How to Save for Retirement at 40 or 50

Saving for retirement can feel more serious in your 40s and 50s. It may be a good time to reevaluate your finances and consider ways to increase your savings in what may be your top earning years.

Key Takeaways

Your 40s and 50s are a good time to evaluate your savings and find out if you need to do more for the retirement you want.

A good place to start is by checking in on your retirement savings progress and to start seriously considering if your finances are in order.

Review five money moves to consider between the ages of 40 and 50 that may help you increase your retirement savings.

Retirement may still seem—and be—years away. However, your 40s and 50s are important years to start thinking more seriously about your retirement plan, evaluating where you are and taking some additional steps to improve your finances, if needed.

Depending on your situation, that could mean anything from upping your monthly retirement contributions to paying off high-interest debt.

Not paying attention to retirement planning may mean some could find the balance of their retirement accounts coming up short. While those who start earlier may do better, it’s never too late to improve your retirement picture. Here are some smart money moves to consider when saving for retirement in your 40s and 50s.

Progress Report: Where Your Retirement Savings Should Be Now

A typical retirement question for people in their 40s or 50s is: How much should I have saved? Everyone’s situation is different, but here’s a quick rule of thumb to help you see where you may stand.

In your 40s, a common suggestion is to save 15 to 20% of your income and have four to five times your annual salary saved by age 50.

In your 50s, try to save 20% or more of your income, with a goal of having six to eight times your annual salary saved by age 60.

As you consider your options, keep in mind longevity risk. If you retire at age 65, you should plan on 30 to 35 years of retirement. Also, women tend to live longer than men, so it’s essential for women to actively plan to help their money last as long as they need it to.

If you’re not quite on target with your retirement nest egg, don’t despair. Instead, consider these strategies.

Start Here: Saving for Retirement vs. Paying Off Debt

If you’ve got high-interest debts, it can be hard to decide what to prioritize. Do you pay down the debt or save for retirement first? Or, set aside more for retirement and pay the minimum on your debt? While it doesn’t always feel like it, paying down debt is also an investment of sorts.

Paying off debts, such as credit cards or a personal loan, can give its own type of return, especially in your 40s and 50s. How? You may end up keeping more money by paying off high-interest debt faster because you may pay less interest overall.

