Understanding ETF Tax Efficiency

Thanks to their unique structure and trading process, exchange-traded funds (ETFs) can help mitigate taxable events and help investors keep more of their money working for them.

Key Takeaways

ETFs’ tax efficiency centers on how they are bought and sold, as well as how shares are created and redeemed.

ETFs distribute less capital gains while held, which means more assets remain invested to potentially compound at a higher rate.

The proof is in the numbers. Data shows how investors may pay lower tax bills with ETFs than with other investment vehicles.

Taxes can take a larger bite out of an investment’s returns than annual management fees. ETFs have built-in tax advantages that can keep more money invested and working for investors rather than Uncle Sam.

Mutual funds and ETFs are required to distribute net investment income and realized capital gains at least annually to shareholders. If distributions occur in nonretirement accounts, investors may be liable for income and capital gains taxes, even if they did not sell any shares or if they reinvested the proceeds.

The amount of those distributions can vary widely between strategies and even among funds with similar objectives. Generally, the more distributions a mutual fund or ETF makes, the more money an investor forfeits to taxes.

This guide explains the mechanics behind ETF tax efficiency and concludes with a case study showing how those characteristics have historically helped limit taxable distributions.

Why Are ETFs More Tax Efficient Than Traditional Mutual Funds?

In simple terms, ETFs are more tax efficient than traditional mutual funds because they are bought and sold differently.

