Sequence of Returns Risk: Why Timing Matters

Can two investors get the same returns and end up with different results? Here's how the timing of investment returns can impact your portfolio over time.

Key Takeaways

Sequence risk refers to the order of investment returns (early or late in life) and the impact those returns will have when you need the money.

The consequences of poor performance are magnified when you’re closer to retirement, when your investment balance is likely at its peak.

Gradually lowering the stock exposure in your portfolio as you approach retirement is one strategy to help avoid larger losses.

The volatility of the stock market plays a major role in your account balance over time—for better and for worse. But even though stock market risk is an inherent part of investing, there’s another angle you might not be considering: the timing, or sequence, of your portfolio’s performance.

Why Your Sequence of Returns Matters

Investors in and around retirement often have large sums of money saved up. Those at the beginning of their careers might have small amounts, but they have more time to keep adding to their portfolios and for those investments to compound (i.e., earn money on the investments and on any earnings after that).

A major market correction of 20%, for example, will have more of an effect on investors who need that money for retirement income right now and don’t have time to recover from a loss. A 20% decline might not matter as much for investors who have decades to go before they start spending.

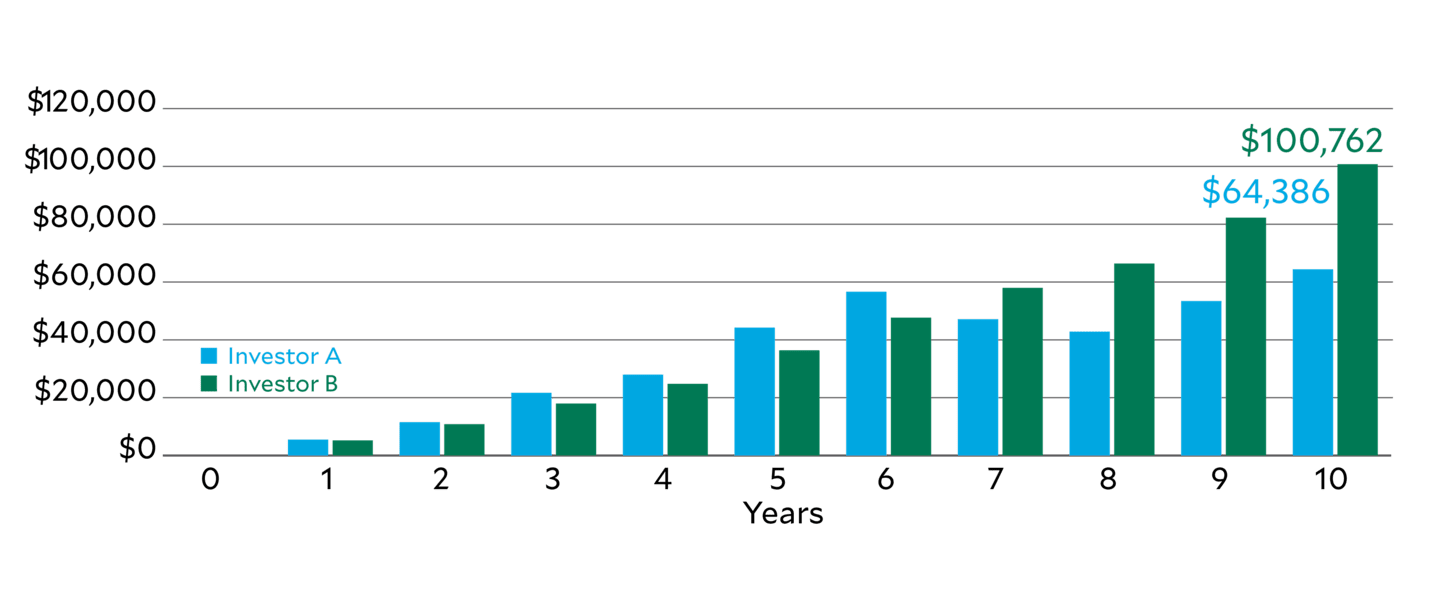

Sequence Risk in Action: Two Investors, Two Different Outcomes

Can two people who invest the same monthly amount and get the same returns end up with different portfolio values? Almost certainly.

The reason lies in each of their portfolios’ sequence of returns and the principle of compounding returns over time.

Same Returns

Same contributions: $400 per month

Same holding period: 10 years

Same average returns: 176% (cumulative) or 10.7% (average)

Different Outcomes

Investor A ends with $64,386

Investor B ends with $100,762

Why?

Everything was equal except for when they experienced gains and losses.

