Up in the Air: How Higher Aerospace Demand Could Benefit Small-Caps

Industry giants typically rely on the expertise of smaller suppliers.

Key Takeaways

A backlog of 17,000 planes gives suppliers a potentially long runway — years of steady demand, better pricing and improved visibility for smaller firms.

Small-cap aerospace firms play critical roles in supply chains and can’t be easily replaced.

Airbus and Boeing, the world’s largest aircraft manufacturers, are boosting production to clear record backlogs.

Next time your flight is delayed, keep in mind you’re not the only one waiting for a plane.

The commercial aerospace industry is staring down an estimated backlog of 17,000 aircraft orders.1 Even if manufacturers didn’t take any new orders, it would still take them about 12 years to catch up under current production levels.2

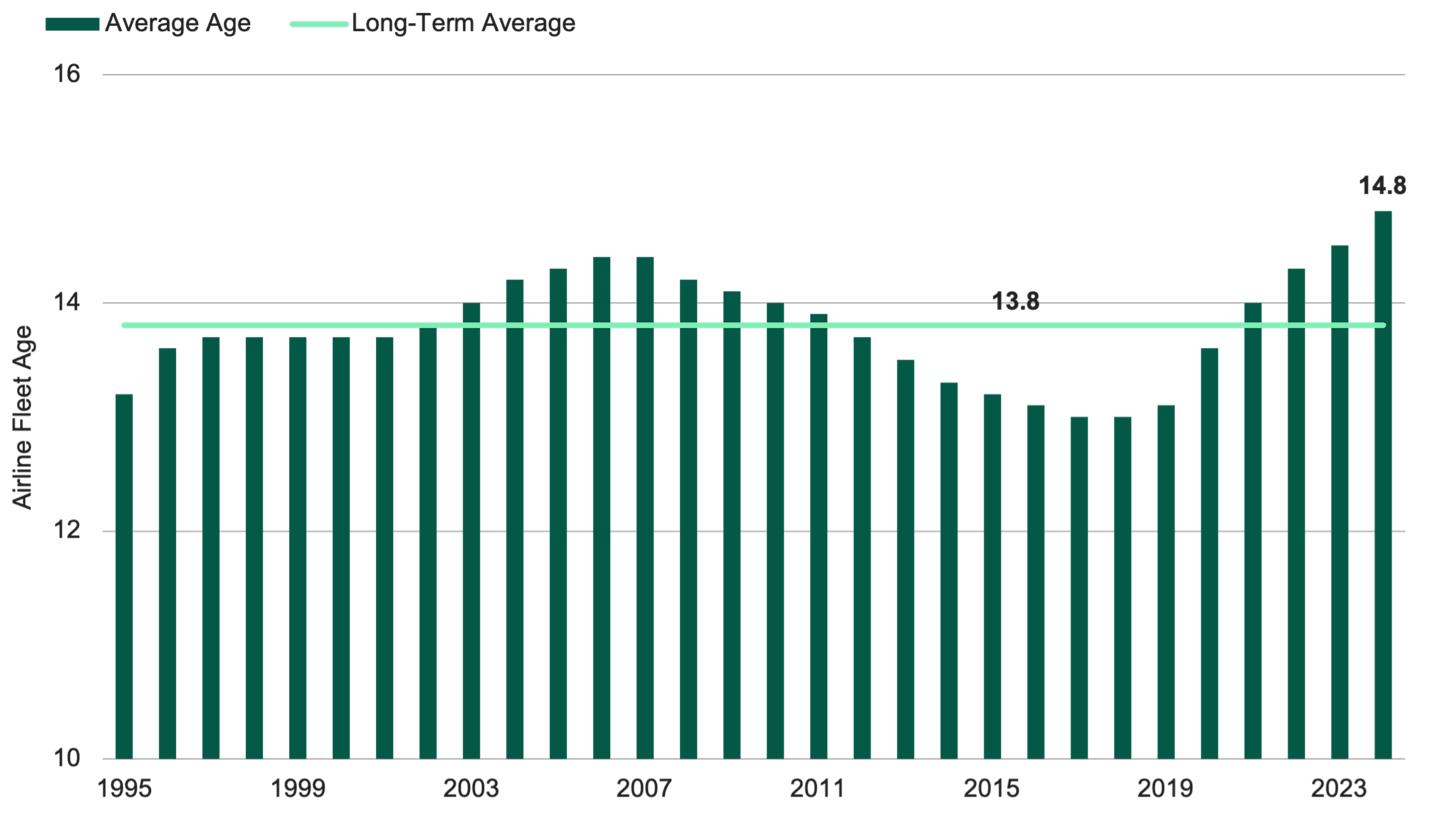

Meanwhile, airlines are keeping older aircraft in service longer than usual because they don’t have new planes ready, as shown in Figure 1. The airlines are also eager to upgrade to next-generation parts and components to boost fuel efficiency.

Figure 1 | Average Age of Global Commercial Airline Fleets Hits New High

Data from 1/1/1995 – 12/31/2024. Source: IATA Sustainability and Economics, Cirium Fleets Analyzer, U.S. Global Investors.

Original equipment manufacturers (OEMs) such as Airbus and Boeing are ramping up production to meet increased demand.3 After years of supply chain headaches, deliveries of new aircraft were expected to rise by 25% last year.4

To handle this higher demand, the OEMs need help from an army of suppliers — many of which are smaller firms with specialized expertise. These companies produce critical parts and components that are hard to find elsewhere.

Even if geopolitics led some airlines to delay orders for new aircraft, we believe the impact would be limited because other airlines would still move forward.

In our view, an improving demand outlook and stronger pricing might help accelerate revenue and profit growth for small-cap aerospace companies over the next several years.

