Should I Cash Out My 401(k) for Money Now?

Can you cash out your 401(k) or retirement plan? Yes, but should you? Learn what happens when you withdraw early from your 401(k) and three reasons to reconsider.

Key Takeaways

Cashing out your 401(k) or other retirement account can be tempting, but there are financial implications now and at retirement.

If you're in a short-term cash crunch, you could consider other options rather than taking an early withdrawal from your retirement account.

When leaving a job, you have options for managing old retirement accounts without taking a 401(k) withdrawal or cashing them out.

Can I Take Money Out of a 401(k) or Retirement Plan Early?

Yes, many retirement plans allow you to withdraw your money early (before age 59 ½), but it may come at a cost. Still, people often dip into their accounts before retirement, despite the potential penalties.

One of the times it feels “easier” to cash out is when you change jobs. While most retirement plans allow you to take the money with you and not lose what you’ve saved, people may see this as an opportunity to cash out rather than continue investing for their future.

Why do people cash out their 401(k)s? Savers report they withdraw money from their retirement accounts for these reasons*:

Financial emergency

Paying off debt

Everyday expenses

Unplanned major expenses

Medical bills

Home improvements

Though these seem like valid reasons to take out a premature 401(k) distribution, it may not be the best course of action in the long run, and there may be better alternatives.

What Happens If I Cash Out? 3 Reasons to Think Twice

It's tempting to withdraw your retirement savings during a short-term cash crunch. But you worked hard to save that money. Consider three key reasons to avoid cashing out your 401(k) and keep your retirement savings invested: taxes, penalties and lost opportunities. These may help you ignore the urge to take a premature distribution from your retirement plan.

1. What are the Tax Consequences if I Cash Out My 401(k)?

There are tax consequences both now and when you file your taxes when you cash out early. That’s because your retirement account is designed to grow tax-deferred until you withdraw from it.

A 401(k) withdrawal could mean a higher tax bill. The withdrawal amount is added to your regular income, potentially putting you in a higher tax bracket.

Many 401(k) distributions paid directly to you are subject to a mandatory 20% federal income tax withholding, though actual taxes owed may be higher or lower depending on your tax bracket. It will be remitted to the IRS as a credit toward the income taxes due on your distribution.

Depending on which tax bracket you're in, you could owe from 10%–37% on your withdrawal when you file your income taxes for the calendar year of the distribution. You could also owe state and local taxes on that amount.

2. What are the Penalties of Cashing Out My 401(k) Early?

On top of your tax bill, the IRS imposes a 10% penalty on withdrawals if you are under age 59½.

Although the IRS makes some exceptions to the early distribution penalty, such as death or disability, the penalty is generally taken right off the top. Combined with your tax bill, you could forgo nearly half of your retirement savings.

Taxes + Penalty = Potentially Forfeiting Nearly Half of Your Money

Example of a $100,000 Cash Distribution

Source: American Century Investments. This hypothetical example assumes the following: the 20% mandatory federal income tax withholding, 6% in potential state and local income taxes and a standard 10% penalty for early withdrawal. This example is for illustrative purposes only. Please note that the 10% early withdrawal penalty does not apply to distributions made to an employee after separation from service during or after the year in which they turn 55. The 20% mandatory income tax withholding will be remitted to the IRS as a credit toward the income taxes due on your distribution. It may be higher or lower than your federal income tax bracket.

3. How Will Cashing Out My 401(k) Affect My Retirement?

Taxes and penalties from a 401(k) withdrawal could hurt your nest egg today. But the biggest hit may come from missed growth opportunities for your financial future. Taking out money today can lead to missing out on your money's growth potential over the years.

Below is an example that shows the money you could potentially forfeit if you withdraw just a portion of your retirement account today, versus keeping it invested for 25 years, or keeping it invested and adding to it. The hypothetical example below assumes a beginning balance of $10,000.

Scenario 1

You withdrawal the money now and are under the age of 59½.