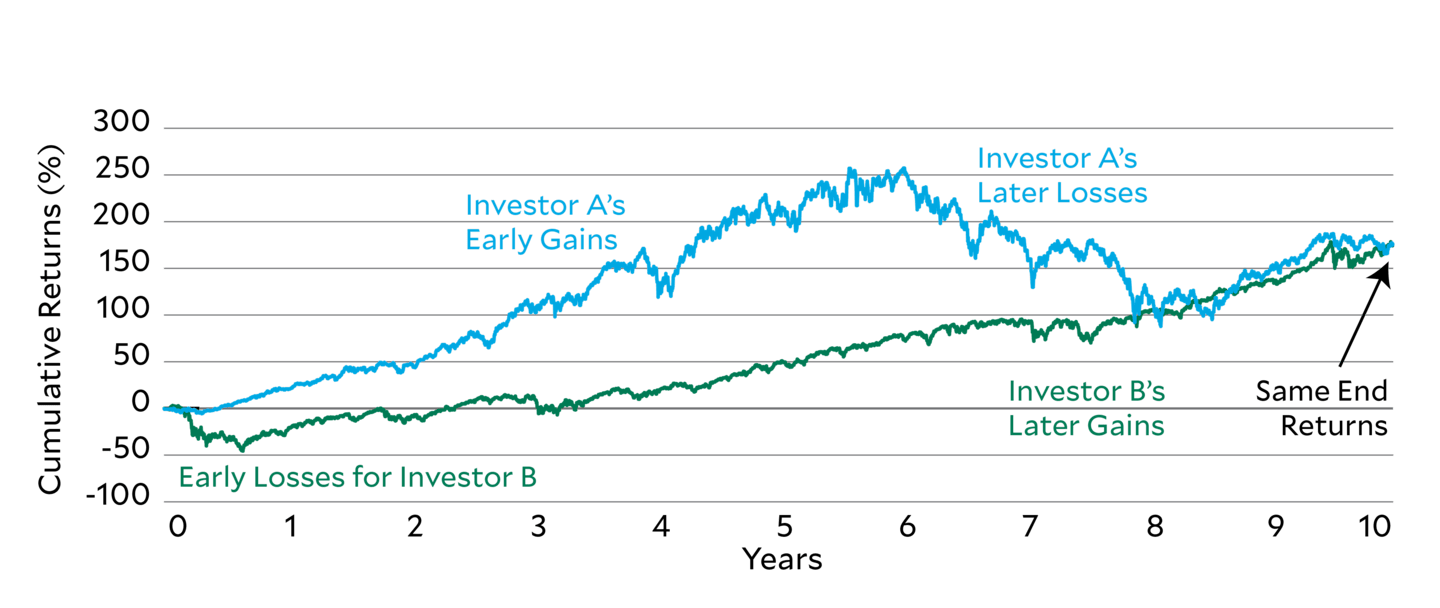

Here’s how we came up with those numbers. Investor A and Investor B both invested $400 a month—but during two different 10-year periods. Investor A’s 10-year investment is represented by actual S&P 500® Index returns from 9/1/1994 to 8/31/2004. Investor B's investment is represented by S&P 500 returns from 8/1/2008 to 7/31/2018.

Each 10-year period had the same cumulative return (176%) and average annualized return (10.7%). But notice how the path to those returns was very different.

Early or Late Returns? Timing of Market Gains and Losses

Source: Morningstar Direct. The stock market is represented by the S&P 500® Index between 9/1/1994 to 8/31/2004 (Investor A, blue) and between 8/1/2008 to 7/31/2018 (Investor B, green). Data assumes reinvestment of dividends and capital gains. The index does not reflect fees, brokerage commissions, taxes or other expenses of investment. Investors cannot invest directly in an index. Past performance is no guarantee of future results.

Investor A was the clear winner early on. Investor B had a rocky start, but it didn’t result in major dollar losses because of the small investment balance at the time. Eventually, Investor B experienced slow, steady, compounding returns.

But when Investor A ran into a few tough years, there wasn’t enough time to recover. The negative returns during the second half of the period had much more of an effect on the larger investment balance.

The result? Investor A ended up with $36,376 less. Remember, the cumulative and average annual returns were identical. The timing of the performance and its effect on the larger investment balance are what made the difference.

Late Losses Drag Down Investor A’s Final Balance

Source: Morningstar Direct. The stock market is represented by the S&P 500® Index between 9/1/1994 to 8/31/2004 (Investor A, blue) and between 8/1/2008 to 7/31/2018 (Investor B, green). Data assumes reinvestment of dividends and capital gains. The index does not reflect fees, brokerage commissions, taxes or other expenses of investment. Investors cannot invest directly in an index. Past performance is no guarantee of future results.

Sequence Risk and Retirement Withdrawals

What does this mean for you? The bad luck of bad stock performance right before or soon after retirement—when your investment balance is likely at its peak—could have a significant impact on your standard of living when you’re relying on investment income.

If you had planned for a certain withdrawal rate from your investments (4% for example), but the value of your portfolio decreased due to a market decline, you may have to adjust that percentage to account for a lower portfolio balance.

In fact, many investors who retired just before or after the 2008 stock market crash or the COVID-19 recession in 2020 had to deal with similar declines in the value of their portfolios.

Does That Mean Stocks Are Too Risky?

