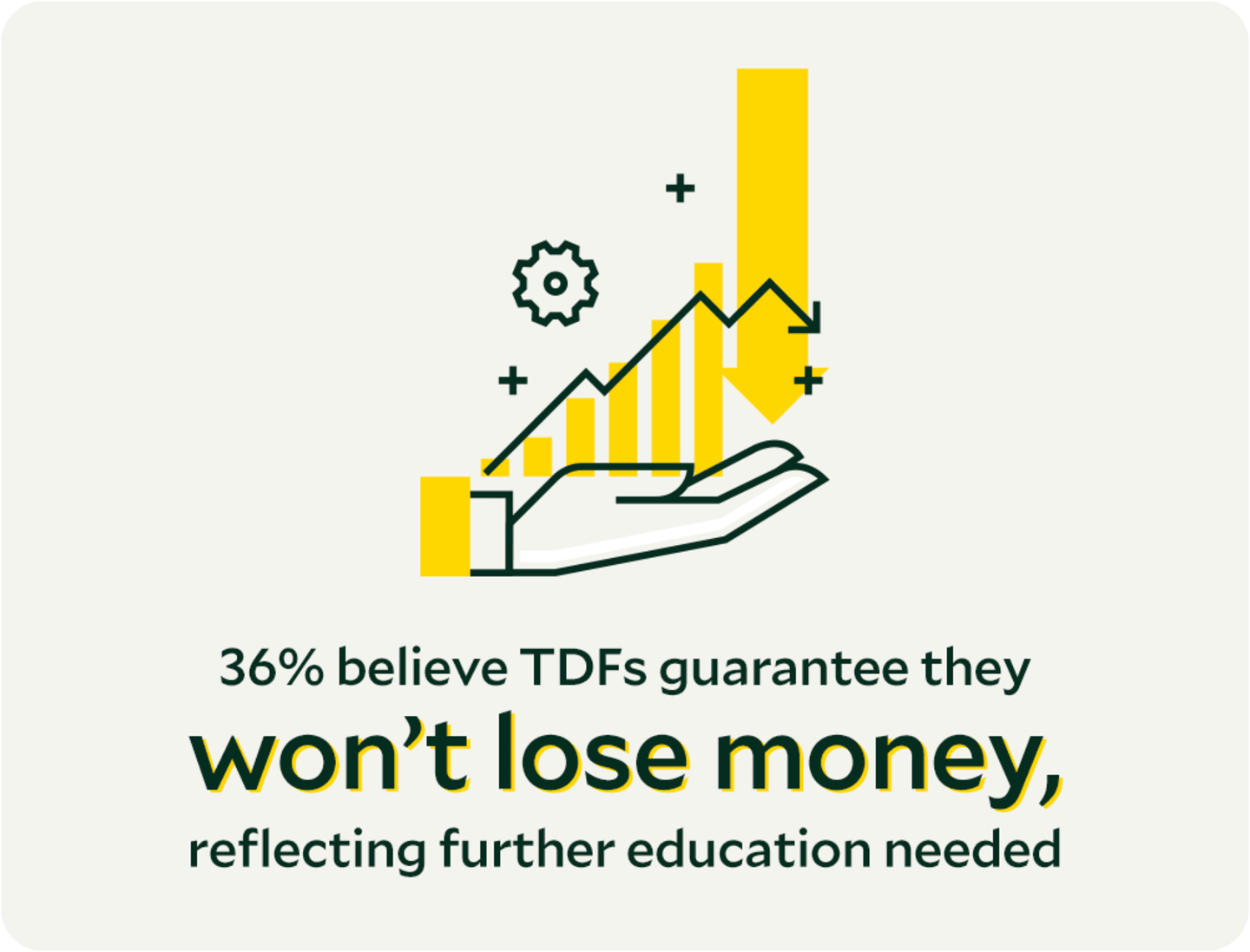

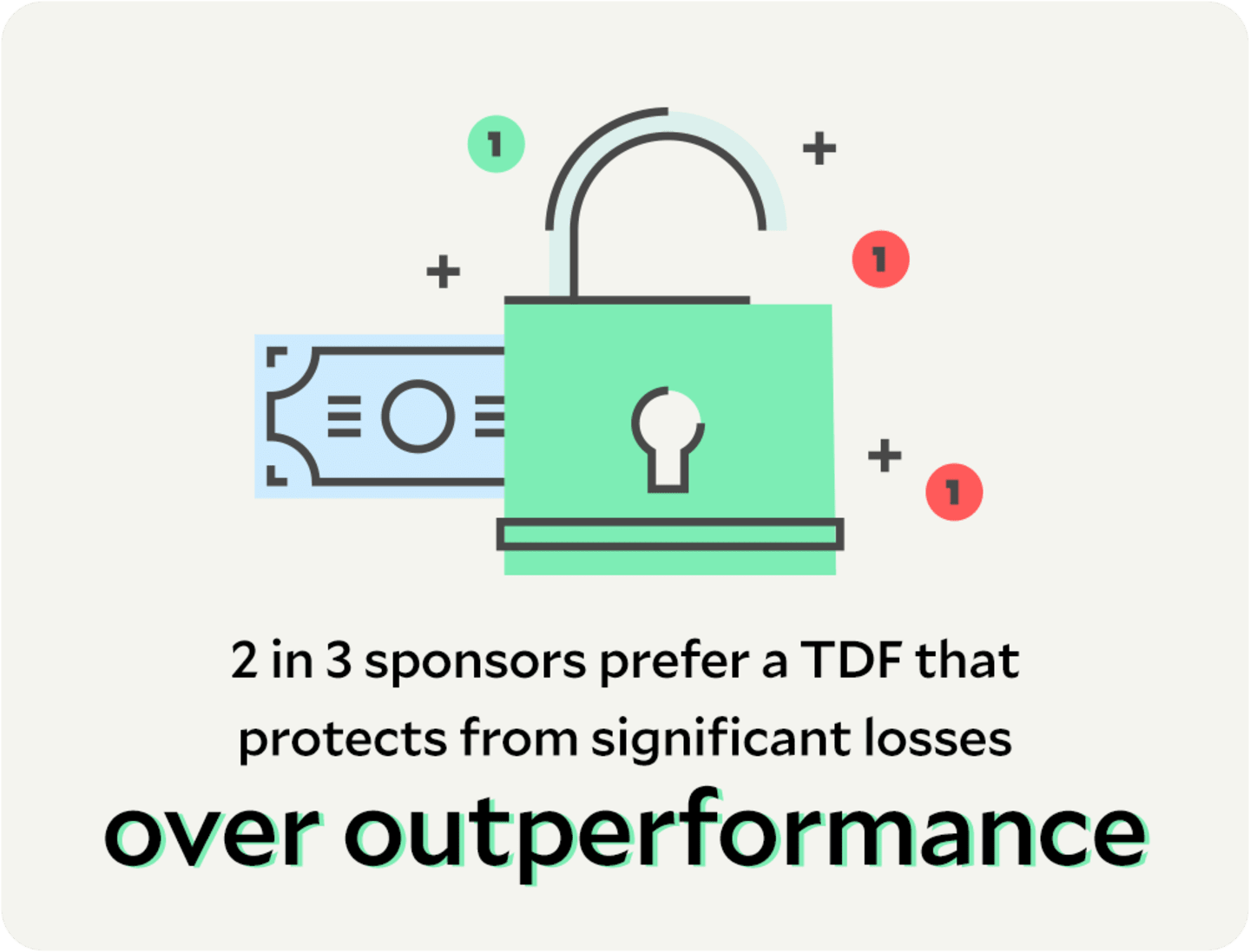

Protect Assets

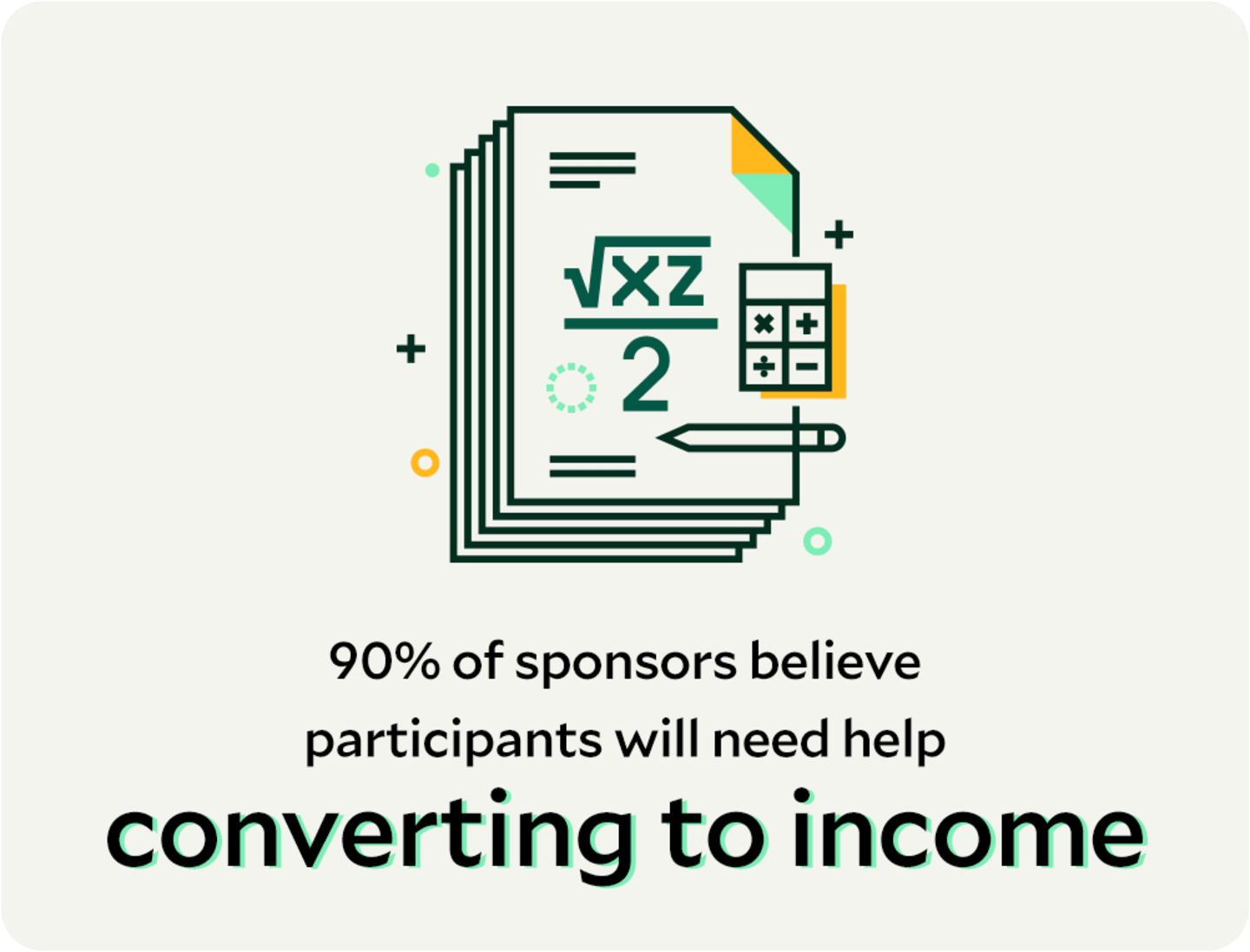

Most participants say it is important to protect their savings from market volatility, but they may misunderstand how to do that—including how a target-date fund (TDF) works.

