Retirement Longevity Risk: Making Your Money Last

Outliving your money is a genuine concern for many. However, you can manage longevity risk by planning, choosing investments that help and using the right withdrawal strategy.

Key Takeaways

Estimating how long your retirement savings may last is key to retirement planning. It can affect your quality of life and your confidence. But you can’t predict how long you will live.

The fear of outliving your money concerns many pre-retirees. According to our 2025 Retirement Survey, 92% said they were at least somewhat concerned. Of those, 59% were very or extremely worried.

You can help reduce longevity risk through careful planning and smart choices, even about Social Security. Understanding other retirement risks can also help.

Longevity Risk and the Fear of Coming Up Short In Retirement

Longevity risk is the possibility of outliving your money in retirement. As people live longer and worry about whether they’ve saved enough, this can create significant fears. According to American Century’s 2025 Retirement Survey, 89% have at least some concern, and 40% say they worry a great deal or can’t sleep at night about running out of money.1

One way to address longevity and its associated fears is to plan and understand how to make smart investment choices now and in retirement. Estimating how much you may need is a good starting point, including planning for a longer life than you expect. Note that longevity and life expectancy are not the same thing.

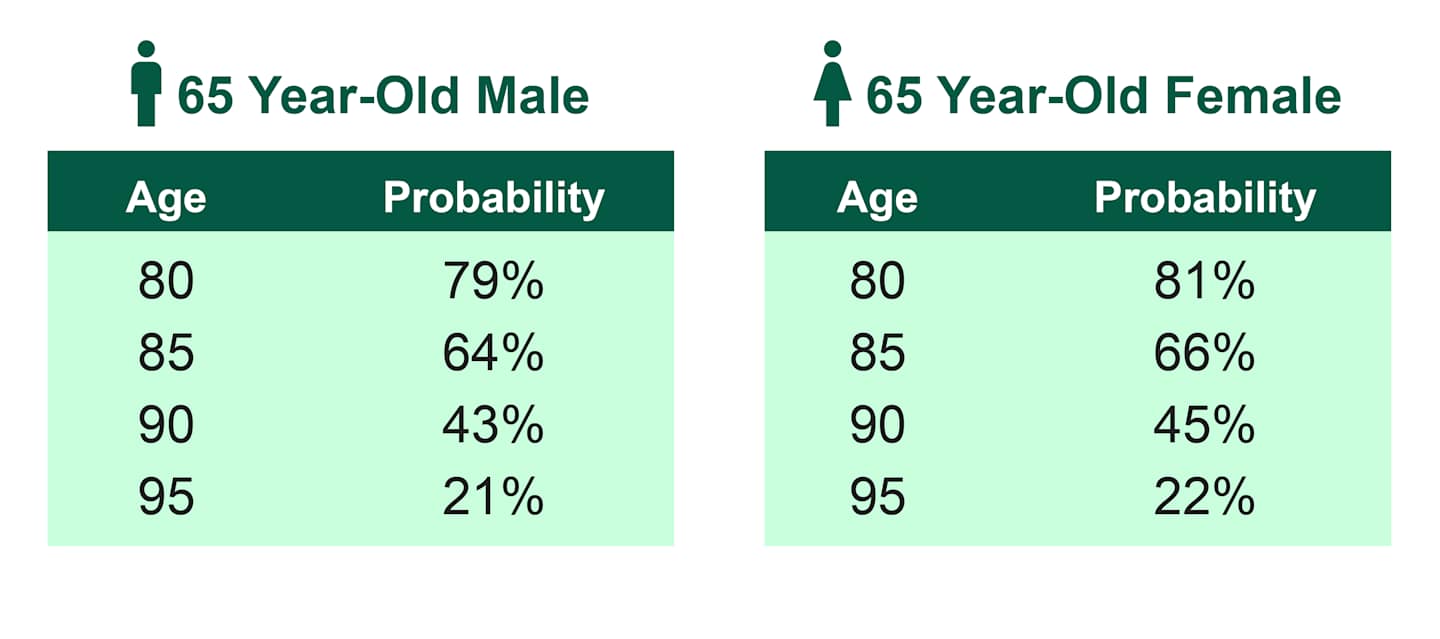

What’s the Difference Between Longevity and Life Expectancy?

Longevity—how long you might live—is often confused with life expectancy, which, according to the Society of Actuaries, is the average length of life for an individual of your age, gender and health. Longevity is a complex calculation of probabilities that can change over time.