Why the Aerospace Industry Needs Small-Cap Firms

Aerospace manufacturing requires precise accuracy because lives can literally depend on these products. We believe that small-cap companies that meet these high standards are likely well-positioned to benefit from increased demand.

Take Carpenter Technology as an example. This company produces specialty alloys engineered to withstand extreme temperatures and pressures without breaking. Its products are used in various end markets, including aerospace, defense and medical transportation.

Higher demand from commercial aerospace benefits Carpenter in two main ways: First, more aircraft are being manufactured; and second, newer planes are increasingly utilizing alloys produced by Carpenter. The company is among only three firms globally competing in this specialized market niche.5

Hexcel is in a similar position. It’s the world’s largest producer of aerospace-grade carbon fiber composites, which are lighter and tougher than traditional materials.6

The next generation of aircraft uses more of the composite materials that Hexcel makes.7 These materials often provide a higher strength-to-weight ratio, better corrosion resistance and greater design flexibility.

Would-be competitors can’t enter this market quickly or easily. Hexcel has made significant investments in production facilities worldwide. It has also developed valuable intellectual property and built a highly trained workforce.

Hexcel CEO Thomas Gentile describes the barriers to entry in the niche industry as “significant.”8

And that doesn’t account for the high regulatory hurdles. Gaining approval for aerospace materials from regulators like the Federal Aviation Administration is a rigorous process that can take years. This adds another competitive layer of protection for established companies like Carpenter and Hexcel.

How Is Global Defense Spending Influencing Aerospace Suppliers?

The aerospace industry could also experience increased demand from the defense and space sectors.