Scenario 2

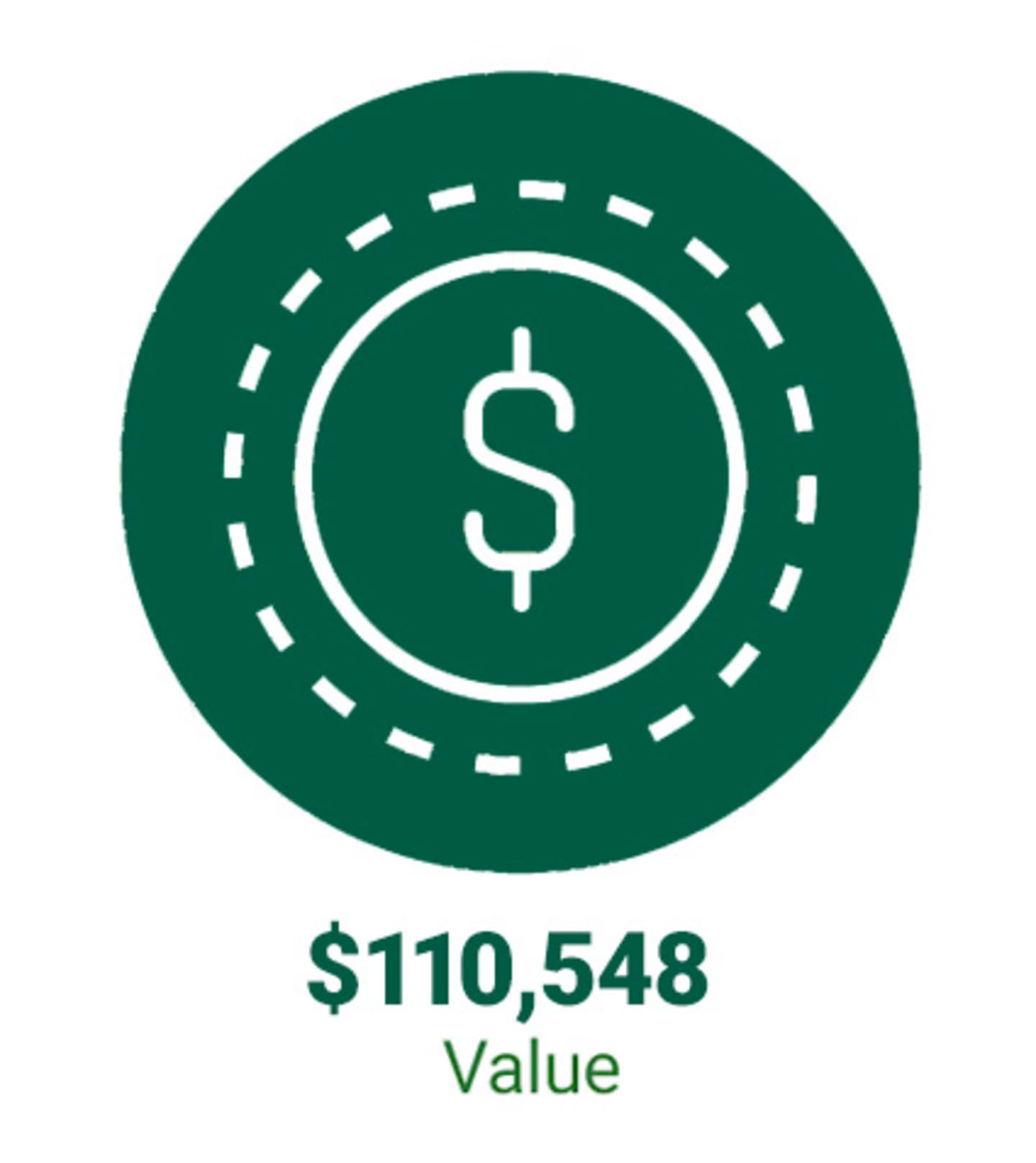

You keep the money invested for 25 years.

Scenario 3

You keep the money invested and you add $100 a month for 25 years.

Source: American Century Investments; Future Value Calculator, Dinkytown, Inc., January 2026. The withdrawal value assumes the following: the 20% mandatory federal income tax withholding, 6% in potential state and local income taxes and a standard 10% penalty for early withdrawal ($6,400) and 6% returns for 25 years if the money ($10,000) stays invested. This hypothetical situation contains assumptions that are intended for illustrative purposes only and are not representative of the performance of any security. There is no assurance that similar results can be achieved, and this information should not be relied on as a specific recommendation to buy or sell securities.

Financial Calculators from Dinkytown.net

Financial Calculators ©1998-2026 KJE Computer Solutions, LLC

Regret and Worry Are Real for Those Facing Retirement

An early 401(k) withdrawal may also result in sacrifices you may need to make in the future. Less money could mean working longer than you'd planned or rethinking how you want to live.

Building a strategy around your retirement savings can help you avoid the temptation to cash out a 401(k) early. A plan can help you realize how much you should save to cover a retirement that may last 20 years or more.