Life Expectancy: Averages for Today’s 65-Year-Olds

Source: American Academy of Actuaries Longevity Illustrator, longevityillustrator.org, April 2026.

The Actuaries Longevity Illustrator can help forecast how long you might live based on your age, health and gender. Having a realistic understanding of how long your retirement could last can help you more effectively combat longevity risk.

How to Manage Longevity Risk? Add Balance, Not More Risk

You may think the easiest way to avoid running out of money is to aim for the highest possible investment returns. But that could mean taking on other risks that lead to losses you might not have time to recover from. At the end of the day, it’s a balancing act of managing all risks to your retirement money and not trading one risk for another.

Growth Versus Downside Risk

An example of a risk trade-off is increasing your stock allocation to pursue higher investment returns to avoid outliving your money. Stock investments generally offer higher growth potential but also increase your exposure to downside risk. Market declines occur more often than you may think. Based on our analysis of the data, the stock market has declined by 20% or more every 8 years over the past 90 years.2

What if a big decline occurs when you’re close to or in retirement? That’s known as sequence risk, the timing or sequence of your portfolio’s performance and it can have a significant impact on some investors.

Other risks can also affect your savings that you don’t have control over. What you do have control over is your investment choices and learning which ones may help you balance the risks to your retirement.

Economic Risks and Exposure to Longevity Risk

Economic factors can come in and out of play as you move toward retirement. For instance, interest rate risk becomes more important as you increase fixed-income investments closer to your retirement date, which many people do. That could also mean lower returns and potentially greater susceptibility to longevity risk.

Inflation risk also rises as retirement nears, as the loss of purchasing power can mean you need to withdraw more than planned to cover the higher cost of living.

Investing for Longevity and All Risks to Your Retirement Money

Investing for retirement should involve balancing the many risks investors face, according to our Multi-Asset Strategies team. The team developed a proprietary balance-of-risks framework for managing our target-date asset allocation funds.

Our professionals actively manage multiple risks as their relative importance changes over time and across market environments. Four key risks they manage can also help combat longevity risk.

Growth risk: The possibility that your investments don’t gain enough to see you through retirement.

Market risk: The risk that a market downturn will significantly harm your chances of having a fully funded retirement.

Macro environment risks: The chance that unexpected changes in the economy, like a recession or high inflation, will hurt investment performance.

Behavioral risks: The risk that investor decisions will hurt retirement readiness, such as abandoning a retirement plan during a market downturn.

- The loss will have more effect on investors who need their money sooner for retirement.

- It may not matter as much for those who won’t need their money for decades and have time to potentially recover from a loss.

Risk Management and a Smoother Path to Retirement

Planning for retirement can feel stressful enough, given all the unknowns. The last thing you want is for your investments to go up and down dramatically, too. Our team’s risk management process focuses on helping reduce the likelihood of large losses.

Explore Multi-Asset Solutions

Consider an already diversified portfolio designed to manage the multiple risks retirement investors face.

The aim is to generate a smoother path of investment returns, which may help more investors successfully reach their retirement goals.

You can gauge a portfolio manager’s ability to manage risks by looking at an investment’s risk-adjusted returns. “Risk adjusted” simply refers to an investment’s gain or loss relative to its risk. So, if two investments have the same absolute return over a given period, the one with lower risk has a better risk-adjusted return.

Careful Planning May Help Reduce Longevity Risk—3 Ways

Besides smart investment choices, you can also help manage longevity risks by the decisions you make before and after retirement. That includes your tax strategy, when you claim Social Security and how much you will withdraw from your investments after you retire.

1. Diversify With Pre-Tax and Post-Tax Savings

While you’re saving for retirement, you may want to think about which kinds of retirement accounts you own. Most people save in a pre-tax traditional IRA or a 401(k) accounts, which has income tax benefits now. However, diversifying with a Roth IRA or a Roth 401(k) can give you tax advantages that may help your money last longer.

You can convert some of your money from a traditional IRA or 401(k) into a Roth IRA or Roth 401(k). This means paying taxes on the converted amount now, but it also means your earnings and withdrawals will be tax-free in retirement. It’s another option that may help your money last longer by protecting it from future tax increases.

2. Take Social Security Strategically to Help Make Your Money Last

For many retirees, Social Security is a key source of income. If you can delay taking benefits, you may be able to reduce longevity risk because you’ll receive more monthly income from Social Security once you start taking it.

You may be eligible to receive benefits at age 62, and that may be the right decision depending on your situation. However, waiting until your full retirement age (which varies depending on when you were born) or until age 70 could mean a higher monthly benefit.

