Health Care in Retirement—What Will It Cost?

What will health care cost you in retirement? Chances are, more than you expect. Learn how to prepare for these expenses, including Medicare's role and factors that affect your costs.

Key Takeaways

Health care may be one of the most expensive and misunderstood expenses for retirees and for those planning for retirement.

Few people plan for what health care may cost them in their retirement budget.

Find out how planning for health care costs may help you have a healthier retirement.

Taking care of your health isn't just about living a healthy lifestyle. It's also important to plan for potential medical expenses after you stop working. Understanding the costs of health care in retirement—and how to prepare—can help you create a retirement budget with a better chance of holding up.

Health Care in Retirement—Misunderstood and Underestimated

Health care could be one of the highest costs you'll face in retirement—and it’s the retirement expense that people don’t often plan for or give enough consideration ahead of time.

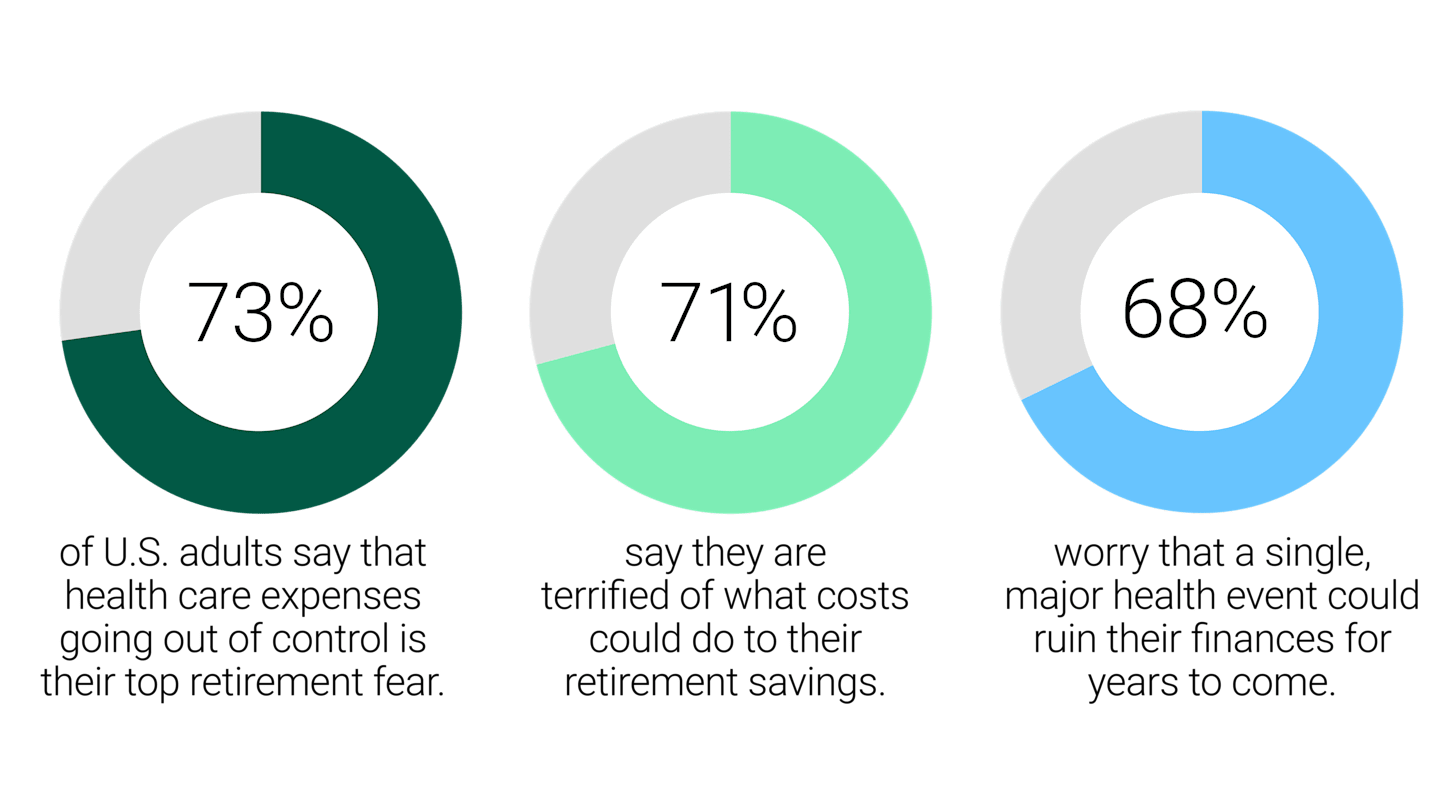

When they do, it also may be one of the most underestimated—even for people who have spent years saving. Two in five retirees note that health care expenses have been higher than they expected.1 Rising costs and people living longer have contributed to concerns people have about health care, as evidenced in a recent survey.

Source: Nationwide Retirement Institute® 2025 Health Care Survey, November 2025.

Couple these concerns with more than half of adults saying that medical expenses have drastically reduced how much they have saved or will save for retirement,2 and it could mean a larger divide between what people save and what they may need.

Planning for Health Care Expenses May Alleviate Fears

Planning for health care is almost always a priority for many of my clients. With significant uncertainty around life expectancy and potential future health needs, it is important to plan for many scenarios and the “what ifs” that may arise.

We know that planning can help give pre-retirees much more confidence in their futures. And that starts with being realistic about how much health care may cost, how much out-of-pocket costs you could pay and understanding the role of Medicare in your plan.

What Will Health Care Cost Me in Retirement?