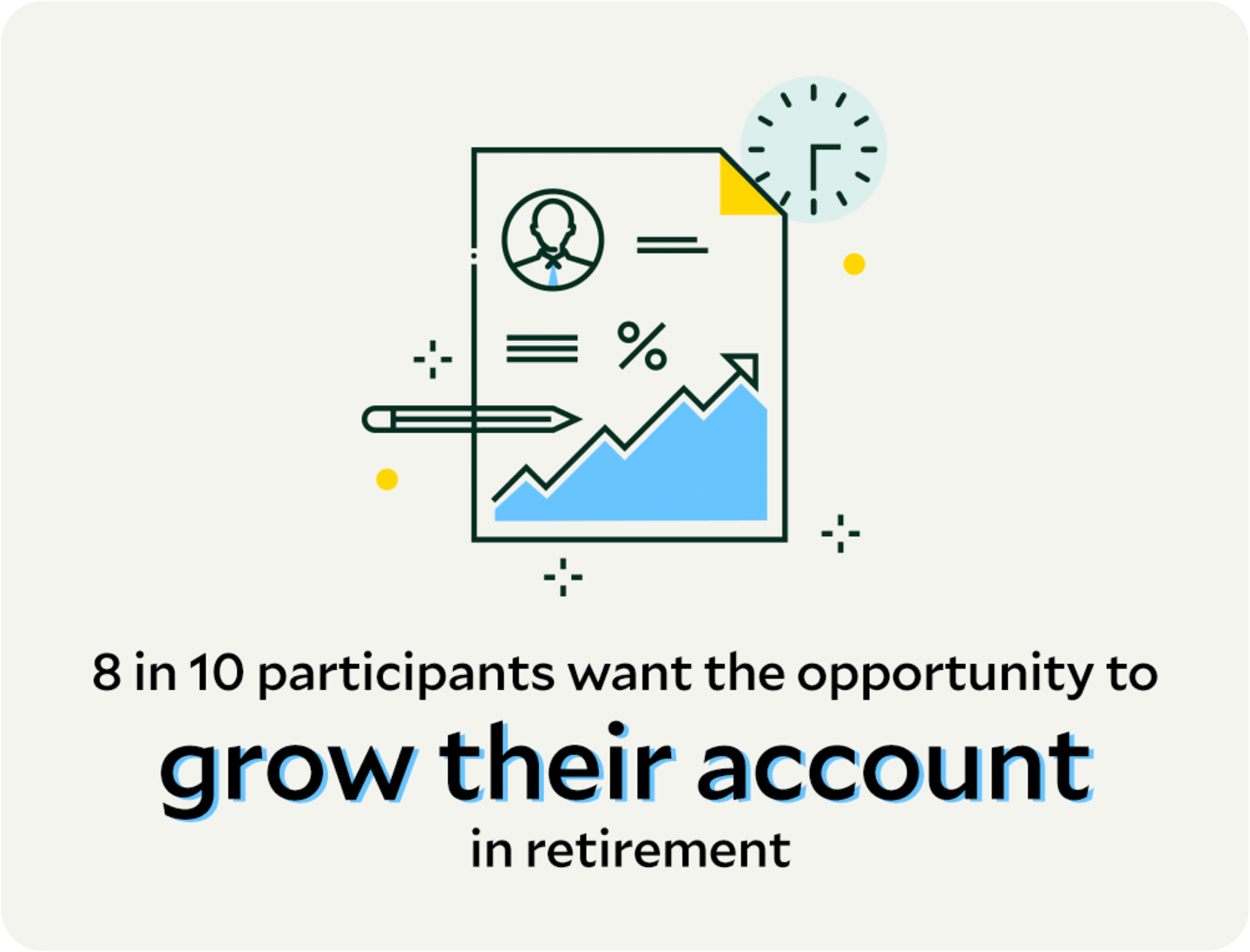

Grow Savings in Retirement

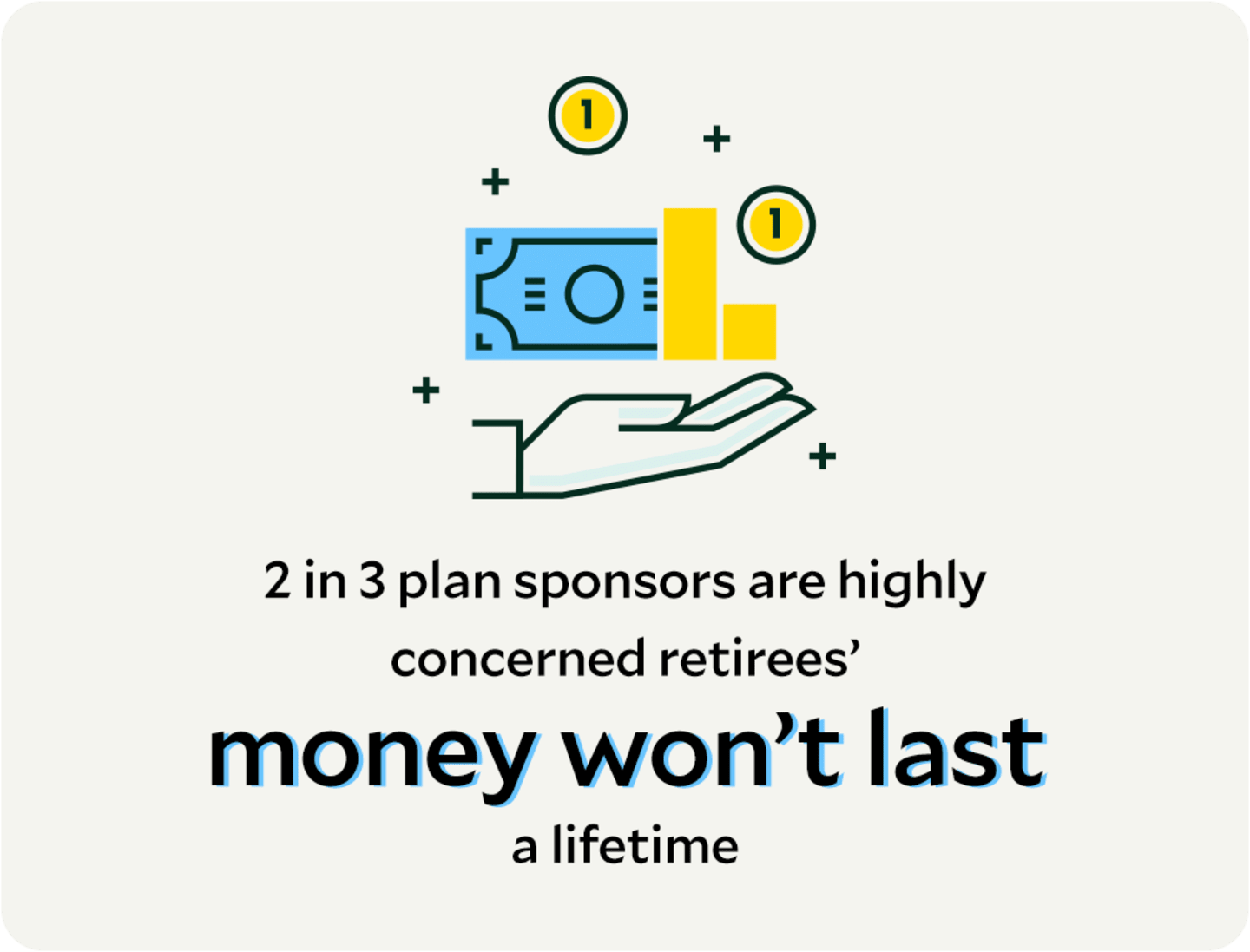

Although contribution rates have remained the same or higher in the past two years, plan sponsors worry their participants aren’t saving enough, and their savings won’t last in retirement.