While stocks might get a bad rap because several types of events can cause them to be volatile, most people still need the growth potential of stocks before and even during retirement. The trick is to balance your need for growth by complementing your stocks with other investments—like bonds—that tend to behave differently in various market conditions and can potentially lower your risk of large losses.

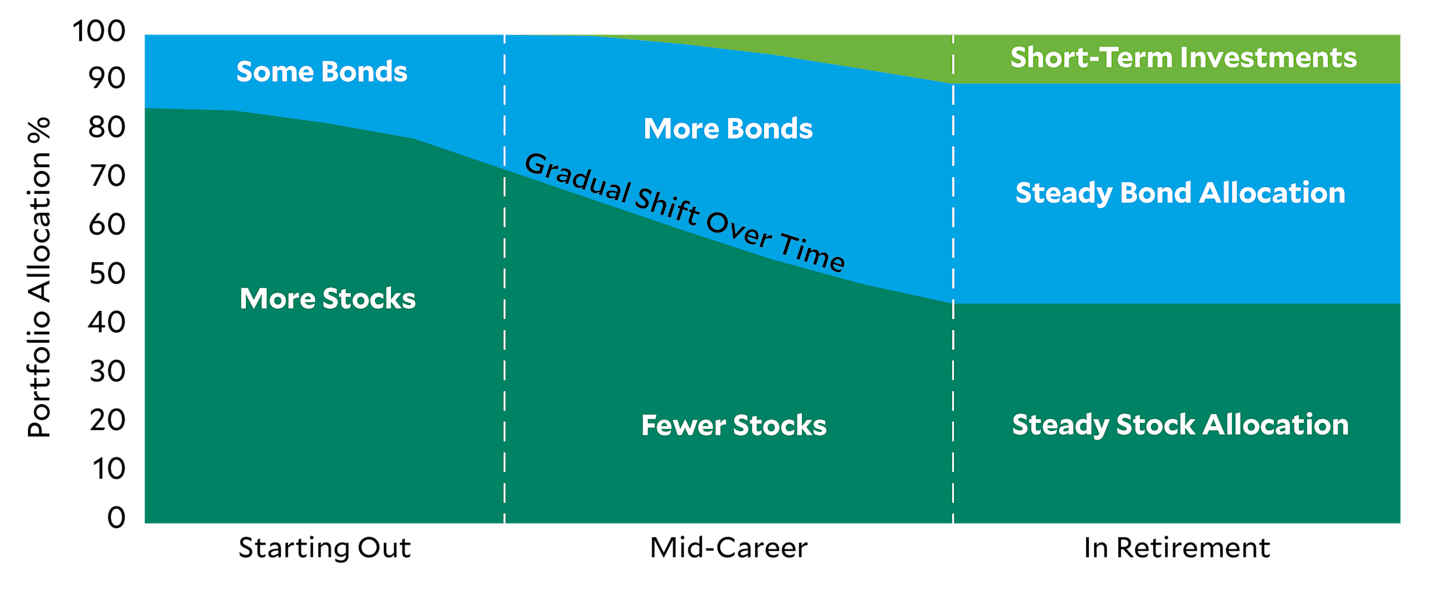

How much of each do you need in your portfolio? That depends on your comfort with risk and your time frame. But our research indicates that a gradual approach to reducing stocks and adding bonds might better manage sequence risk and temper the risk of market volatility.

Your Path Can Help Manage Sequence Risk

You never know what your sequence of stock returns will be, but you can adjust your portfolio to account for this risk. Gradually lowering your stock exposure is one way to help you avoid larger losses as you approach retirement.

That decrease is called a glide path, and it’s a key feature of target-date funds—broadly diversified portfolios that automatically adjust from a stock-heavy growth focus to a more conservative allocation.

A glide path’s “slope” describes how quickly or slowly the change in stock allocation occurs. The quicker the decline—the steeper the slope—the more you could be affected by the sequence of investment returns. Flatter glide paths aim to offer greater potential for smoother rides.

Balance Your Stocks and Bonds Over Time

Sample Portfolio Shift

Source: American Century Investments. Each investor's situation is different. This chart is for general educational purposes only.

Does Your Portfolio Need To Shift?

If you’re headed toward retirement with a portfolio full of stocks, it might be time to reevaluate. A diversified mix of stocks, bonds and short-term investments (like short-duration bonds or money markets) is ideal—as long as it matches your goals.

No one can control the timing of downturns. Even professionals who manage and adjust a portfolio for you, as with target-date funds, can’t ignore sequence risk. But understanding its impact can help you make more informed decisions when managing your portfolio.

Authors

Financial Consultant

Is Your Portfolio at Risk?

Whether you’re far from retirement or your last paycheck is right around the corner, we can help you build a portfolio (or find an appropriate target-date fund) to help manage sequence risk.

Diversification does not assure a profit nor does it protect against loss of principal.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

Generally, as interest rates rise, the value of the bonds held in the fund will decline. The opposite is true when interest rates decline.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

©2026 Morningstar, Inc. All Rights Reserved. Certain information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.