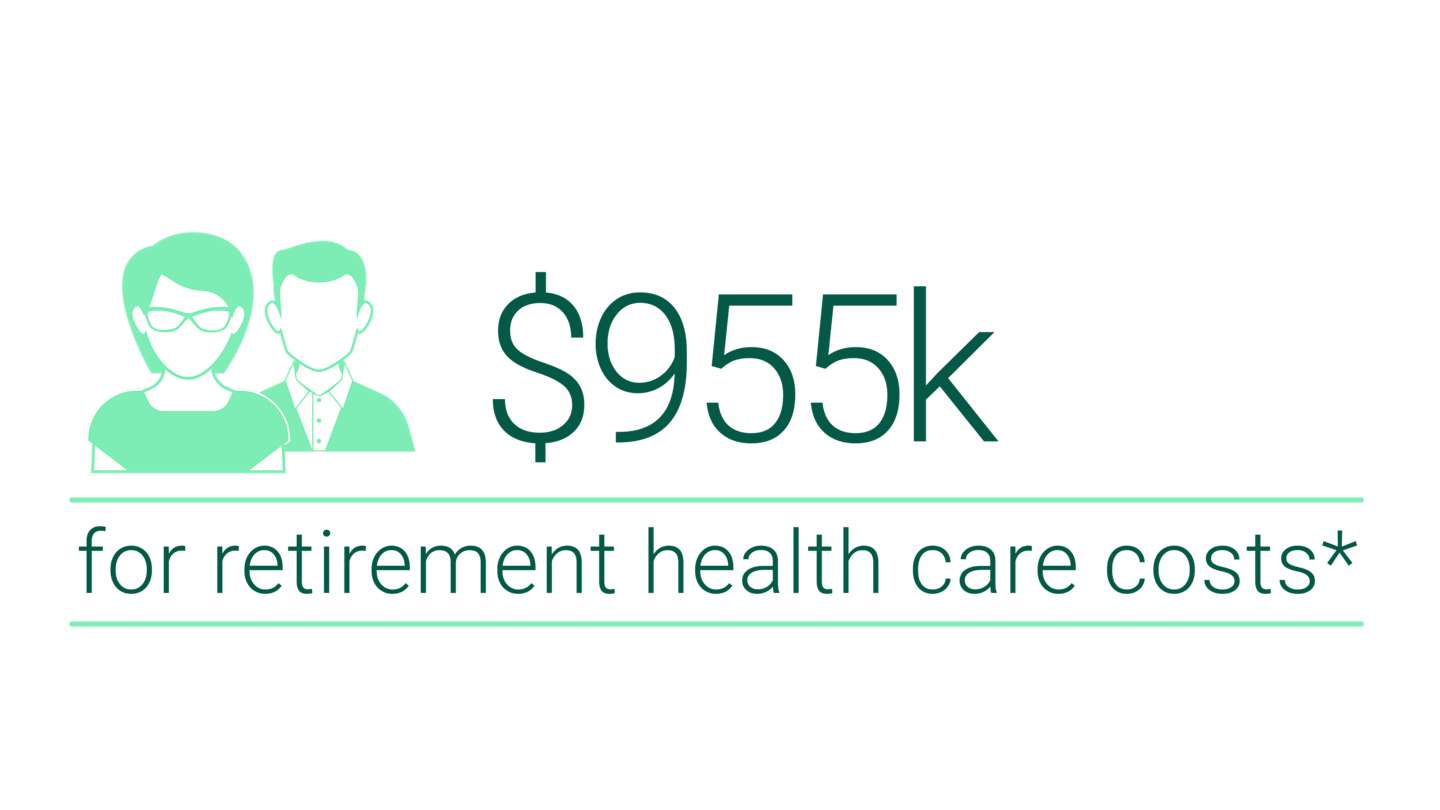

An average 65-year-old married couple retiring today may pay:

*Includes all average expenses not covered by Medicare, such as additional premiums for Medicare Parts B and D, supplemental insurance, deductibles, co-pays, and costs for hearing, vision and dental care.

Source: Health View Services 2026 Health Care Cost Data Report.

Why Is Health Care So Expensive in Retirement?

Medical advances allow retirees to turn to medical interventions. But longevity may also come at a higher price. The rate of growth of health care costs—known as health care inflation—has historically been 1.5 to 2 times3 the rate of the Consumer Price Index (CPI), one of the Federal Reserve’s indicators of overall inflation. However, in recent years, health care inflation has been even higher. Other factors can also include the following.

Retirees Shoulder More Out-of-Pocket Expenses

In their working years, many employees participate in comprehensive medical, dental and vision benefits through their employer, which also pays a sizeable share of the insurance premiums. Upon retirement, coverage premiums are borne by the individual, which increases health care costs.