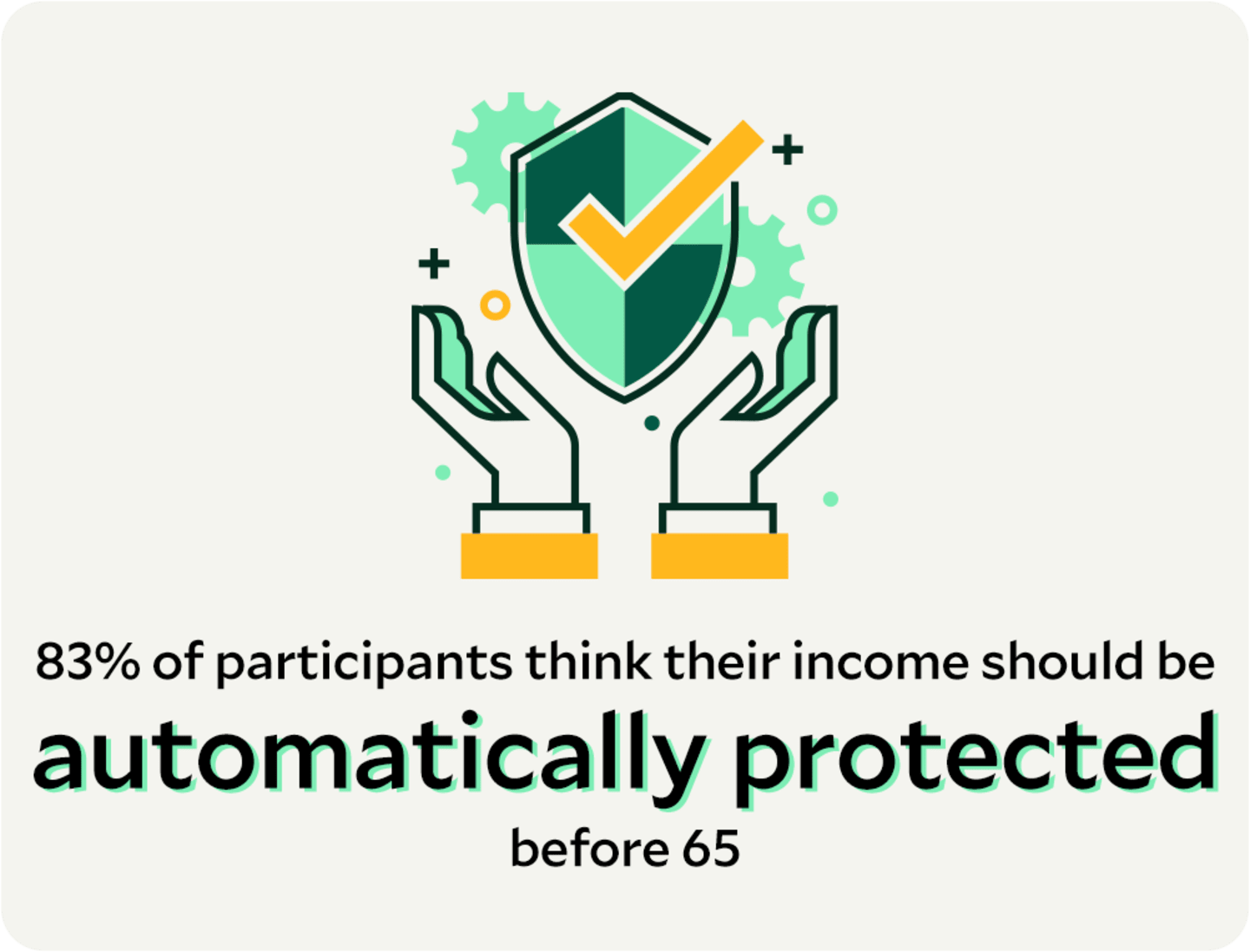

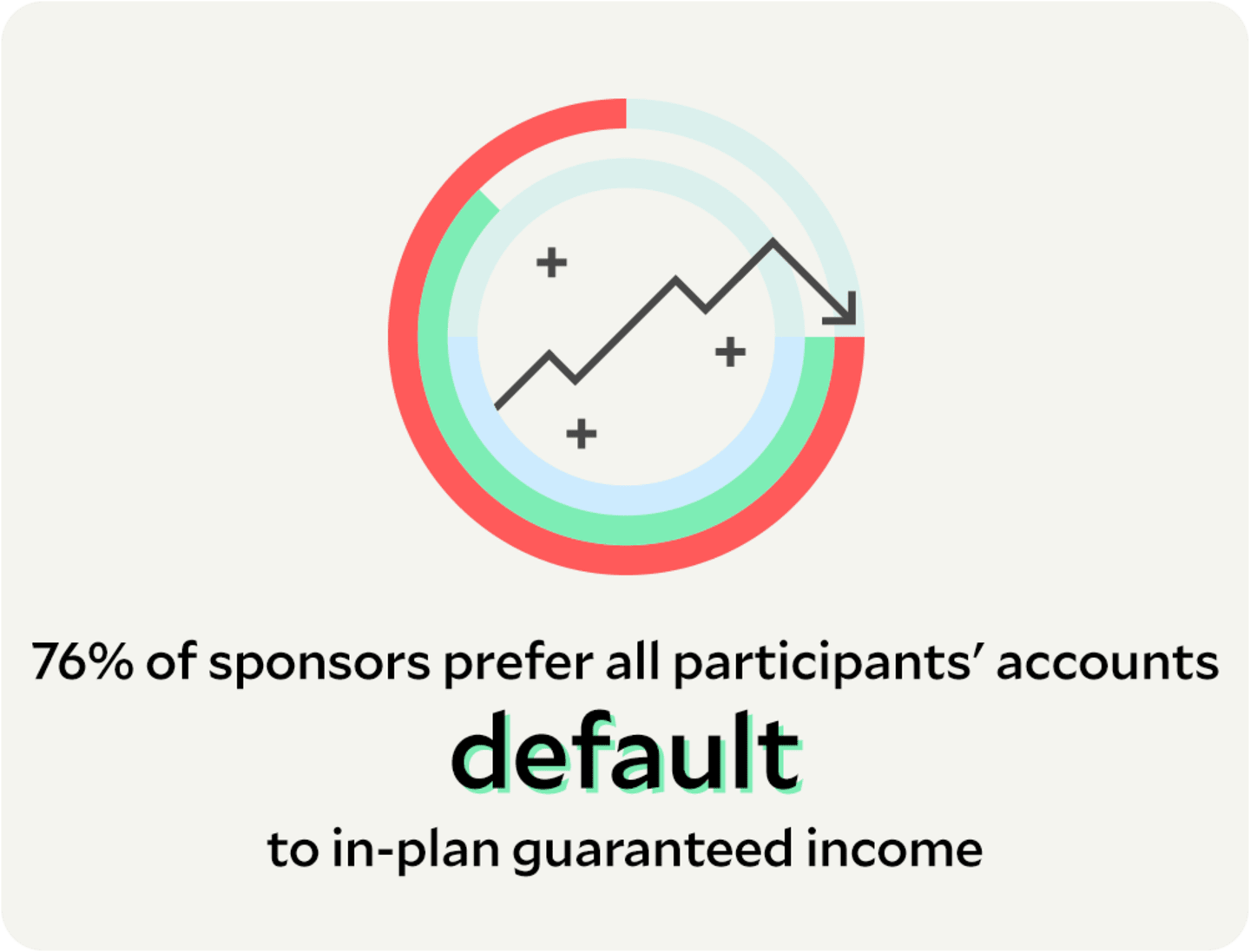

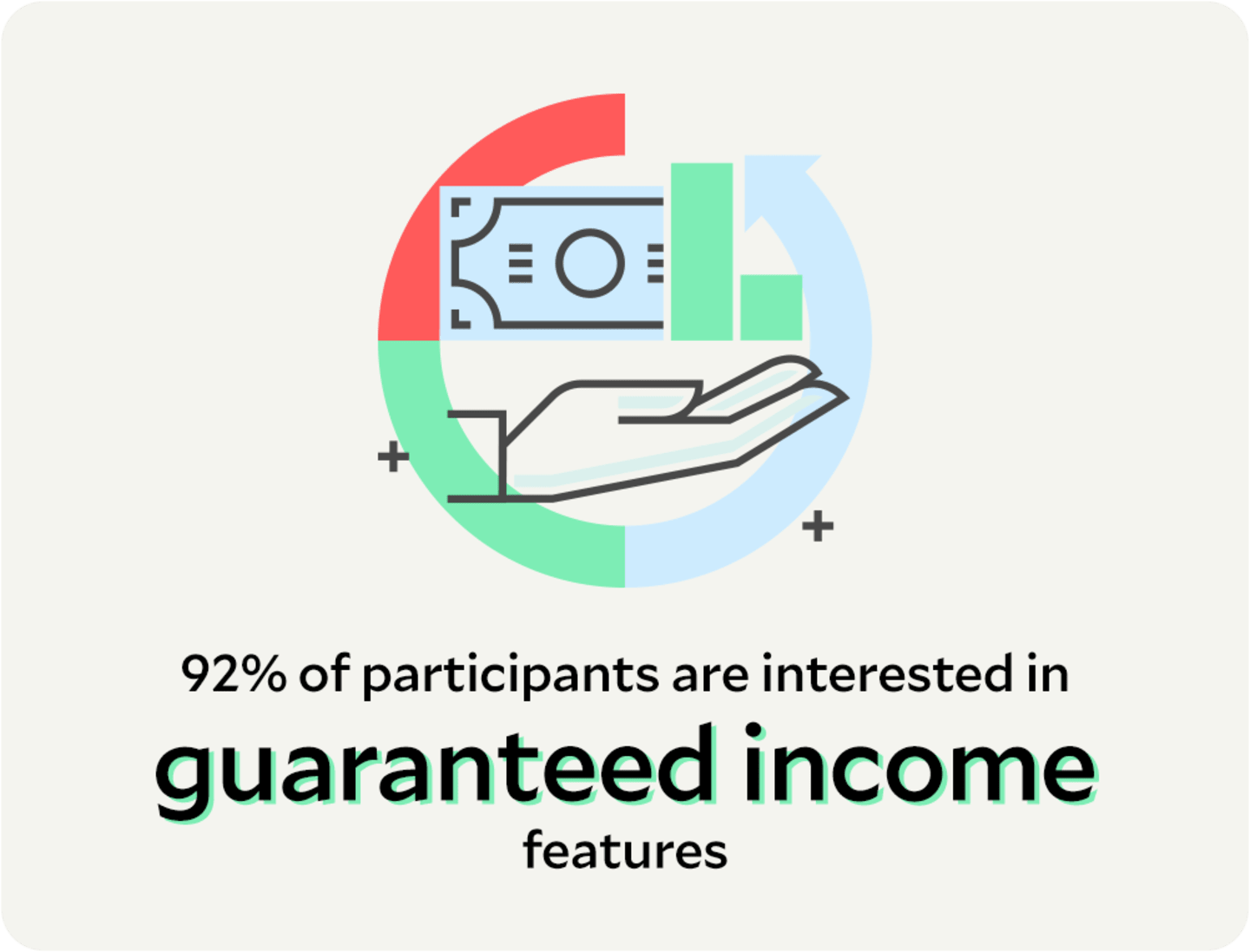

Protect Future Income

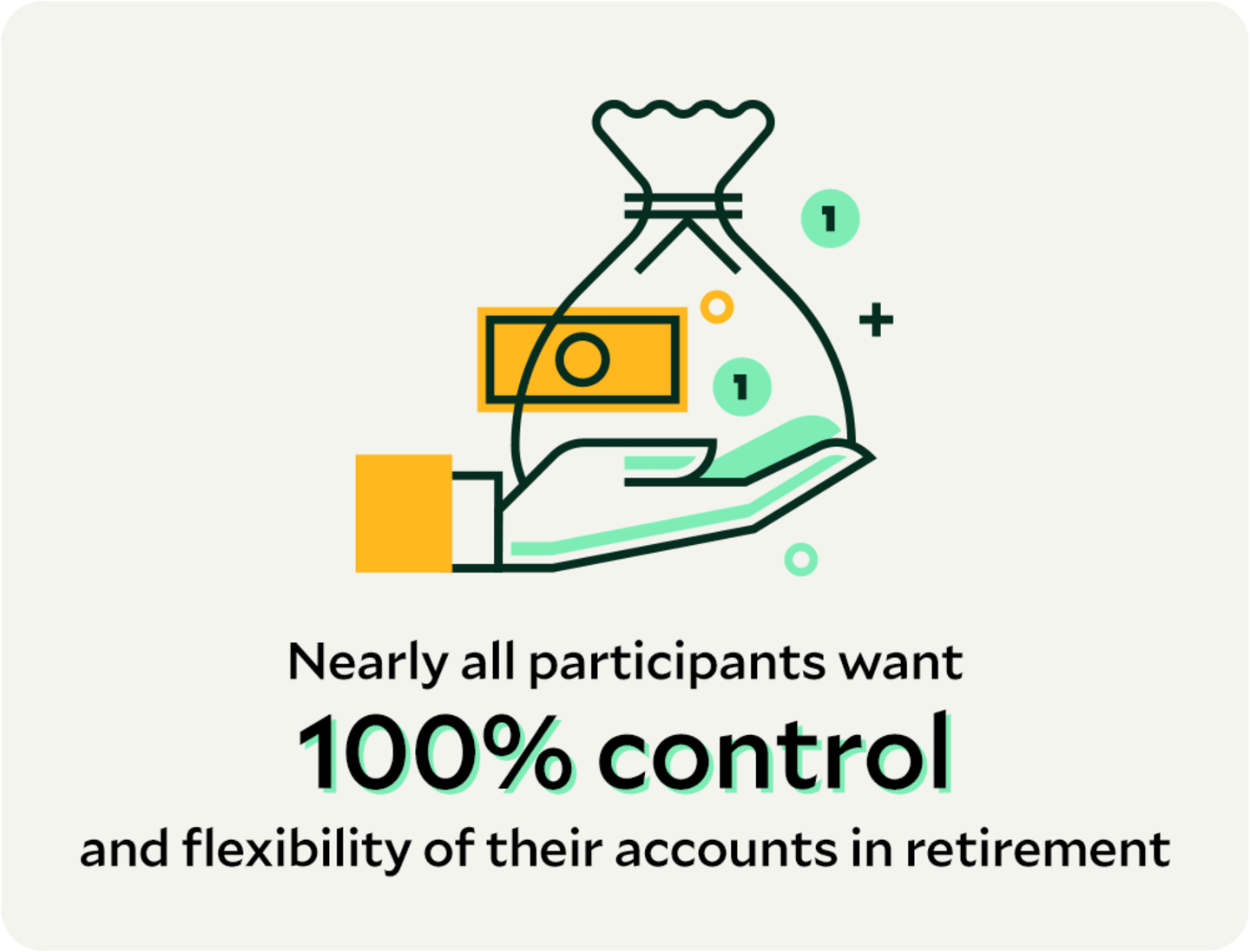

Most plan sponsors want to retain retiree assets in their plans, and some will actively seek it. Participants are interested in using some of their savings to get guaranteed income if they can control what happens. Plan sponsors agree they should offer it.

Target-Dates and Guaranteed Income Options Check Boxes

Sponsors believe TDFs and guaranteed in-plan income options seem to answer participants' asset protection needs and desire for control and flexibility. However, there are some misconceptions.

Have the Conversations Your Clients Need

Our survey found some clear misunderstandings about retirement income from both participants and plan sponsors, especially regarding asset protection, in-plan