How Do I Choose Investments?

You’re ready to start putting your money to work for your future. Now, it’s time to choose investments. But how? Learn your options, what to consider when selecting investments, how to put it all together and the choices you have with us.

What Are My Investment Options?

A good place to start is understanding the broad asset classes of stocks, bonds, and cash equivalents. Learn how each can play a crucial role in your portfolio.

Stocks

Add Potential to Grow Your Assets

Investing in the growth of various companies and the economy as a whole can offer higher return potential than bonds and cash but also carries a greater risk of losses.

Bonds

May Provide Income and/or Less Volatility

Higher-quality bonds tend to do well when stocks decline, which may help manage risk. Bonds may also provide income. However, usually the higher the yield potential, the lower the credit quality—meaning there’s a greater risk the issuer could default on payments.

Money Market Funds

Have Access to Money and Help Preserve Capital

These funds typically hold fixed-income securities that mature within one year, such as U.S. Treasury bills. Although that offers a low average annual return, it provides more stability of principal as you get closer to withdrawing money from your portfolio.

Multi-Asset

A Diversified Portfolio in a Single Fund

Multi-asset funds combine stocks, bonds and short-term investments, targeting either a specific risk level or the date you’d like to use your money.

Mutual Fund or ETF—Which to Use?

Choosing between a mutual fund and an ETF may depend on your objectives, the level of flexibility you desire, your views on taxes, or if you’re interested in the simplicity of having an automatic investment.

All mutual funds and ETFs have specific investment objectives, features and costs to consider. You can choose both and combine them with individual stocks and bonds to customize your portfolio. The primary difference between mutual funds and ETFs is how they are bought and sold.

A mutual fund's net asset value (NAV), or the price of a single share, is calculated once per day after market close. All trades are based on the day's NAV.

ETFs are securities that trade like individual stocks on an exchange, and as a result, can experience price changes as they are bought and sold throughout the day. Generally, an ETF's price is the market value of the underlying securities at the time of the trade.

Log in to your brokerage account to trade American Century® ETFs commission-free or open an account today.

Learn more about the differences between ETFs and mutual funds in the areas of tax advantages, trading flexibility and fees.

How Do I Choose Investments That Are Right for Me?

Choosing the right investments begins with understanding certain elements about your goals and yourself. These three steps can help you get there and know which investments may work best to help you achieve your goals, and a portfolio based on knowledge rather than guesswork.

Step 1. Define Your Financial Goal(s)

Knowing what you want to invest for, how long until you’ll need the money and how much you’ll need to have is a good place to start.

Name It

Know what you're investing for. Is it retirement, a college education for yourself or a child, general investing to grow your current savings or some other goal?

Date It

Determine the time frame for when you'll need the money from your investment. Different goals may require different timelines and different strategies.

Estimate the Amount

Add up how much you may need for each goal. Our calculator can help you determine how much you may need to invest depending on timing and your goal amount.

Terms like risk tolerance and diversification are coming up. Learn some of the basics from our 101 guide to investing.

Step 2. Know Your Risk Tolerance

Choosing investments that are right for you means understanding the type of investor you are. Terms like "aggressive," "moderate," and "conservative" refer to the level of risk you are comfortable taking.

What’s My Risk Tolerance?

Investing involves risks and knowing your risk tolerance can help you determine how much of the market's ups and downs you can tolerate and find balance in your portfolio.

It can help you choose a mix of investments that might suit your situation, depending on how conservative or aggressive you want to be.

Remember that not taking enough risk with your investments is a risk too. A more aggressive portfolio may be suitable for goals that are many years in the future, such as retirement for individuals in their 20s and 30s. The opposite may be true for someone just a few years from retirement who doesn’t have time to recoup losses from a market downturn.

Ready to learn your risk tolerance level?

Answer a few questions to learn your comfort level. You’ll also find sample portfolios that may fit your risk level.

Step 3: Know Your Investing Style

In investing, “style” can refer to various things, such as the investment approach a portfolio manager uses when constructing a portfolio. Examples include a growth style, where the primary goal is to maximize returns, or a value style, where the manager seeks to achieve results by purchasing investments they believe are undervalued. Your personal investing style is your approach to making investment decisions.

What’s My Investing Style?

Making investment decisions can feel daunting, especially when you’re just starting out. However, it ultimately comes down to understanding how you prefer to make decisions. Some people prefer to conduct their own research and draw their own conclusions about what will work for them. Others lack the time or inclination to conduct extensive research and prefer to work with a financial professional.

We offer investment guidance to help you understand all your options so you can make an informed decision. If you would like a professional recommendation, our advice services are available. If you’re unsure, we can help you determine which service is best for you.

Building Your Portfolio—What to Consider

Now that you’ve figured out what your goal is, when you’ll need the money, how much you’ll need, how much risk you want to take and your personal investing style, it’s time to bring it all together into your actual investment portfolio.

Mix It Up to Manage Risk

A key strategy is to select a mix of diverse investments to build a well-diversified portfolio. Diversification is a common term you’ve likely heard but can sometimes be misunderstood.

How much of each type of asset (stocks, bonds, cash equivalents and others) you choose will depend on your tolerance for risk. This will be your asset allocation. Explore the differences between asset allocation versus asset classes.