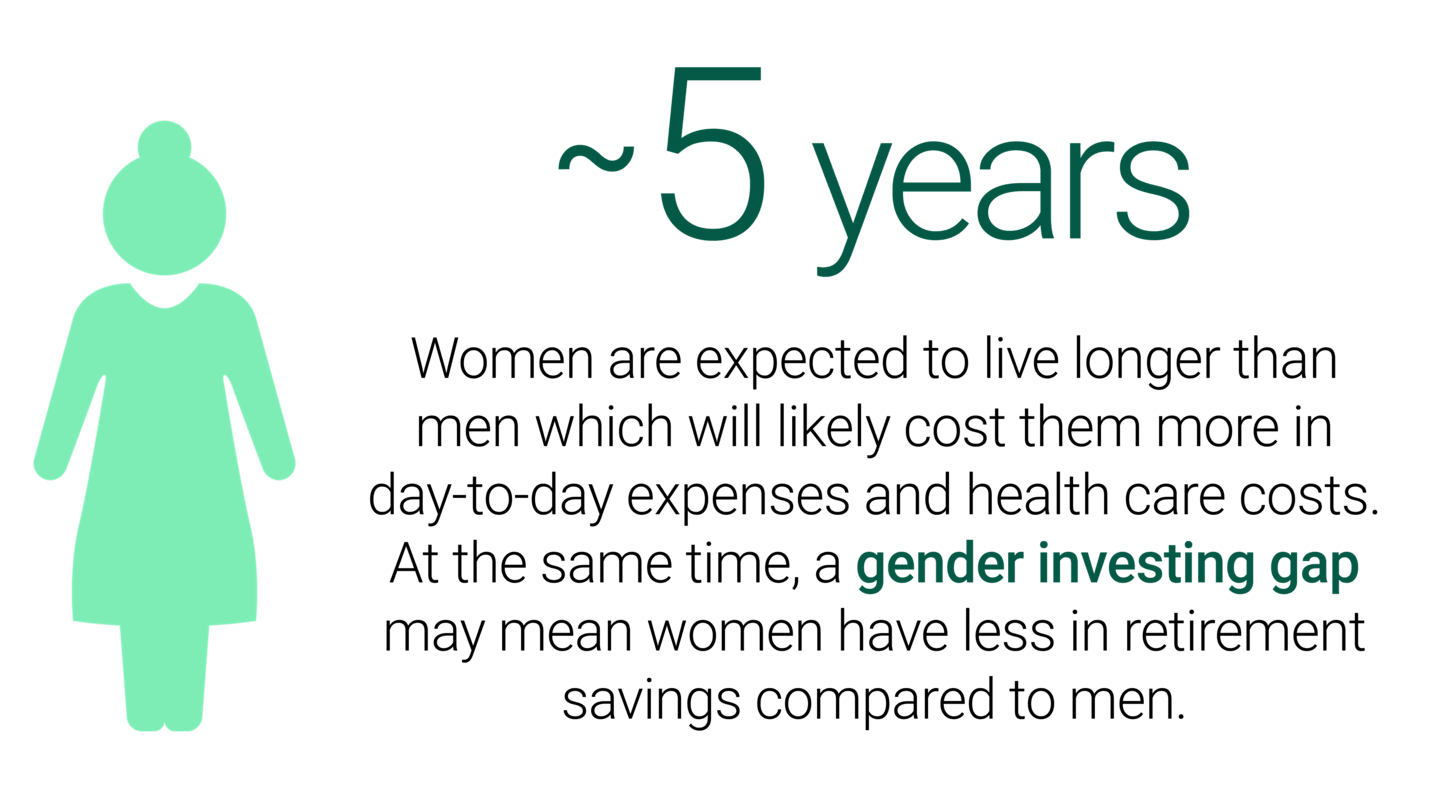

Women May Spend More on Health Care in Retirement

Women outlive men on average by several years and will likely have more health care costs because of it. On the flip side, they may have less money in retirement due to time away from work, caregiving for aging parents, spouses and children.

While female partners may help their male partners save on some health care costs by caring for them in retirement, women may add to their own expenses from the stress of caring for others and by neglecting their own health. Caregiving is likely to affect jobs and income, making saving for retirement more challenging.

Read more about the gender investing gap.

Sources: Worldometer Life Expectancy in the U.S., March 2026. Women and Investing: 2026 Trends and Strategies, SoFi, March 2026.

