Tax-Loss Harvesting With ETFs: A Guide to Lowering Your Tax Bill

Investment losses can be hard to swallow. The good news is that losses may come with a silver lining in the form of potential tax benefits.

The excitement of selling an investment for a profit can quickly turn to dismay when an unexpected, hefty tax bill appears. However, there is an effective way to help manage those costs—tax-loss harvesting. It’s a strategy that allows investors to offset gains from one investment with losses from another investment. With a bit of planning, you can.

Here’s a basic guide for using tax-loss harvesting to potentially lower what you may owe the IRS while maintaining long-term investment goals.

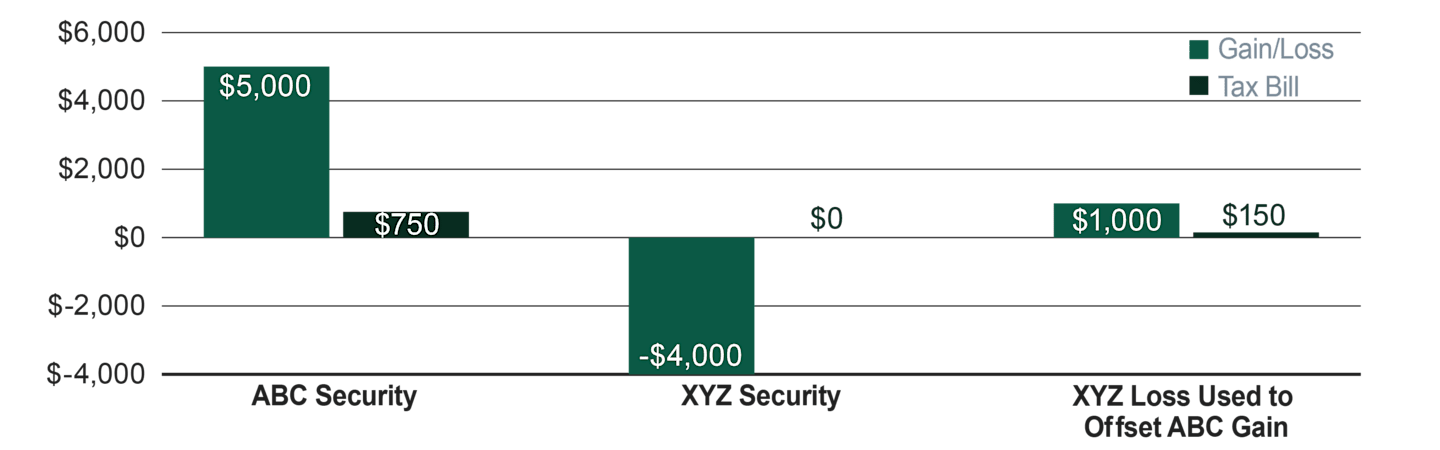

How to Use Tax-Loss Harvesting to Reduce Tax Liability (Example)

- The hypothetical long-term loss from the sale of XYZ partially offsets the long-term gain from the sale of ABC.

- This example assumes a capital gains tax rate of 15 percent. This rate varies by filing status and income.

- The offsetting loss results in a tax savings of $600.

Tax-Loss Harvesting Rules, Risks and Common Mistakes

Following a few general guidelines could help you take advantage of this opportunity and may help avoid running afoul of the IRS’s wash sale rule. Remember, everyone’s situation is different. Please consult a tax advisor for your individual situation.

NOTE: Specific security types, such as municipal bonds, may be subject to additional rules. Please consult your tax advisor.

Key Tax Law Updates for Investors

Reviewing each portfolio’s capital gains tax exposure is an important component of a holistic financial planning approach.

Below is an overview of some recent changes in tax law that you should keep in mind when tax planning:

Overview of the 2025 Tax Bill, One Big Beautiful Bill (OBBB)

In July of 2025, One Big Beautiful Bill was signed into law. For many taxpayers, this prevented tax increases that would have occurred if the Tax Cut Job Act (TCJA) of 2017 had expired in December of 2025.

Reference: | OBBB Provisions

Tax Impact of Long-Term vs. Short-Term Capital Gains*

There’s a significant tax advantage to holding onto assets for longer than a year, since long-term cap gains tax rates (0%, 15%, 20%) are much lower than short-term cap gains tax rates (taxed as ordinary income).

Qualified dividends are taxed at the long-term capital gains rate and ordinary dividends and income paid on bonds is taxed at the ordinary federal income tax rates.

Note that the Medicare Surtax of 3.8% applies on net investment income above certain thresholds.

Investors may also deduct up to $3,000 in losses from their income each year.

If capital losses exceed gains in a given year, they can be carried forward indefinitely until gains are depleted.

Taxes may apply on gains from the sale of a main residence above a certain gain exclusion (net of improvements and exclusions), yet losses on their sale cannot be deducted.

IRS Tax Inflation Adjustments to Know

The Internal Revenue Service annually updates multiple tax provisions to reflect inflation, which can affect standard deductions, tax brackets, credits and other thresholds.

2025 Tax Year

For the 2025 tax year (generally, tax returns filed in April of 2026), the OBBB Act (passed in July 2025) included increases to the standard deduction, significantly increased the cap on the state and local tax SALT deduction, and added a new seniors tax deduction.

2026 Tax Year

Changes for the 2026 tax year include increased standard deductions, additional inflation adjustment to the income tax brackets, and maintaining the raised cap on the SALT deduction among other deductions.

