Rollovers & Transfers: Options for Moving Money

Whether you need a new home for your old 401(k) or other retirement plan money or you’re looking for new investment options, we offer options to keep your money working for you.

Options for Your 401(k) Money

When you change jobs or retire, deciding what to do with your old 401(k) or other retirement plan can feel overwhelming. You can leave your money where it is, roll it over to an IRA or to your new employer’s plan, or cash it out—though cashing out may have penalties and the money won’t have an opportunity to grow over time.

Explore your options and choose what’s best for you and your financial future.

1. Roll Over the Money to an IRA

Rolling your 401(k) into an IRA gives you more say in how your money is invested. With a Rollover IRA, you get access to a broader selection of investments compared to most employer plans.

There’s no limit to how much you can roll over into the Rollover IRA. If you wish to add new money to the account as an annual contribution, you can combine your rollover assets and your new IRA contributions in a Traditional IRA. (See Other Rollover Considerations for important details.)

How Do I Start the Rollover Process?

Complete our online application.

Request a distribution from your current plan.

Contact your former employer or employer’s plan sponsor to request a direct rollover distribution and complete any paperwork. If a letter of acceptance from us is required, we can fax one to your former employer. Request that the check be issued as follows:

Payee: American Century Investments FBO (Your First and Last Name)

Memo Field: Your American Century Investments' IRA account number

Mailing Address: PO Box 419292, Kansas City, MO 64141-6292

Receive confirmation of deposit.

Tax-deferred earnings. Just like your 401(k), any earnings grow tax deferred and are taxed at your ordinary income tax rate when you withdraw once you reach age 59½.

Potentially lower fees. Rollover IRAs may have lower administrative and management fees than 401(k)s.

More than just retirement. The IRS allows for “special purpose” withdrawals from IRAs, such as the purchase of a first home or college tuition. Consult a tax advisor to see if this option is appropriate for your situation.

Contributions and commingling. You can't make annual IRA contributions to a Rollover IRA account, but you can combine or “commingle” the contributions and Rollover IRA assets in a Traditional IRA. Keeping the rollover money separate from contributions is required if you decide to move the rollover funds to another Rollover IRA or an employer plan in the future.

Other fees. Depending on the type of investment, you could pay higher investment fees or account expenses than you would in a 401(k).

Learn more about Rollover IRA accounts and moving money from an old 401(k).

Mutual funds. Select from a variety of no-load mutual funds based on your risk tolerance and investment goals.

Diversified portfolios. Multi-asset mutual funds combine stocks, bonds and short-term investments.

ETFs. You can invest in an ETF in a Rollover IRA through our brokerage service.

Brokerage. Choose from more than 10,000 mutual funds from other fund families, as well as ETFs, publicly traded stocks, bonds and more.

Ready to Start Your Rollover?

Complete the online rollover application or discuss your options with one of our rollover specialists.

2. Move the Money to a New Employer’s Plan

If your new employer’s 401(k) plan allows, you can roll over money from your old job’s plan. The new plan will likely have many of the same pros and cons as your previous one.

Retirement accounts in one place. You’ll be able to see your old 401(k) balance alongside your new plan money. This may make it easier to keep track of your retirement plan money.

Plan limitations. Your new plan could offer the same drawbacks as your previous plan.

Learn more about moving money to a new employer’s plan.

3. Leave Your Money With Your Old Employer

In some cases, it might make sense to leave your money in your old employer’s plan. Your investments can keep growing tax-deferred until you retire. However, if your vested 401(k) balance is under $7,000, you may not be able to use this option.

Simplicity. Your money will remain in a tax-deferred status, and you may not incur the same fees, expenses or penalties if you move it to a non-retirement account or cash it out.

Lack of control. Your former employer will continue to control the administration and recordkeeping of your account, as well as available investments.

Oversight. You may overlook the old plan when managing your finances.

Learn more about the risks of leaving money in an old 401(k).

4. Cash Out Your 401(k)—and Pay Taxes and Penalties

Cashing out your 401(k) or other retirement plan gives you quick access to your money. But keep in mind you'll owe federal income taxes (20% mandatory withholding), state and local taxes and a 10% federal penalty if you're under 59½. These costs can significantly shrink your payout.

Use our 401(k) Cash Out Calculator to see how much you could pay in taxes and penalties, and what you could be missing out on for your future.

Access for immediate needs. You may be able to cash out 401(k) money for emergencies, medical bills, unexpected expenses, etc., but you won’t receive the full amount of your requested distribution. A 20% mandatory federal income tax withholding will apply to the distribution.

Significant taxes and penalties. In addition to the immediate 20% for mandatory federal tax withholding, you’ll pay the 10% federal penalty tax (if you’re under age 59½) and any other taxes when you file your income tax return.