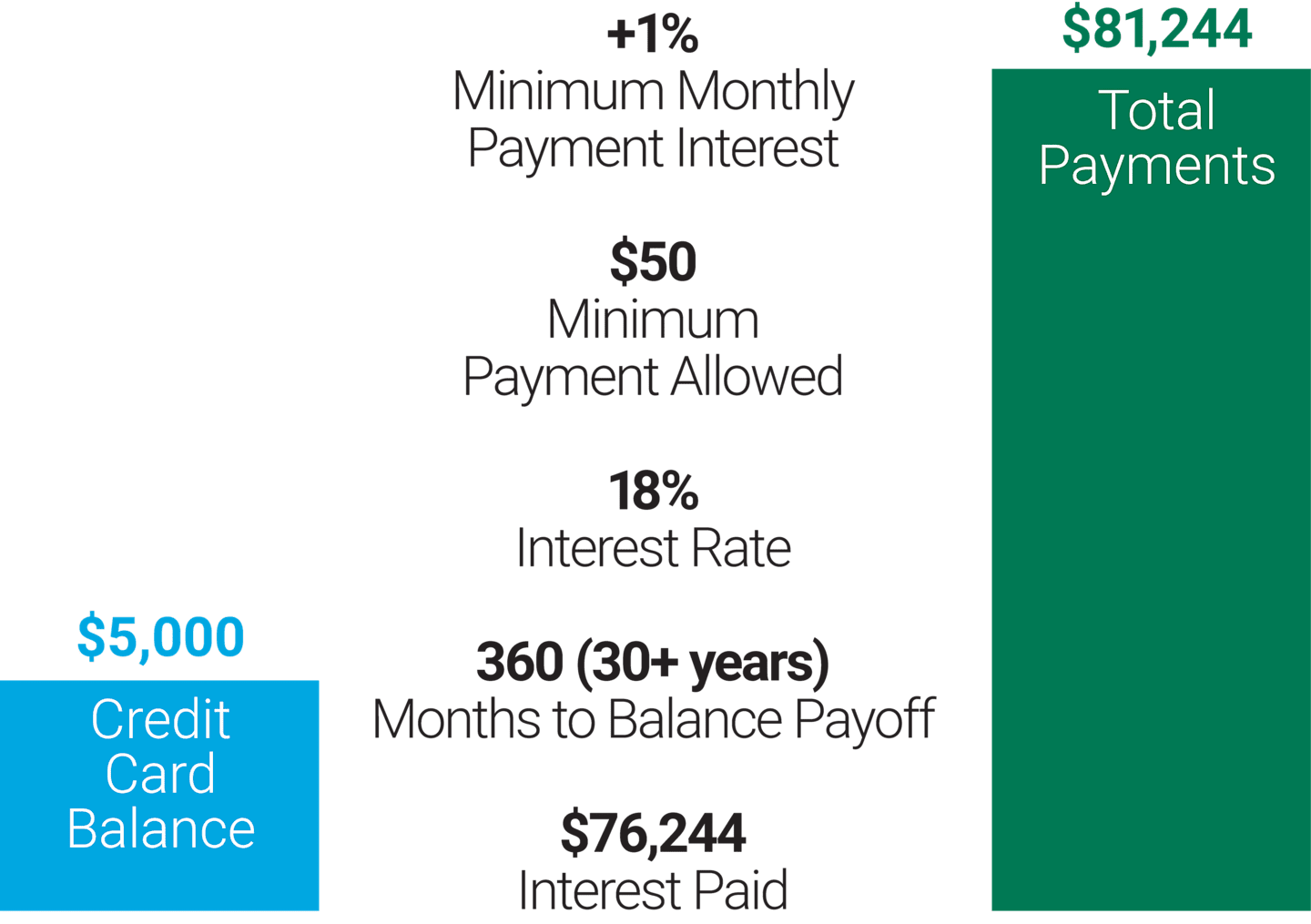

The High Cost of Paying the Minimum

The above calculation assumes you will not make additional purchases with this card. Source: Credit Card Minimum Payment Calculator, Greenpath, Inc.®, accessed August 2024.

Take credit card debt, for example. In the chart, the total interest paid is $76,244. If, instead of paying the $50 minimum, the person had invested the $50 per month at a 6% return for the same time period of 30 years, they would have close to $49,000.1,2 Take that $49,000 versus the $76,244 paid in interest, and it seems wiser to have paid off the high-interest debt first. In addition, the emotional relief that comes with paying off debt is an investment in yourself and your well-being. Tip: Once you’ve paid off that debt, think about making the same payments toward increasing your retirement portfolio. Similarly, if you get a bonus or a raise, consider investing that increase.

Stay Committed: Smart Moves When Saving for Retirement in Your 40s and 50s

With your high-interest debt reviewed, you can look for other ways to potentially increase your retirement savings. Here are some tactics to consider.

1. Take advantage of money on the table

Start looking for additional money to add into your retirement funds. Does your workplace match retirement contributions up to a certain amount? And, if so, are you meeting at least the minimum for that match?

If not, try to boost your monthly contributions to capitalize on this benefit. This can be a relatively pain-free but powerful tactic to enhance your future retirement savings, especially if you are in your 40s and can eventually max out your contributions. Otherwise, you’re leaving money for retirement on the table every month.

2. In your 50s? Take advantage of 401(k) catch-up limits

With more recent IRS guidelines, participating employees can put up to $23,500 (for 2025) of pre-tax salary each year into a 401(k) or other employer-sponsored plans such as a 403(b) or 457(b) plan. And once you hit age 50, that annual limit rises to $31,000 for 2025. Taking advantage of retirement catch-up limits can help you down the road.

3. Make your HSA a retirement vehicle

Beyond a retirement plan, does your employer offer a Health Savings Account (HSA) program with annual contributions? An HSA can be used for your medical expenses today, but it can also be used as a retirement account in the future.

Contributions you make to your HSA are tax-deductible and can gain tax-deferred earnings. While you can withdraw, tax-free, from the account for medical expenses now, once you turn 65, you can use the remaining funds as retirement income or to fund rising health care costs.

4. Consider an appropriate IRA or other account

Depending on where you are in your career trajectory, investing in different IRAs can provide different benefits. Much of your evaluation may depend on whether you think your tax bracket will be higher or lower after you retire.

If you’re in your 40s in a lower income bracket and anticipate your tax rate will go up, a Roth IRA might be the right choice. If you’re expecting to be at a lower tax rate when you withdraw from your IRA, a traditional IRA might be the better fit.

Another consideration for both Roth and traditional IRAs is that you can also make an additional catch-up contribution annually once you’re 50 or older.

Other Considerations

A question I get asked a lot is whether clients should convert their traditional IRA to a Roth. It may be something to consider if you’re looking for potential tax savings in retirement. A financial consultant can help you evaluate the pros and cons to a move like this. I believe your 40s and 50s are a good time to get those questions answered so you can decide if converting sooner or later, if at all, is the right choice for you.

In addition to IRAs, which are designed for and the “go to” for retirement, you might also consider non-retirement accounts. Having more account variety gives you more choices when you start withdrawing your money in retirement. Plus, non-retirement accounts do not have contribution limits, and you can withdraw the money without tax penalties, though earnings are taxable.

5. Set automatic investments and increases

Using automatic investments and increases can be a great tool for your retirement plan in your 40s and 50s. Automatic investments can help you eliminate the guesswork of when to make new purchases.