Reference: IRS Tax Inflation Adjustments for Tax Year 2026

IRS Wash-Sale Rule and What It Means for Tax-Loss Harvesting

The IRS’s wash sale rule is designed to keep investors from claiming artificial losses, so it’s critical to understand it if you’re planning to harvest losses.

The rule prohibits the sale of a security in order to claim a loss if the investor repurchases it—or a “substantially identical” security—within 30 days before or 30 days after the sale for a total of 60 days. Violating this rule could negate the potential tax benefits from the transaction. How does the IRS define “substantially identical” security? Unfortunately, they have not identified specific criteria.** Nevertheless, to determine the potential for a wash sale violation, there are some factors that investors may want to consider, including the degree of holdings overlap and the difference in prospective returns. The greater the holdings overlap and the more similar the prospective returns, the greater the possibility of a wash sale classification by the IRS.

The IRS’s e-learning resource walks you through the ins and outs of the rule and provides examples: IRS Courseware - Link & Learn Taxes

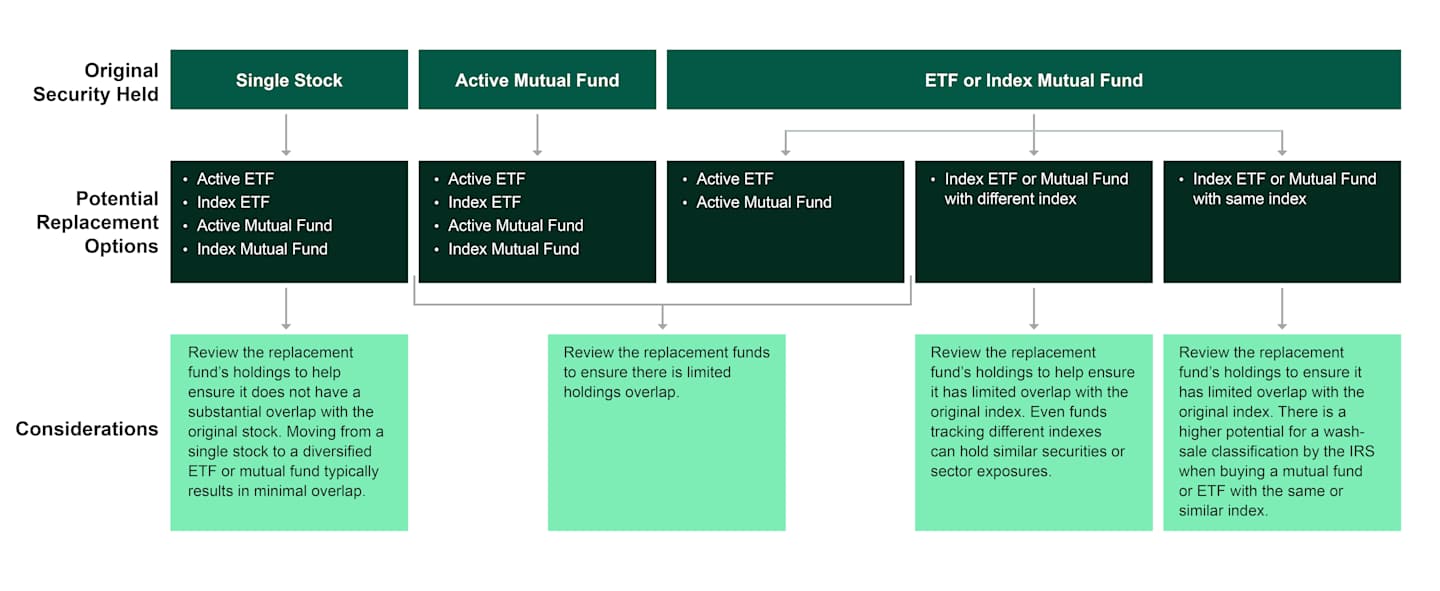

Many investors consider Exchange Traded Funds (ETFs) as well as active and indexed mutual funds as effective tools to gain desired portfolio exposures. But remember, they can fall in the substantially identical category if holdings overlap too much.

The following framework provides an overview of the extent to which ETFs, active mutual funds, and index mutual funds may feature low portfolio overlap as well as differences in prospective returns under various scenarios.

Visual Breakdown of Key Tax-Loss Harvesting Considerations by Investment Type

Note: You should consider the replacement fund’s investment objectives, risks and charges and expenses carefully before you invest.

Tax-Loss Harvesting Do's and Don'ts

Use our framework as a starting point for year-end tax planning discussions.

Long- and short-term capital gains are taxed at different rates. Long-term gains may only be offset by longer-term losses. Likewise, short-term gains may only be offset by short-term losses.

As of March 1, 2026, the Internal Revenue Service has not released a definitive opinion regarding the definition of “substantially identical” securities and its application to the wash sale rule and ETFs. The information and examples provided are not intended to be a complete analysis of every material fact and are presented for educational and illustrative purposes only. Tax consequences will vary by individual taxpayer and individuals must carefully evaluate their tax position before engaging in any tax strategy.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

IRS Circular 230 Disclosure: American Century Companies, Inc. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated with American Century Companies, Inc. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

This information is for educational purposes only and is not intended as tax advice. Please consult your tax advisor for more detailed information or for advice regarding your individual situation.

Exchange Traded Funds (ETFs) are bought and sold through exchange trading at market price (not NAV), and are not individually redeemed from the fund. Shares may trade at a premium or discount to their NAV in the secondary market. Brokerage commissions will reduce returns.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.