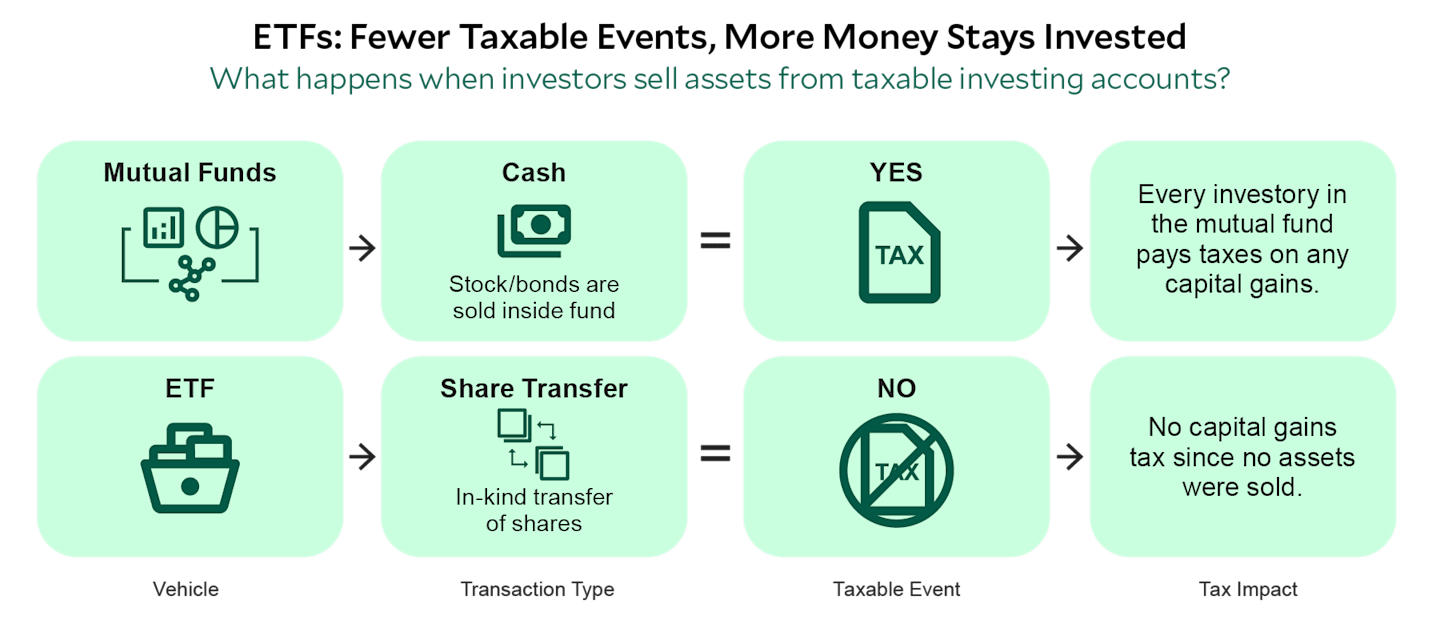

Selling mutual funds requires selling securities to generate cash. When an investor (or advisor on the investor’s behalf) wants to sell mutual fund shares, the fund issuer needs to sell some of the fund’s underlying holdings and reallocate the assets in the portfolio to generate the cash to redeem the shares.

Selling appreciated securities can create capital gains for the remaining shareholders invested in the fund, even if those shareholders did not sell any shares.ETFs generally limit the need to sell securities by trading on an exchange or in kind. Investors who want to buy or sell shares of an ETF essentially transfer shares with other investors in the market. They do not interact directly with the fund issuer.