Learn the truth about diversification and how to choose a mix of investments that helps manage risk in a portfolio.

Why Do I Need a Diversified Portfolio?

Markets are unpredictable. Combining different investment types can help you better prepare for various market conditions and may also help provide more consistent, less rocky returns over time.

Diversification should extend beyond the general categories of stocks, bonds, and cash equivalents (such as money markets). Each of these can be further divided into specialized categories, potentially targeting different market segments.

Is it easy to build a diversified portfolio?

Choosing a mix of stocks, bonds, and other asset classes isn’t necessarily hard, but it’s important to know how to pick ones that don’t move in the same direction when markets shift.

If you prefer a simpler approach, consider a pre-diversified portfolio managed by experienced investment professionals. They’ve done the research and selection for you.

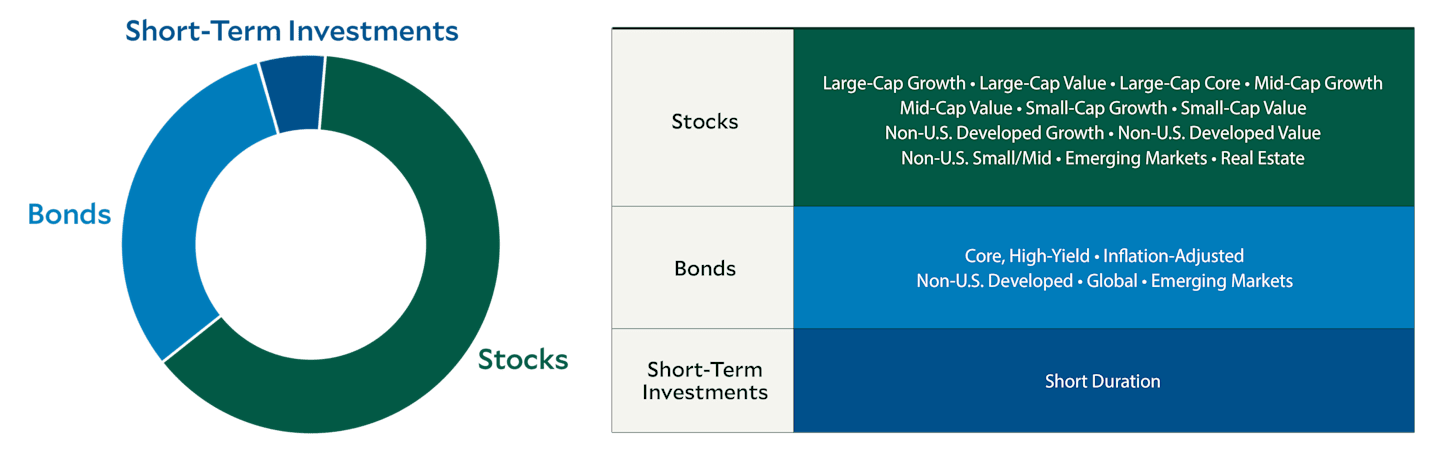

Putting It All Together: A Sample Portfolio

There are many ways to construct a portfolio. The right mix for you should take into account your timeline, risk tolerance and future goals. In this example, you can see several choices from each of the larger categories of stocks, bonds and short-term investments.

Your Options for Building a Portfolio With Us

Choose a Pre-Diversified Portfolio

No time or inclination to research and make all your own investment choices? Put our professional money managers to work for you with a pre-built portfolio based on your timeline or risk level.

Build Your Own Portfolio

Create a diversified portfolio with our broad lineup of no-load mutual funds. Our complete list includes stock, bond, asset allocation and money market funds for you to choose from.

Choose a Brokerage Account

Select from more than 10,000 mutual funds from other fund families, as well as ETFs, publicly traded stocks, bonds and more.

Get Personal Financial Advice

Don’t want to go it alone? You don’t have to. Choose our advice services, from a one-time session with a certified financial planner to in-depth, ongoing advice and planning.

Investing and Your Finances

Investing can be a crucial part of your overall financial picture and a way to practice a healthy financial habit. However, there’s much more to your finances, including budgeting, building an emergency fund, creating a comprehensive financial plan and managing debt. Discover ways to manage your finances.

Not Sure Where to Start?

Our investment consultants are available to help. Start by requesting a call back.

Exchange Traded Funds (ETFs) are bought and sold through exchange trading at market price (not NAV), and are not individually redeemed from the fund. Shares may trade at a premium or discount to their NAV in the secondary market. Brokerage commissions will reduce returns.

Generally, as interest rates rise, the value of the bonds held in the fund will decline. The opposite is true when interest rates decline.

Diversification does not assure a profit nor does it protect against loss of principal.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

American Century's advisory services are provided by American Century Investments Private Client Group, Inc., a registered investment advisor. These advisory services provide discretionary investment management for a fee. The amount of the fee and how it is charged depend on the advisory service you select. American Century’s financial consultants do not receive a portion or a range of the advisory fee paid. Contact us to learn more about the different advisory services. All investing involves the risk of losing money.

Brokerage Services are provided by American Century Brokerage, a division of American Century Investment Services, Inc., registered broker/dealer, member FINRA, SIPC .