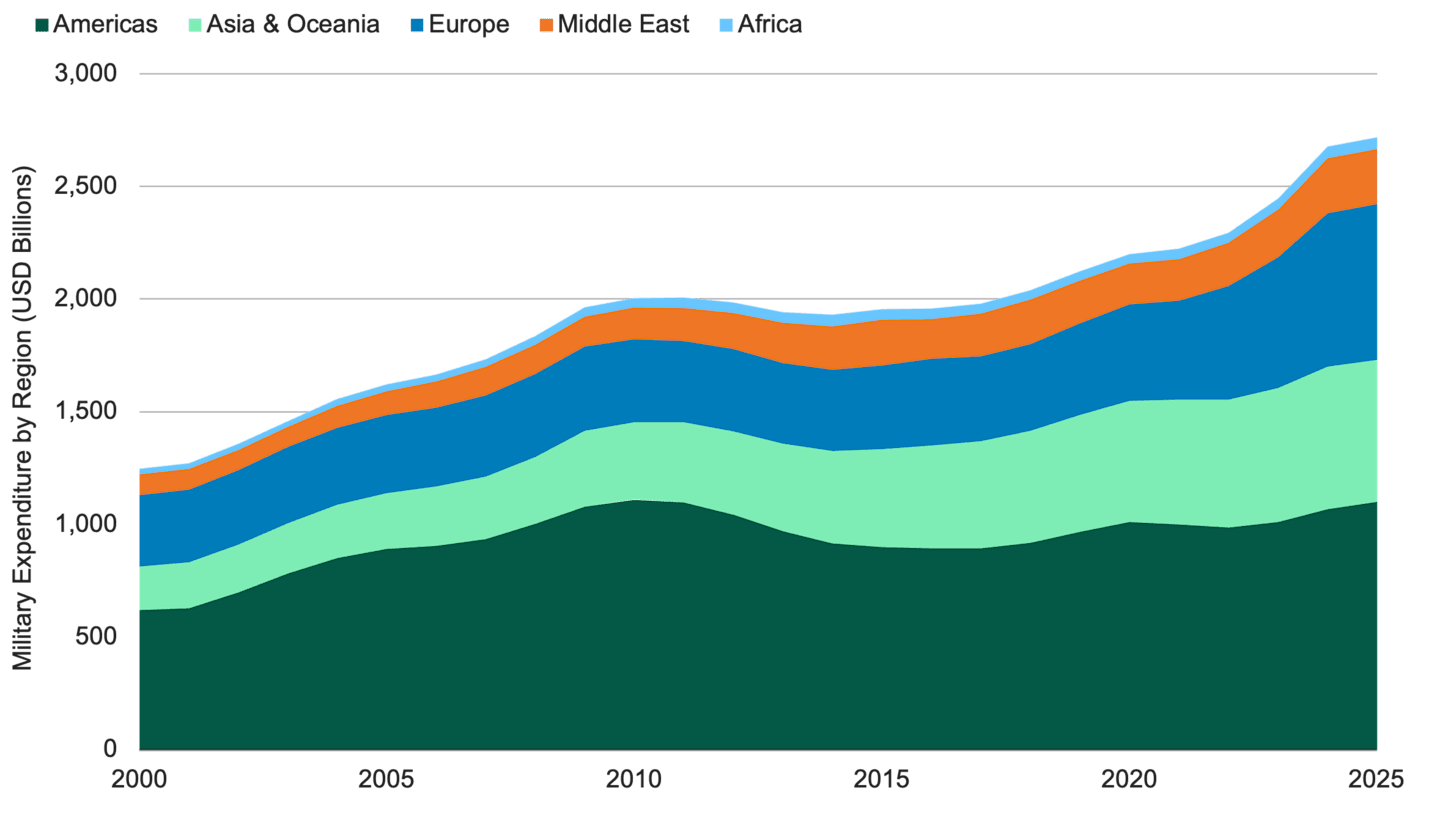

Military spending is rising globally, as shown in Figure 2. For example, after decades of stagnant defense budgets, Europe aims to boost spending by 300 billion euros through 2030.9

Figure 2 | Defense Budgets Keep Climbing Around the World

Data from 1/1/2000 – 6/30/2025. Source: SIPRI Military Expenditure Database 2025, HSBC.

Companies like Hexcel are seeing improving defense-related orders. The company said its defense sales have improved due to increased demand for military rotorcraft.10 Its composites are used in rotor blades and other parts.11

MDA Space has seen increased interest in its satellite technologies, which could be used in defense communication networks.12

In 2025, the company secured contracts to build uncrewed aircraft for the Royal Canadian Navy, which intends to use them to monitor maritime threats.

“We’re in the early days of a new, and what is expected to be a prolonged, investment cycle.”

MDA Space CEO Mike Greenley

How Could Satellite Growth Increase Demand Across Space Suppliers?