When the number of available ETF shares equals demand, an investor who wants to sell the ETF simply trades shares with someone who wants to buy. (More on what happens when demand outstrips supply in a moment.) The stocks and bonds within the ETF are unaffected.

Because there is no turnover in the underlying holdings themselves, there is no taxable income event for other shareholders.

How Do APs and the Creation and Redemption Process Drive ETF Tax Efficiency?

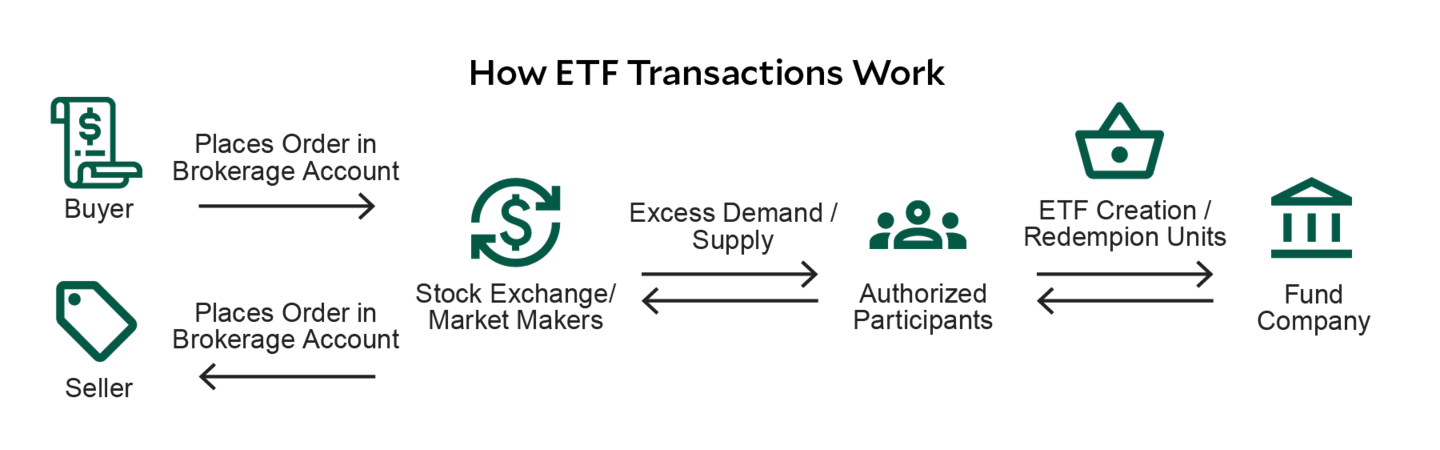

When there’s more demand to buy or sell an ETF than existing shares can handle, large institutional investors called authorized participants (APs) step in. They work directly with the ETF issuer to create or redeem shares.

How ETFs Create Shares

To create new ETF shares, the AP acquires the exact mix of stocks or bonds the ETF holds (called the creation basket) and delivers them to the ETF issuer. In return, the ETF issuer gives the AP an equal value of ETF shares.