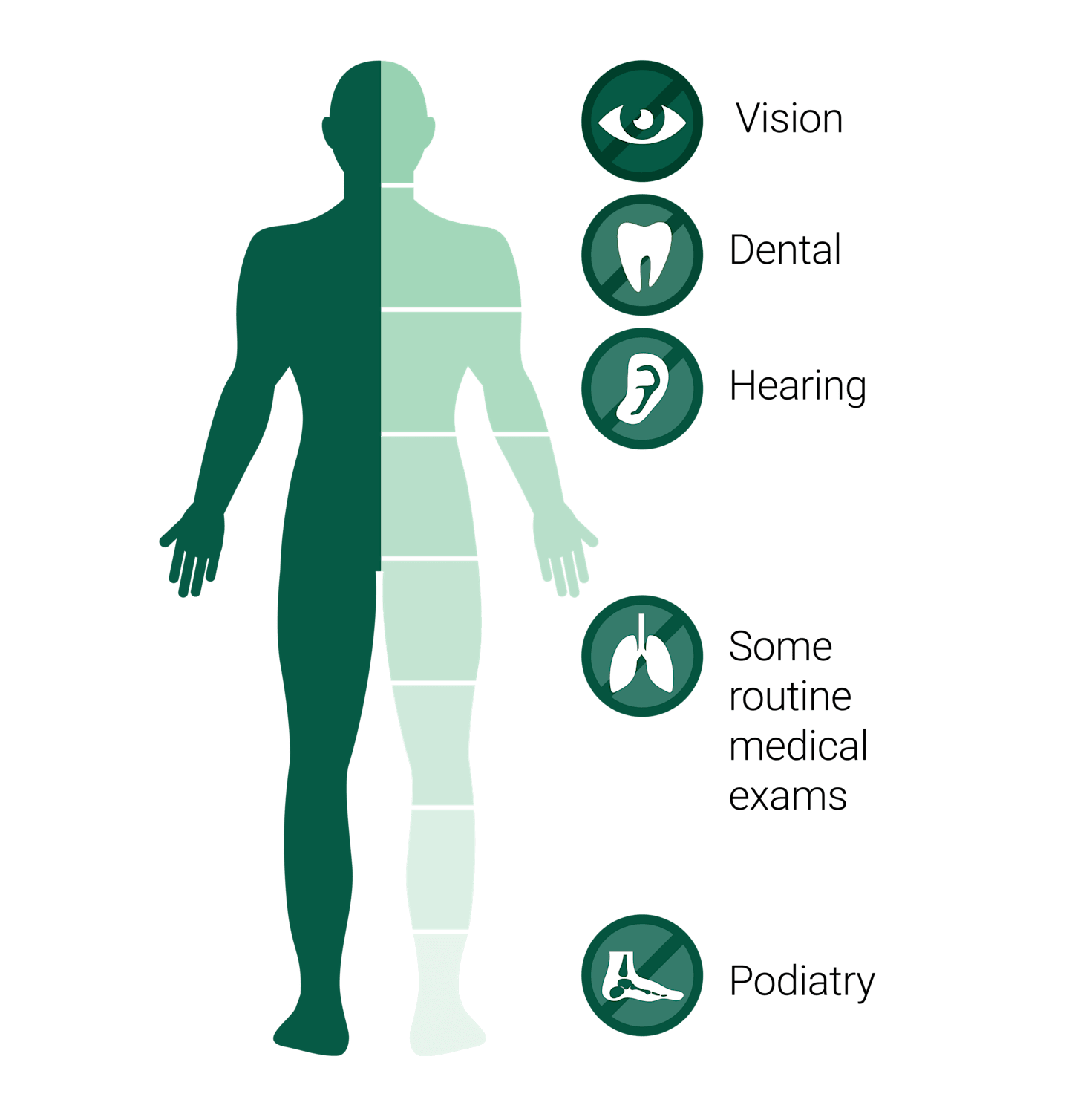

Medicare Doesn’t Cover Everything

During retirement planning reviews with my clients, the federal health insurance program, Medicare, is always a topic. It is so important to consider all costs, especially those that are not covered by traditional Medicare. And often, clients are surprised that Medicare benefits aren’t as comprehensive as they thought.

There are two ways to get Medicare: traditional Medicare (Part A and B) or a Medicare Advantage Plan (Part C). Additionally, you may optionally purchase Part D for prescription drug coverage and Medigap to help pay for coinsurance and out-of-pocket expenses under Original Medicare, such as the 20% coinsurance on Part B.

- Part A: Hospital Insurance

- Part B: Medical Insurance

- Part C: Medicare Advantage is private insurance bundling Part A, B, and usually D.

- Part D: Prescription Insurance

- Plan G or Plan K: Medicare Supplemental Insurance—Medigap. Medicare doesn't cover all types of medical expenses or long-term care in most cases.

Source: Medicare.gov, March 2026.

Source: Medicare.

How To Plan for Rising Health Care Costs in Retirement

Managing your retirement health care costs now may help you avoid using all your retirement savings on medical expenses. The key is to start planning now. Here are some steps to consider.

Explore Your Medicare Options

Learn your Medicare options.

Before you retire, take time to understand your choices: Parts A and B or Medicare Advantage Part C. Sound like alphabet soup? It's beneficial to consider your options before you're eligible.Explore supplemental medical coverage.

Medicare supplemental insurance is private health insurance that helps cover out-of-pocket expenses Medicare does not, such as deductibles, copays, and coinsurance. Policies differ from state to state and provider to provider, so it's important to do your homework.

What If Medicare Is Not an Option for You?