Not saving enough for retirement is often a significant level of worry for many people. Running the numbers to estimate how much you'll need can help ease the temptation to withdraw money from your 401(k) account early.

- 82% worry they haven't saved enough for retirement.

- 29% saved less than they should have by age 50.

Source: American Century Investments Participant Retirement Survey, July 2025.

What are Some Alternatives to Cashing Out My Retirement Savings?

There are several alternatives to cashing out your retirement savings early, including maintaining an emergency fund, taking a 401(k) loan or a low-interest personal loan if feasible. You could also look into some 401(k) withdrawal exceptions.

How Much Do I Need for an Emergency Fund?

Before you need money in a hurry, work to build an emergency fund of three to six months' worth of expenses.

If you aren’t sure how much you’ll need, add up your regular expenses to figure that out. To build your emergency fund, start by reviewing your budget to identify areas where you can cut back or eliminate expenses.

Is Taking a 401(k) Loan a Good Idea?

Borrowing from a 401(k) or other type of retirement plan has its drawbacks, but it may be a better alternative to cashing out because you will pay it back. Many 401(k) plans permit employees to borrow from their account balances and repay the loan over time. (Note that you can't borrow money from an IRA account.)

However, like cashing out, you'll have less money for retirement because you likely missed out on some growth while repaying the loan. In addition, if you terminate employment before you have paid back the outstanding loan, you may owe taxes and possibly penalties on the amount of the outstanding loan.

What Are Other Better Options to Cashing Out My 401(k)?

Other alternatives to cashing out your 401(k)—and if a 401(k) loan isn’t possible—include personal loans or seeing if you qualify for a 401(k) withdrawal exception.

For instance, if you qualify for a personal loan or a home equity loan, you can keep money in your retirement account and let it grow over time without taxes or penalties.

If you still need the cash and borrowing isn’t an option, you can also see if you qualify for any early 401(k) withdrawal exceptions that are not subject to the 10% penalty tax, if your plan allows for early withdrawals.

Expenses relating to the birth or adoption of a child, a first-time home purchase, disaster recovery, medical premiums (if you are unemployed), among others, could qualify you for penalty-free withdrawals.

Starting in 2024, the SECURE 2.0 Act lets you withdraw up to $1,000 annually from your 401(k) for emergency expenses for yourself or your family.

What Are Options for My 401(k) if I Leave a Job?

When you leave a job, you don't have to be tempted to cash out your 401(k). You have several options for managing your money, including leaving it where it is, rolling it into a new employer’s plan, or transferring it to an IRA. Let’s look at some details about each option.

Leave it in your old plan.

If you leave money in an old retirement plan, you cannot continue contributing to it. The account will be subject to rules set by your former employer, but this is likely preferable to a 401(k) cash-out. When you leave the money where it is, you won’t be subject to taxes and early withdrawal penalties, if under age 59½, until you take a distribution.

Roll it into an employer's plan.

Money from an old account would work alongside the new money you and your employer contribute. You may prefer to manage a single retirement account over multiple scattered accounts.

Transfer it to an IRA.

Perhaps your new employer's retirement account charges high fees, or it's a small company that doesn't offer retirement accounts. You might decide to transfer your old 401(k) into an IRA as a direct rollover. That way, you can continue contributing and consolidate it with other accounts.

None of these three options involves withdrawing money from your retirement account. Your access to these may vary depending on the details of the old and new retirement plans. If nothing else, you can transfer the old account into an IRA to avoid taxes and early withdrawal penalties.

Authors

Financial Consultant

Keep Your Eyes on the Future

Need help avoiding the cash-out temptation? Let us help answer questions or run your numbers.

Retirement Throughout the Ages: The American Middle Class-25th Annual Transamerica Retirement Survey, Transamerica Center for Retirement Studies, October 2025.

This information is for educational purposes only and is not intended as a personalized recommendation or fiduciary advice. There are different options available for your retirement plan investments. You should consider all options before making a decision. Our representatives can help you evaluate all of your distribution options.

IRS Circular 230 Disclosure: American Century Companies, Inc. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated with American Century Companies, Inc. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

This information is for educational purposes only and is not intended as tax advice. Please consult your tax advisor for more detailed information or for advice regarding your individual situation.

You could lose money by investing in a mutual fund, even if through your employer's plan or an IRA. An investment in a mutual fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

IRA investment earnings are not taxed. Depending on the type of IRA and certain other factors, these earnings, as well as the original contributions, may be taxed at your ordinary income tax rate upon withdrawal. A 10% penalty may be imposed for early withdrawal before age 59½.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.