How ETFs Redeem Shares

When shares are redeemed, the process works in reverse: Instead of selling investments for cash, the ETF provider gives the basket of the actual securities it holds to the AP. This avoids selling inside the fund, which keeps trading costs low and prevents the triggering of taxable events.

How the Creation and Redemption Process Matters for Taxes

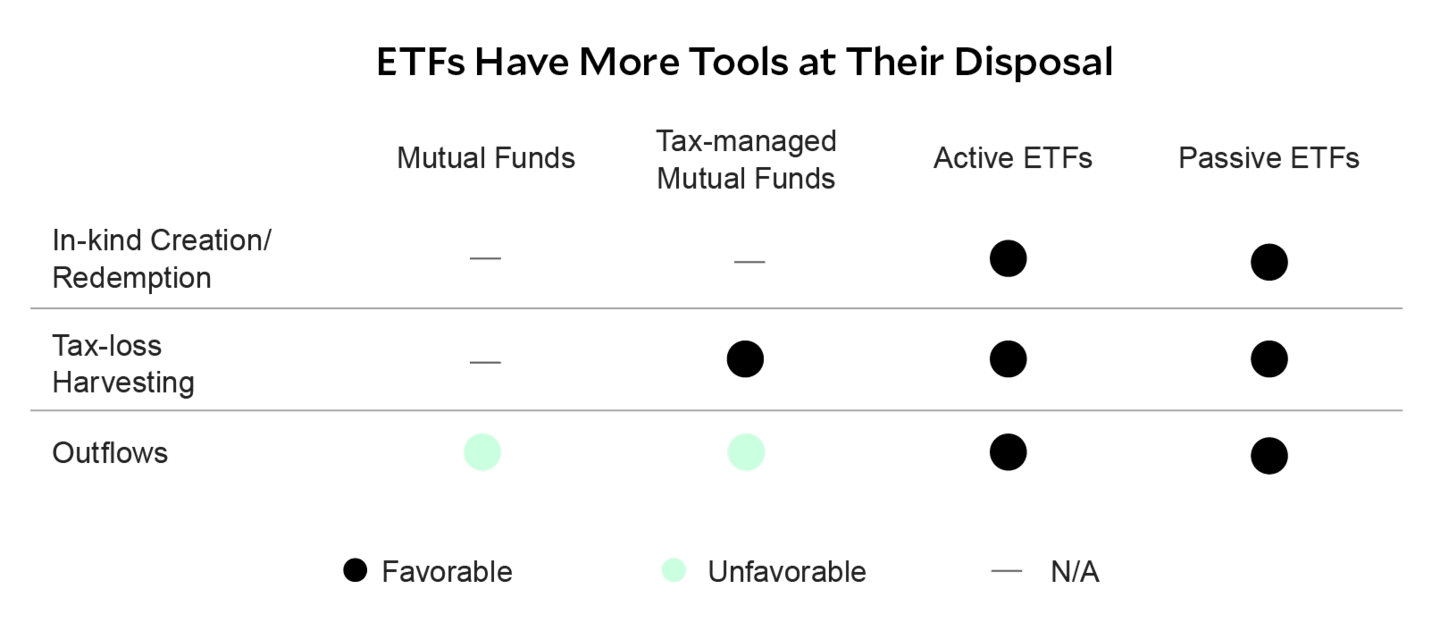

ETF transactions usually happen “in kind,” meaning securities are swapped. No cash changes hands, so no taxable sale occurs. Additionally, ETF portfolio managers could give the AP the securities with the lowest cost basis (the biggest unrealized gains). In other words, the securities with built-in gains move to the AP, helping keep existing shareholders from having extra tax bills.

The majority of ETF purchases and sales occur among buyers and sellers in the secondary market.

If demand outstrips available inventory on the exchange, APs can create more ETF shares.