The space industry could grow by 9% annually through 2035, reaching a $1.8 trillion market. That’s based on a forecast from the World Economic Forum and McKinsey & Co. To put that into perspective: Nearly 15,000 satellites currently orbit Earth, and Goldman Sachs Research estimates another 70,000 could be launched into low orbit in the next five years.13

Space exploration represents another potential avenue for small-caps in the aerospace industry. MDA Space is developing a robotic arm system for space missions.14 The firm has also joined an effort to develop a lunar utility vehicle.15

How Aerospace OEMs Support Their Small-Cap Suppliers

While smaller aerospace firms possess several advantages, they also face challenges, including skilled labor shortages and rising costs.16

To get ahead of potential problems, larger aerospace OEMs are taking steps to fortify their supply chains. They’re adding new suppliers in other regions, investing in AI-powered forecasting and relocating production closer to customers.

Several OEMs are also entering long-term agreements with their suppliers, paying them more or both. This has boosted results for some small-cap suppliers and given them confidence to invest in expanding their operations.

Carpenter, for example, plans to increase production capacity by 7% above 2019 levels.17 However, Carpenter’s efforts, along with those of other companies, may not solve the aerospace supply issue overnight.

“While this [capacity expansion] is meaningful to the financials of Carpenter Technology, it is not a meaningful increase for the industry.”

Carpenter CEO Tony Thene

Why Aerospace Demand Could Continue

A shortage of new aircraft presents a real and pressing problem for the global economy.

The International Air Transport Association, a global trade group for airlines, predicts that passenger demand will more than double by 2050.18 But the group also notes production bottlenecks could impact growth.19

Aerospace companies are working to increase capacity, but such capital investments tend to move slowly. Combine that with steady growth in new plane orders, and we believe revenue growth could continue well into the 2030s, depending on production rates and other factors.

Authors

Senior Investment Analyst

Senior Client Portfolio Manager

Explore Our Small-Cap Capabilities

International Air Transport Association, “Global Outlook: Trade, AI and the Energy Transition,” December 2025.

International Air Transport Association, “Aerospace Supply Chain Bottlenecks Continue to Constrain Airlines,” Press Release, December 9, 2025.

Airbus, “Ramping Up A320 Family Production,” October 30, 2025; Boeing, “Boeing Reports Third Quarter Results,” Press Release, October 29, 2025.

Accenture, “Resilience in Flight: Securing Future Growth amid Volatility,” Insight Report, October 13, 2025.

FactSet, Carpenter Technology Corp. Q2 2026 Earnings Call Transcript, January 29, 2026.

FactSet, Hexcel Corp. Q3 2025 Earnings Call Transcript, October 23, 2025.

Rohan Patole, Nitin Ambhore, and Devendra Agrawal, “Carbon Composites in Aerospace Application - A Comprehensive Review,” Materials International, October 12, 2023.

FactSet, Hexcel Corp. Q3 2025 Earnings Call Transcript, October 23, 2025.

David Chinn, Hugues Lavandier, Jakob Stöber, Marcel Schlepper and Tobias Otto, “European Defense by the Numbers,” McKinsey & Co., February 12, 2026.

FactSet, Hexcel Corp. Q4 2025 Earnings Call Transcript, January 29, 2026.

Hexcel, Defense & Space, as of March 6, 2026.

FactSet, MDA Ltd. Q3 2025 Earnings Call Transcript, November 14, 2025.

Goldman Sachs, “The Global Satellite Market Is Forecast to Become Seven Tmes Bigger,” March 5, 2025.

MDA Space, “NASA’s Gateway Mission: Canadarm 3,” as of February 18, 2026.

FactSet, MDA Ltd. Q3 2025 Earnings Call Transcript, November 14, 2025.

Brooke Weddle, Kevin Sachs, Elizabeth Mygatt and Yasi Akbari, “Accelerating Progress: Maximizing the Return on Talent in A&D – 2025 AIA Aerospace and Defense Workforce Study,” Aerospace Industries Association, 2025.

FactSet, Carpenter Technology Corp. Q2 2026 Earnings Call Transcript, January 29, 2026.

International Air Transport Association, “Air Travel Demand Will More Than Double by 2050,” Press Release, March 17, 2026.

International Air Transport Association, “Global Outlook: Trade, AI and the Energy Transition,” December 2025.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.

No offer of any security is made hereby. This material is provided for informational purposes only and does not constitute a recommendation of any investment strategy or product described herein. This material is directed to professional/institutional clients only and should not be relied upon by retail investors or the public. The content of this document has not been reviewed by any regulatory authority.