features and guaranteed income. The solution? Retirement advisors can change the conversation. And that may start with asking the right questions.

Savings Plan or Income Replacement Plan?

One way retirement advisors can begin to change the conversation with their clients about retirement income is to encourage plan sponsors to think about income replacement.

Get More of Our Tips About Changing the Retirement Conversation

A retirement plan without an income replacement plan is just a savings account.

Retirement Advisor Tools—Be the Resource Your Clients Need

Target-Date Blueprint

Narrow the TDF universe to focus on only funds with investment profiles that align with a plan’s demographics, risk profile and preferences.

Income Blueprint

Compare and contrast features and benefits of in-plan guaranteed income products.

Methodology: The participant survey was conducted between June 11, 2024, and June 27, 2024. Survey included 1,505 full-time workers between the ages of 25 and 65 saving through their employer’s retirement plan. The data were weighted to reflect key demographics (gender, income, and education) among all American private sector participants between 25 and 65.

The sponsor survey was conducted between June 10, 2024, and June 26, 2024. Survey included 500 plan sponsor representatives holding a job title of Director or higher, and having considerable influence when it comes to making decisions about their company’s retirement plan (either 401(k), 403(b), or 457 plans). The data were weighted to reflect the makeup of the total defined contribution population by plan asset size.

Percentages in the tables and charts may not total 100 due to rounding and/or missing categories.

Greenwald Research of Washington, D.C., completed data collection and analysis.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

You could lose money by investing in a mutual fund, even if through your employer's plan or an IRA. An investment in a mutual fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

The target date in a fund’s name is the approximate year when investors plan to retire or start withdrawing their money. The principal value of the investment is not guaranteed at any time, including at the target date.

Each target-date fund seeks the highest total return consistent with its proprietary asset mix. Over time, the asset mix and weightings are adjusted to be more conservative. In general, as the target year approaches, the portfolio's allocation becomes more conservative by decreasing the allocation to stocks and increasing the allocation to bonds.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.