The creation/redemption process typically takes place by delivering or redeeming securities in kind.

Portfolio managers can elect to deliver low-cost basis securities in a redemption, reducing capital gains exposure.

How Do ETFs Give You Control Over When Capital Gains Taxes Are Paid?

ETFs can be a smart choice for investors who want to manage their annual tax bills. However, investors will still owe capital gains taxes if they sell their ETF or mutual fund shares for more than they paid in their taxable accounts.

Mutual funds often realize capital gains each year as managers buy and sell investments to meet investor redemptions and reallocate the portfolio. In contrast, ETFs are designed to minimize these taxable events, with most capital gains recognized when investors sell their ETF shares in their taxable accounts. This means more money stays invested and has the potential to grow over time.

Tips for Managing Capital Gains Taxes

1. Mark the Calendar for Year-End Distributions

Both mutual funds and ETFs must distribute capital gains and income to investors at least once a year. Fund companies usually start announcing estimated capital gains distributions in September, with payments typically made in December.

Pay attention to these estimates. Sometimes, the distributions can be large compared to the fund’s value. If a fund is projecting significant capital gains, an investor might consider selling before the record date to avoid the distribution. Keep in mind, though, that selling shares in a taxable account is itself a taxable event.

2. Keep an Eye on Capital Gains All Year

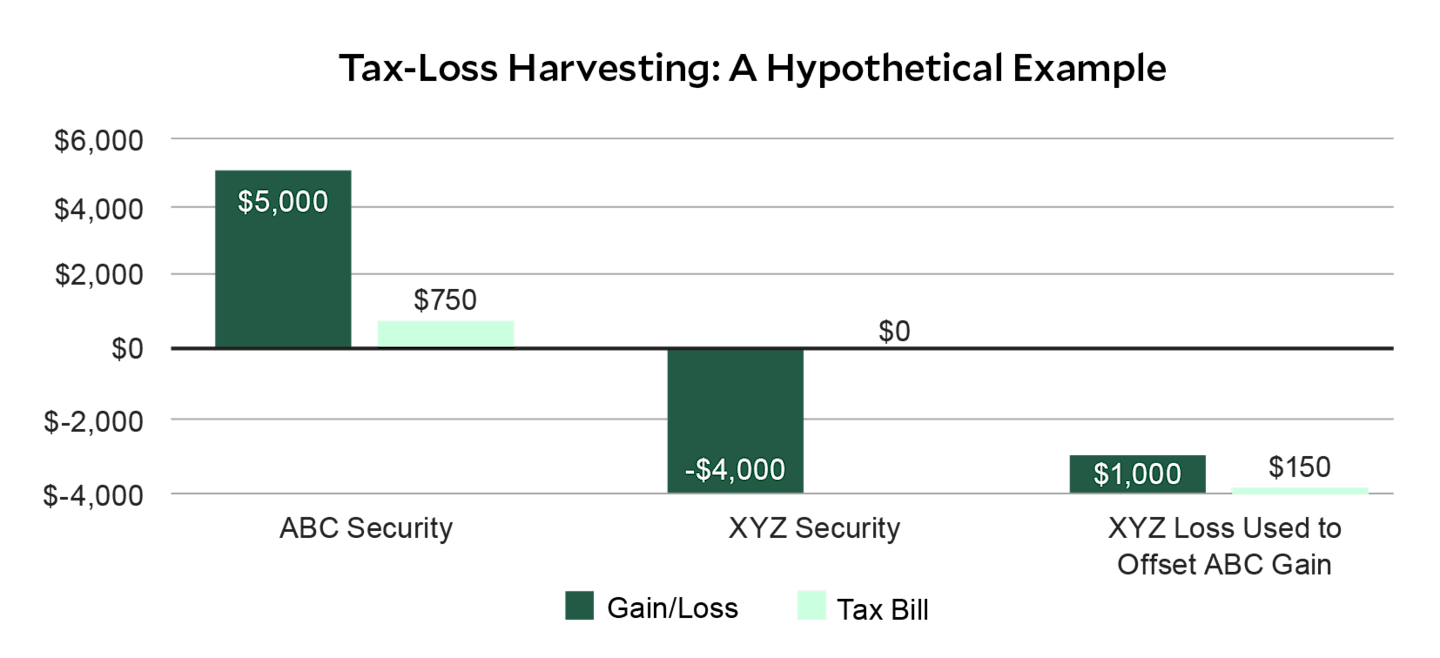

Many advisors and investors look for ways to reduce capital gains taxes at year-end, but it’s wise to think about taxes throughout the year. Opportunities to offset gains with losses—known as tax-loss harvesting—can arise at any time and help lower an overall tax bill.

Tax-loss harvesting allows investors to offset gains realized in one investment with losses incurred in another.* The following hypothetical example illustrates how this technique can help reduce an investor’s tax liability.

The hypothetical long-term loss from the sale of XYZ partially offsets the long-term gain from the sale of ABC.

This example assumes a capital gains tax rate of 15%. This rate varies by filing status and income.

The offsetting loss results in a tax savings of $600.

It’s important to know the tax-loss harvesting rules, risks and common mistakes, including the IRS’ wash-sale rule. A tax advisor can help investors with their specific situations.

3. Consider Which Account Type to Use for Each Investment

Asset location can help lower taxes and improve after-tax returns. For instance, using tax-efficient investments like ETFs in taxable accounts can help not only manage the ongoing capital gains and tax liabilities but also enhance the returns investors keep.

CASE STUDY: ETF vs. Mutual Fund Tax Efficiency | Why ETFs Usually Win the After-Tax Battle

Analysts at American Century Investments compared the tax losses incurred by investors in different types of equity funds. The results showed that ETFs—whether actively or passively managed—were the most tax-efficient options.