Sometimes, Medicare may not be the best option for health insurance. For instance, you cannot access the coverage if you retire before age 65. Also, Medicare doesn't provide insurance for dependents if you need to insure partners or children, and there may be lower-cost options for you to gain insurance. Medicare alternatives to explore include:

Negotiate a Benefit Extension With Your Employer

In some cases, you may negotiate a continuation of health insurance as part of a retirement or severance package. This is somewhat rare but can happen, and it may offer comprehensive coverage at a low cost.Stay On a Partner’s Plan

If your spouse or partner works and participates in an employee plan, adding you to the plan is likely a low-cost way to stay insured.Buy COBRA Through Your Employer

If you are close to the eligible age, you can opt to purchase COBRA coverage to continue the health insurance coverage you had through your employer for up to 18 months. This will be more expensive because your employer will no longer subsidize the premiums.Pay for Private Insurance

You may buy private coverage on your state’s exchange or through a professional association; however, this option might be expensive. You may also seek to purchase private vision, dental and hearing coverages even if you purchase traditional Medicare.

Consider a Health Savings Account (HSA)

If you're still working and your employer provides this benefit, you might want to take advantage of it. Health savings accounts can give you triple tax savings while you save and pay for medical expenses now and in retirement. It's a good idea to learn about HSAs. You may also want to talk to an advisor about how much you invest in an HSA versus your retirement accounts.

Investigate Long-Term Care Coverage

Long-term care insurance covers expenses for extended medical needs. It can include in-home services or treatments in a facility. You can choose options that fit you. Things to consider in purchasing it now are your age and your health.

What Can Affect Health Care Expenses in Retirement?

Rising health care costs are not the only thing that can affect how much you may pay for medical expenses in retirement. And there are steps you can take now to help manage what you may pay later, including taking care of your health, choosing your retirement date and selecting your insurance. Other factors can affect what you pay, but may not be within your ability to change. Let’s review each of these.

Your Health

Take care of your health today. Leading a healthy lifestyle or making changes to be healthier now can help reduce medical costs in the future. Check in with your doctor and see what changes you could make.

Your Location

Cost-of-living differences between states can vary widely. While traditional Medicare coverage is the same everywhere, supplemental, prescription Part D, and private insurance can vary across and within states.

Your Retirement Age

Besides adding to a longer period of health care costs in retirement, retiring before 65 can be costly because you don’t have access to Medicare programs.

Your Insurance Choice

Purchasing additional coverage—through Medigap, Part D and private insurance—will increase your fixed health care costs (monthly premiums) but may reduce unexpected out-of-pocket costs arising from a health event.

Your Income

If you have put aside a considerable amount for retirement or are still engaged at your job after signing up for Medicare, you may need to expend more for premiums because the government won't give as much financial aid for your expenses.

How you live in retirement may depend on how you prepare today, especially for health care expenses. Taking some of these steps can help build more confidence as you prepare yourself emotionally for retirement. Do your homework now and plan to live your best life.

Paying for Health Care in Retirement Takes Planning

Understanding Medicare benefits and planning for potential health care costs can give you a better chance of making your retirement money last. You won’t know exactly what your needs will be 10 to 20 years into retirement. Still, understanding the impacts and planning for the best, most likely and worst-case scenarios can provide more confidence as you navigate the unknowns of your retirement future.

Also note that your plan will almost certainly change in some way through retirement. Planning for your retirement and potential health care costs is one way an advisor can help you before and during your retirement years.

Get Help With Our Retirement Income Guide

Authors

Financial Consultant

Plan for Retirement and Your Health Care Costs With an Advisor

Our financial consultants can assist you in planning for all the expenses you might face during retirement. Discover the advice options available to you.

35th Annual Retirement Confidence Survey, Employee Benefits Research Institute, April 2025.

Nationwide Retirement Institute® 2025 Health Care Survey, November 2025.

Schnaidt, Scott, Why Do Healthcare Costs Grow Faster Than Overall Inflation? A Historical Perspective. November 2025.

IRS Circular 230 Disclosure: American Century Companies, Inc. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated with American Century Companies, Inc. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

This information is for educational purposes only and is not intended as tax advice. Please consult your tax advisor for more detailed information or for advice regarding your individual situation.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

American Century's advisory services are provided by American Century Investments Private Client Group, Inc., a registered investment advisor. These advisory services provide discretionary investment management for a fee. The amount of the fee and how it is charged depend on the advisory service you select. American Century’s financial consultants do not receive a portion or a range of the advisory fee paid. Contact us to learn more about the different advisory services. All investing involves the risk of losing money.