Married couples can benefit from planning their Social Security strategies together. Each spouse’s earnings and anticipated life expectancy help determine when and how it makes sense to claim.

Before you file, run different scenarios to see how your benefits would change depending on when you collect. You can contact the Social Security Administration up to four months before starting benefits, but you can review your options much earlier. Socialsecurity.gov is a good resource, or call 1-

Talk Over Your Social Security Claiming Strategy with an Advisor

We offer one-time consultations with a Certified Financial Planner® who can help you review scenarios for claiming Social Security and other questions about retirement planning.

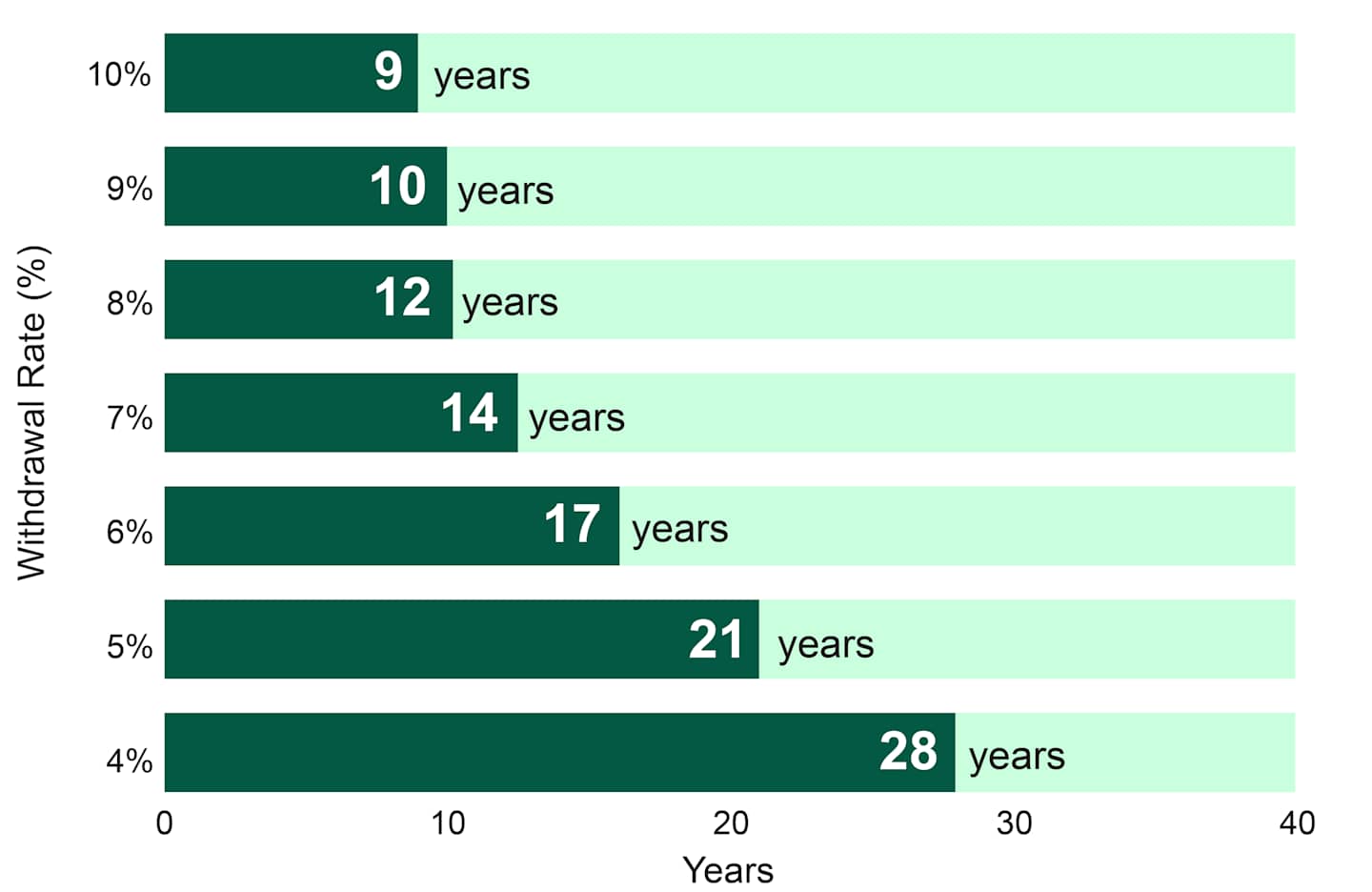

3. Choose a Sustainable Withdrawal Rate to Avoid Outliving Your Money

Of course, the rate at which you withdraw your retirement savings affects how long they will last. Your withdrawal rate is the amount you withdraw from your retirement accounts each year to cover living expenses. A sensible withdrawal strategy can help you make the most of the money you worked hard to accumulate.