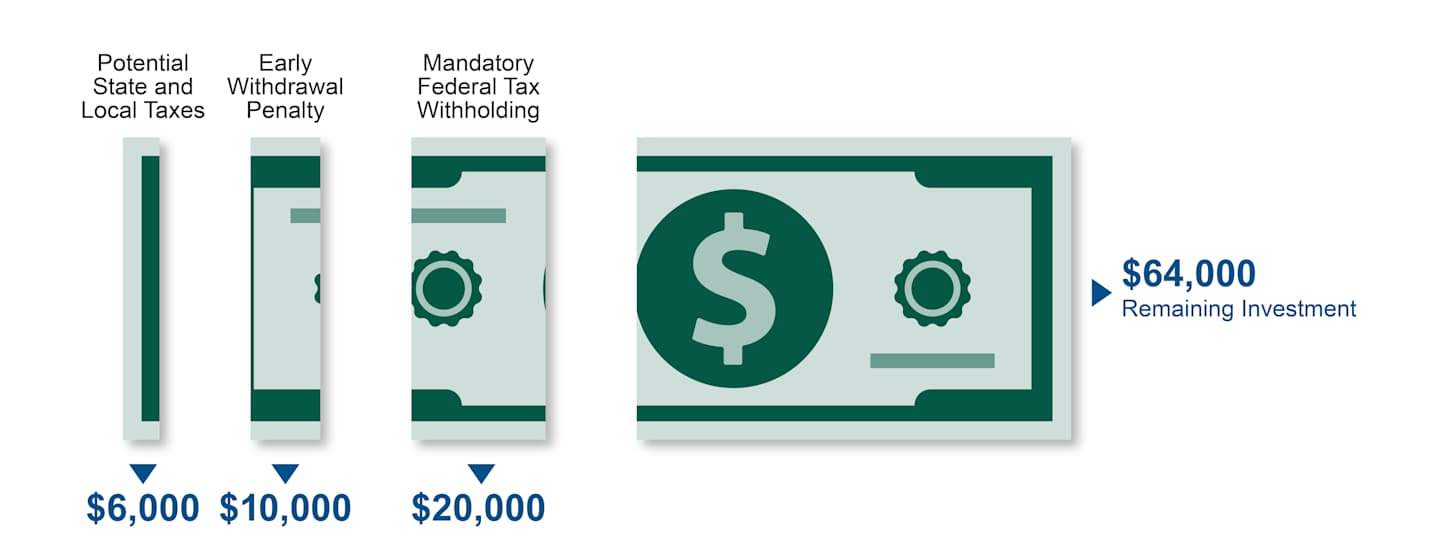

Taxes + Penalty = Potentially Losing Nearly Half of Your Money

Example of a $100,000 Cash Distribution

Source: American Century Investments. This hypothetical example assumes the following: the 20% mandatory federal income tax withholding, 6% in potential state and local income taxes and a standard 10% penalty for early withdrawal. This example is for illustrative purposes only. Please note that the 10% early withdrawal penalty does not apply to distributions made to an employee after separation from service during or after the year in which they turn 55. The 20% mandatory income tax withholding will be remitted to the IRS as a credit toward the income taxes due on your distribution. It may be higher or lower than your federal income tax bracket.

Learn more about what to consider before making an early withdrawal from your 401(k).

Transferring Other Accounts

An account transfer refers to the movement of a retirement or non-retirement account from one investment company to a similarly registered account with a new company (e.g., a Roth IRA to another Roth IRA, or a joint account to another joint account). It’s a separate process from a 401(k) rollover.

Why Make a Transfer?

Investors may move money from one investment company to another for a variety of reasons:

Seek specific investment choices.

Find specific tools or advice services.

Inherited Accounts

Have you received an inheritance? Learn more about the options available for managing and transferring inherited accounts.

Ask a Specialist for Help

The process of moving your money can seem complicated, but we’re here to help make it as smooth as possible.

The best place to start is to talk to a consultant. They’ll serve as your single point of contact and help manage the transition. A consultant can offer insights from our experience moving accounts from other firms and assist with paperwork (ours and the other company's). Finally, they will monitor the process and let you know when the assets are transferred.

How to Start Your Transfer

Gather Account Information

A recent statement from the account you are moving should have all the information you need:

Account number

Account type (individual, joint, IRA, etc.)

Name, phone number and address of the company where the account is currently held (current custodian)

Complete the Correct Form

For an IRA, complete an online application.

For an individual, joint or trust account:

Talk to a tax advisor about potential taxes. If this option is a good fit for you, contact your current company to initiate the transfer.

Complete an online application now or download an application.

For an option without taxes, transfer to a Brokerage account using a Brokerage Transfer Form and a Brokerage Application.

Mail Paper Forms

Mail the paper application and/or transfer form to the appropriate address listed on the form.

Why Choose American Century Investments?

You can build a personalized investment portfolio with a company that cares about your financial goals. American Century Investments offers a wide range of options and is dedicated to making a positive impact—both for you and the world around us.

Investment Opportunities

Build a diversified portfolio that aligns with your risk tolerance, time horizon and investment goals.

Make an Impact

When you invest with us, you can also invest in the future of others. Together, we can become a powerful force for good.

Personal Financial Advice

Choose how you want work to with us—from a one-time appointment to ongoing planning.

Ready to Roll Over or Transfer Your Money?

Contact a specialist to discuss your options and start the process of moving your money.

IRS Circular 230 Disclosure: American Century Companies, Inc. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated with American Century Companies, Inc. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

This information is for educational purposes only and is not intended as tax advice. Please consult your tax advisor for more detailed information or for advice regarding your individual situation.

IRA investment earnings are not taxed. Depending on the type of IRA and certain other factors, these earnings, as well as the original contributions, may be taxed at your ordinary income tax rate upon withdrawal. A 10% penalty may be imposed for early withdrawal before age 59½.

This information is for educational purposes only and is not intended as a personalized recommendation or fiduciary advice. There are different options available for your retirement plan investments. You should consider all options before making a decision. Our representatives can help you evaluate all of your distribution options.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

Diversification does not assure a profit nor does it protect against loss of principal.

American Century's advisory services are provided by American Century Investments Private Client Group, Inc., a registered investment advisor. These advisory services provide discretionary investment management for a fee. The amount of the fee and how it is charged depend on the advisory service you select. American Century’s financial consultants do not receive a portion or a range of the advisory fee paid. Contact us to learn more about the different advisory services. All investing involves the risk of losing money.

Brokerage Services are provided by American Century Brokerage, a division of American Century Investment Services, Inc., registered broker/dealer, member FINRA, SIPC.