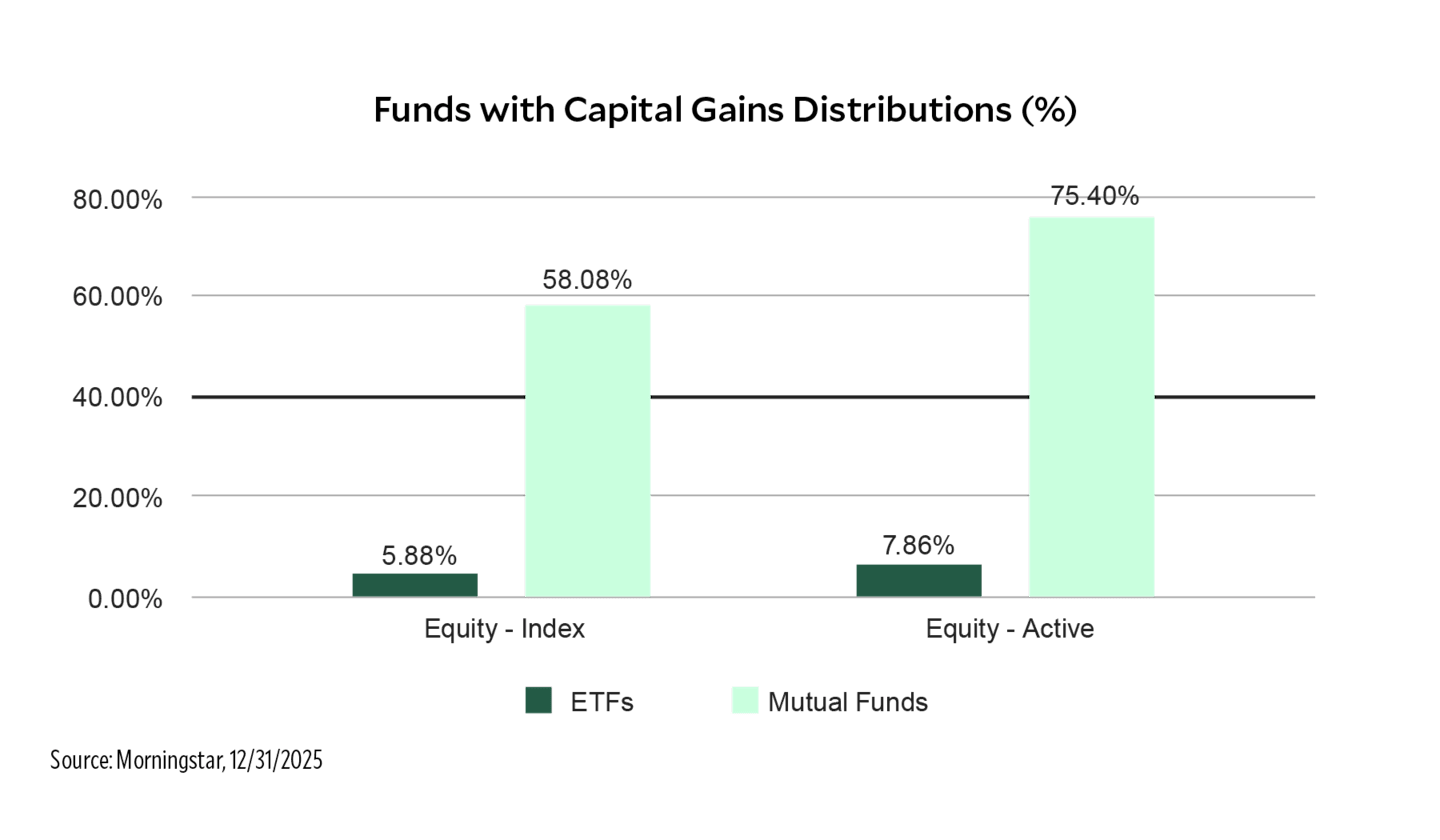

How Are the Distribution Patterns of ETFs and Mutual Funds Different?

Across the board, the number of ETFs that distributed capital gains was considerably less than the number of mutual funds.

Analysts looked at how often different types of funds distributed capital gains, comparing both index and actively managed equity funds. This chart shows the percentage of funds in each category that made these distributions from each fund’s inception through the end of 2025.

The percentage of equity ETFs that paid out capital gains was considerably less than mutual funds. For example, almost 8% of active equity ETFs paid out capital gains, while nearly 76% of active equity mutual funds did.