A withdrawal rate that is too high can deplete your savings too soon.

A withdrawal rate that is too low means you may unnecessarily miss out on the lifestyle you really want.

In the examples below, withdrawing 10% each year may result in the money running out after nine years. That’s too short a time horizon for most people retiring now. However, reducing the withdrawal rate to 4% shows the money lasting 28 years.

Your Withdrawal Rate Impacts How Long Your Money May Last

Hypothetical Example

These hypothetical situations contain assumptions that are intended for illustrative purposes only and are not representative of the performance of any security. There is no assurance similar results can be achieved, and this information should not be relied upon as a specific recommendation to buy or sell securities. Assumes a portfolio with 50% equity, 45% bond, 5% cash equivalents over 30 years at a 90% confidence level, with the following average monthly capital market returns: stocks 7.08%, 16.00% standard deviation; bonds: 4.30%, 4.56% standard deviation; cash equivalents: 2.50%, 1.77% standard deviation. The correlation between stock and bond returns is 0.12. Inflation rate is assumed to be 2.25% annually and is included in each of the withdrawal rates depicted above. Standard deviation defines how widely returns vary from the average over a period. Source: American Century Investments, 2026.

What Are Other Retirement Withdrawal Strategies?

Typical withdrawal rate guidelines range from 3% to 5% and assume you will withdraw the same amount every year in retirement. However, the strategy you choose must fit your specific circumstances. You may want more flexibility with a dynamic approach that adjusts to market conditions, or base your withdrawal rate on your actual essential expenses.

A Dynamic Withdrawal Strategy Can Give More Flexibility

With a dynamic withdrawal strategy, you decide how much to withdraw each year based on market activity. If the economy or markets are bad, you could spend less and delay expenses until things improve. This strategy allows you to keep more money invested during difficult times and may help you recover from losses when the situation improves.

When using a dynamic withdrawal strategy, spending may vary significantly from year to year, so careful planning is required. You may plan to increase your income in good market years, but remember to save for lean years.

Income Floor Strategy Helps Cover Your Essential Expenses

An income floor withdrawal strategy helps you plan your cash flow by covering the essentials you need to live on. Think food, housing, utilities, medical costs and anything else that makes up your “needs” to determine your income floor.

Usually, investors choose income sources that won’t fluctuate much in value to cover their income floor, such as Social Security, pension income or bond dividends. That can help keep other investments, like stock funds, growing for the “wants” and help reduce longevity risk.

Tackling Longevity Risk Is Smart Contingency Planning

Accounting for longevity risk in your retirement plan means considering the probabilities of living to different ages and the financial resources you’ll need. You can think of it as contingency planning—being prepared for the unexpected.

Authors

Financial Consultant

Let Us Help You Plan for Retirement Longevity

Our financial advisors can help develop a plan based on your circumstances and objectives—and make the most of the time you have left before retirement. Choose how you want to work with us.

2025 Retirement Survey of plan participants and plan sponsors.

Source: FactSet, S&P 500® Index Returns. Average returns 1/1/1929 – 12/31/2025.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

Diversification does not assure a profit nor does it protect against loss of principal.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

Generally, as interest rates rise, the value of the bonds held in the fund will decline. The opposite is true when interest rates decline.

You could lose money by investing in a mutual fund, even if through your employer's plan or an IRA. An investment in a mutual fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

IRS Circular 230 Disclosure: American Century Companies, Inc. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated with American Century Companies, Inc. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

This information is for educational purposes only and is not intended as tax advice. Please consult your tax advisor for more detailed information or for advice regarding your individual situation.

Please consult your tax advisor for more detailed information regarding the Roth IRA or for advice regarding your individual situation.

Taxes are deferred until withdrawal if the requirements are met. A 10% penalty may be imposed for withdrawal prior to reaching age 59½.

American Century's advisory services are provided by American Century Investments Private Client Group, Inc., a registered investment advisor. These advisory services provide discretionary investment management for a fee. The amount of the fee and how it is charged depend on the advisory service you select. American Century’s financial consultants do not receive a portion or a range of the advisory fee paid. Contact us to learn more about the different advisory services. All investing involves the risk of losing money.