Availability Bias: Mind the Generation Gap When Investing

Facing new market conditions? How you respond may be affected by when you started investing. Learn ways your age may unknowingly influence your investment decisions.

Key Takeaways

Availability bias is the tendency to place too much emphasis on information that is easily available to you.

How you react to today’s market environment of higher inflation and interest rates may be affected by when you started investing.

Using precommitment strategies can help you combat behavioral biases and emotional decisions about your investments.

When facing new situations, it’s human nature to fall back on mental shortcuts—known as behavioral biases—to help make decisions.

One common shortcut is availability bias, which is the tendency to place too much emphasis on information that is easily available to you. In other words, you're more likely to think of the risks you know (versus recency bias, which says you're more likely to consider risks you just experienced).¹

Our minds naturally reach for connections, so generational differences can affect how we handle our money without us realizing it.

“…people’s lifetime investment decisions are heavily anchored to the experiences those investors had in their own generation—especially experiences in their early adult life,” explains award-winning financial journalist Morgan Housel.²

Here’s how availability bias—and your age—could work against you when making financial and investing decisions.

Facing New Market Conditions? Beware of Availability Bias

How you react to today’s market environment of higher inflation and interest rates may be impacted by when you started investing—and availability bias could lead to misjudging risk.

For example, did you or someone close to you suffer a big loss during the 2007–2008 bear market? Investors who experienced this might be very pessimistic and cautious.

Although some caution is a good thing when investing, being overly so might cause some investors to overlook the potential for a rebound and quickly sell stocks to avoid more losses. They could also invest too conservatively to reach their goals.

On the other hand, does your investing experience begin after March 2009 when over a decade-long bull market took off? The S&P 500® Index still went through its daily ups and downs, experienced brief bear markets in 2020 (during the pandemic) and 2022 as well as some market corrections. However, the market bounced back unusually fast.

Market recoveries have not always been that dramatic, and some investors might be overly optimistic about stock market performance over time and have a portfolio heavily weighted in stocks.

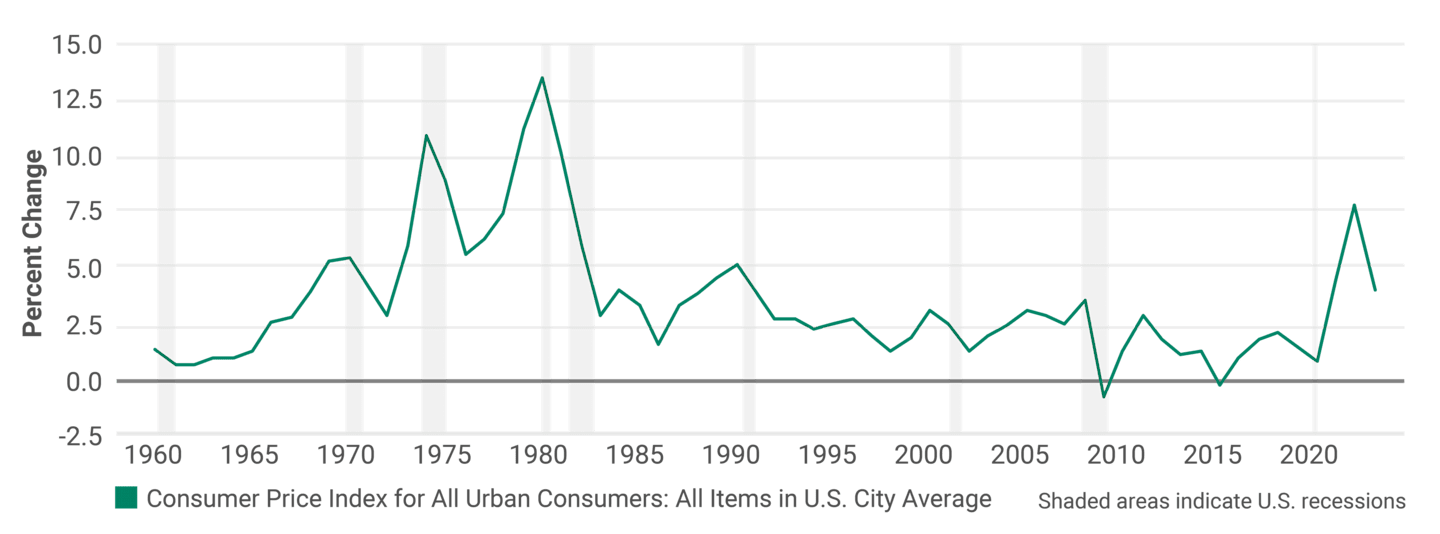

Generational experience with inflation also varies. For nearly 40 years, it was not a problem. From 1983 to 2020, the average rate of inflation was only 2.6% per year.

In contrast, older generations lived through the challenges of inflation.

One notably difficult period in U.S. economic history was the Great Inflation of 1965–1982. Energy costs rose sharply, and prices on some goods and services rose more than threefold.

During this time, baby boomers were in their prime working years—earning, spending, potentially investing their own money—while living through a disappointing period for the economy and stock returns.

Similar to today, the Federal Reserve (Fed) raised interest rates multiple times to combat stubborn inflation. This meant high mortgage rates and other borrowing costs with the federal funds rate reaching its highest point of 20% in 1981.

The line on the graph below shows the level of inflation, as measured by the Consumer Price Index. The gray areas show U.S. recessions.

Different Generations, Different Experiences With Inflation

Data from 1/1/1960-10/31/2023. Sources: U.S. Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers; FRED, Federal Reserve Bank of St. Louis.

Use our Inflation Calculator

Precommitment Strategies Can Help You Avoid Availability Bias

Studies show that emotions can take over when financial stresses hit. Precommitment strategies let you make commitments now to stop your future self from hindering your goals.

Contributing automatically to a retirement plan or savings account is an example of a precommitment strategy. By making the decision once to set aside money each month, you avoid knee-jerk reactions to market ups and downs.

Slow Down and Bring Out Your Rational Side

Social scientists sometimes say there are two separate systems of thinking.

System 1 is fast and instinctual. It helps you respond quickly in critical situations, but it can be impulsive.

System 2 is more reflective and deliberate. It helps you with long- and short-term planning and setting goals.

In investing, headlines and global events can feed system 1 behaviors, such as buying high and selling low. Slowing down your responses with system 2 thinking can make you less susceptible to availability and other behavioral biases.

Get the latest Views You Can Use.

Talking to Your Generation: How Every Age Can Use a Financial Plan

Working with a financial professional can help you be more aware of biases in your decision-making. Of course, financial needs are specific to each person and will grow and change as you age.

For older Gen Xers and baby boomers, plans likely will focus on retirement—accumulating as much as they can, planning for the retirement income they need and how they will manage finances and investments in retirement. They may also be thinking about transferring their wealth to heirs.

For younger Gen Xers and older millennials, the key to financial planning may be building up savings as much as possible while juggling life’s many priorities. Other millennials and up-and-coming Gen Zers can find support for starting their financial journeys.

Learn more about getting financial help at any age.

We’re Here to Help

Perceptions and biases can lurk under the surface—preventing you from objectively assessing the facts of a situation. Knowing about availability bias can be helpful for investors and those working with them.

The right partner can be an invaluable resource.

Get More Tips and Insight on Inflation

Jones, Kyle Bradford. How to Avoid Two Common Biases. University of Utah Health, 22 December 2017.

Housel, Morgan. The Psychology of Money. Harriman House, 2020.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.