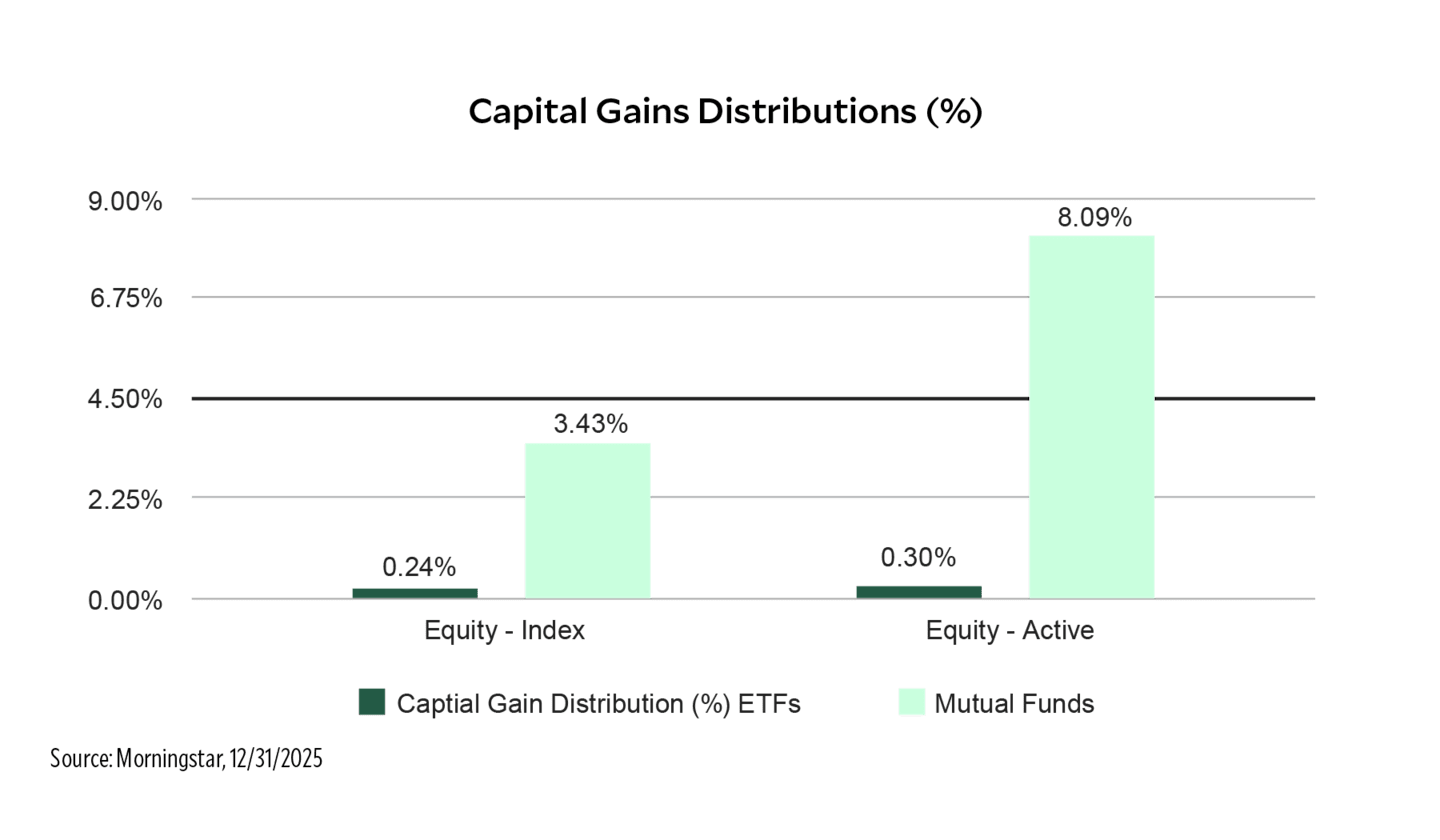

Analysts also examined the average capital gains distribution as a percent of the fund’s net asset value. Data in the chart shows the amount of distributions in the equity category from the inception of each fund to December 31, 2025.

The amount that equity ETFs paid out in capital gains was substantially lower than that of mutual funds.

Why ETFs Lead the Way in Tax-Efficient Investing

ETFs stand out for their ability to help investors manage taxes. Not only do they offer lower costs and straightforward trading, but their structure also helps mitigate taxable events—so more money stays invested and working for them.

While no one can avoid reporting and potentially paying taxes on profits from selling any investment, ETFs make it easier to control when and how much investors pay in capital gains taxes. By using smart strategies and staying invested, investors have the opportunity to reduce their tax bills.

ETFs are a powerful choice for investors who seek to keep more of their money working for them and manage taxes efficiently. Because everyone’s situation is different, investors should consult a tax advisor who can help determine what works best for them.

Do ETFs Have a Place in Your Portfolio?

ETFs can be combined with other investments, including mutual funds and individual securities, to build diversified and flexible portfolios.

Long- and short-term capital gains are taxed at different rates. Long-term gains may only be offset by longer-term losses. Likewise, short-term gains may only be offset by short-term losses.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

IRS Circular 230 Disclosure: American Century Companies, Inc. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated with American Century Companies, Inc. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

This information is for educational purposes only and is not intended as tax advice. Please consult your tax advisor for more detailed information or for advice regarding your individual situation.

Diversification does not assure a profit nor does it protect against loss of principal.

©2026 Morningstar, Inc. All Rights Reserved. Certain information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.