Automatic annual increases in payroll deductions to your employer’s retirement plan can be small like 1% to 2%. These small changes may be so gradual that you might not notice them on your paycheck. But at the same time, you’re setting more aside for retirement.

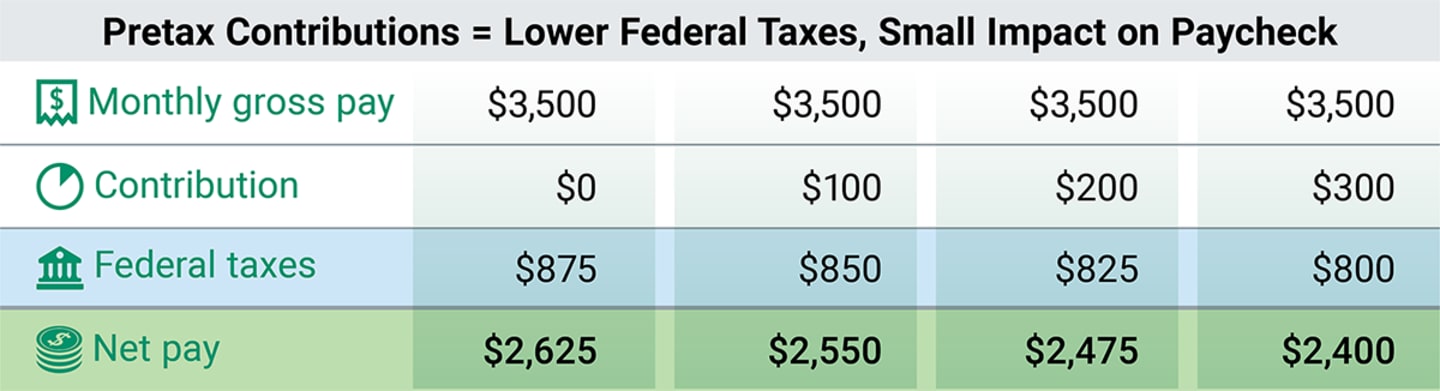

Increasing Contributions Doesn’t Have to Break Your Paycheck

Source: American Century Investments, 2025.

Table is based on an annual salary of $42,000 and assumes a monthly paycheck, single employee with no dependents and a federal tax rate of 25%. Some states also provide savings for individuals who participate in an employer's retirement plan; however, FICA (U.S. federal payroll tax) and Medicare taxes are not reduced by a contribution. Rounded to the nearest dollar.

Leveling Up: Should You Make 529 Contributions?

You can do both. If you’ve got a child or other relative you want to help with college expenses, you may consider setting up a 529 education savings plan.

A 529 plan can be a helpful way to invest for college or other education for yourself or for a loved one. But take inventory of your progress toward your own retirement funding before establishing a 529 plan. Try setting up one only after you’re on track (or even ahead) with your retirement investing.

Focus on Retirement in Your 40s and 50s

It’s important to know how much you need to save for retirement at 40 or 50 (or later in your 50s or 60s). Think about other things too. Consider factors, such as whether your account mix is diversified to align with your risk tolerance, and whether you might need to consider how to make money in retirement.

As retirement gets closer, you may want to consider enlisting the help of a financial advisor who can help with the financial planning, and help you understand when and how to take Social Security benefits when you’re ready.

Advisors can also help you create a plan for converting your savings into a steady stream of income for retirement.

Authors

Financial Consultant

Need Help With Retirement Planning?

We offer ongoing advice services with financial planning, or you can get a financial plan in a session or two with an advisor for a flat fee.

Dinkytown Future Value Calculator, American Century Investments, 2025.

The investment example is a hypothetical situation that contains assumptions that are intended for illustrative purposes only and are not representative of the performance of any security. There is no assurance similar results can be achieved, and this information should not be relied upon as a specific recommendation to buy or sell securities.

Please consult your tax advisor for more detailed information regarding the Roth IRA or for advice regarding your individual situation.

Taxes are deferred until withdrawal if the requirements are met. A 10% penalty may be imposed for withdrawal prior to reaching age 59½.

IRS Circular 230 Disclosure: American Century Companies, Inc. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated with American Century Companies, Inc. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

This information is for educational purposes only and is not intended as tax advice. Please consult your tax advisor for more detailed information or for advice regarding your individual situation.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

You could lose money by investing in a mutual fund, even if through your employer's plan or an IRA. An investment in a mutual fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

American Century's advisory services are provided by American Century Investments Private Client Group, Inc., a registered investment advisor. These advisory services provide discretionary investment management for a fee. The amount of the fee and how it is charged depend on the advisory service you select. American Century’s financial consultants do not receive a portion or a range of the advisory fee paid. Contact us to learn more about the different advisory services. All investing involves the risk of losing money.