ETFs: 3 Levels of Liquidity for Greater Market Access

ETFs have different layers of liquidity that allow investors to trade ETFs in amounts that can far exceed an ETF’s ADV without significantly affecting the price.

Key Takeaways

ETFs offer three levels of liquidity—on-screen liquidity, broker-assisted liquidity and specialist-accessed liquidity.

The average daily volume of an ETF shows only what has been traded, not what could have been traded.

The creation and redemption process helps ensure that an ETF’s share price aligns with the value of the underlying securities.

Although the liquidity of an exchange-traded fund (ETF) can seem complex, it comes down to recognizing that it goes beyond visible trading volume. It encompasses not only the trading of the ETF shares themselves but also the liquidity of the underlying securities in the ETF’s portfolio. And it’s the vehicle’s unique creation and redemption process that gives it the depth of liquidity to dynamically respond to investor supply and demand.

Trading Volume Does Not Equal Liquidity

The average daily volume (ADV) has always been a strong indicator of liquidity for stocks, but it’s a common misconception that it’s the sole indicator of an ETF’s liquidity. In reality, ADV is only what has been traded of an ETF, not what can be traded of an ETF. That’s because, unlike stocks that have a set number of shares, new ETF shares can be created and existing shares can be redeemed based on investor demand.

Due to the creation and redemption process, ETFs have different layers of liquidity that allow investors to trade ETFs in amounts that can far exceed an ETF’s ADV without significantly affecting the ETF’s price.

3 Sources of ETF Liquidity

There are three levels of liquidity to consider for ETFs: on-screen liquidity, broker-assisted liquidity and specialist-accessed liquidity.

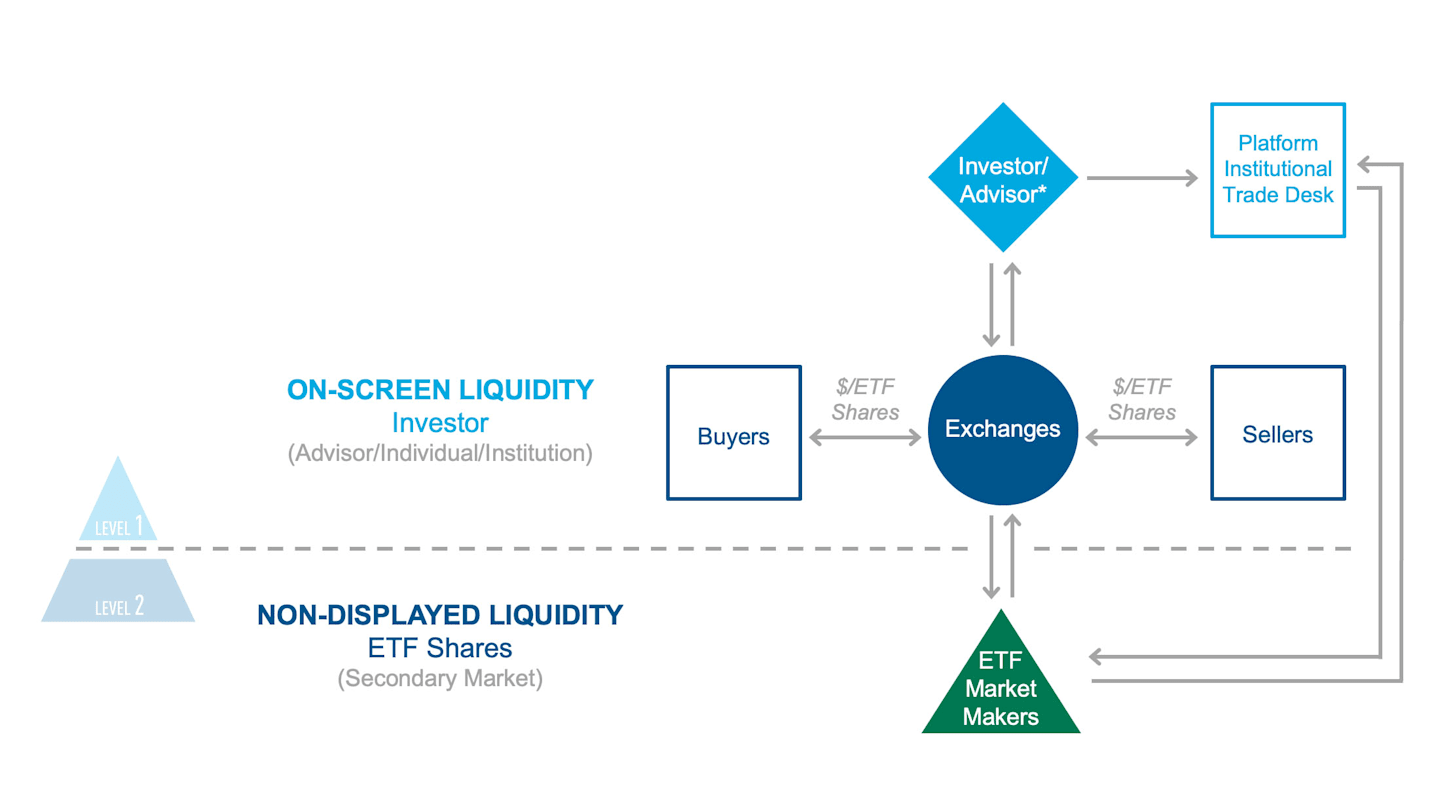

On-Screen Liquidity

The most visible source of ETF liquidity is on-screen liquidity, which the average investor can see via a variety of sources, such as financial websites. On-screen liquidity represents the trading activity that has already occurred on the exchange and is visible in the secondary market where ETFs are priced and traded like stocks.

A market maker publishes quotes in the secondary market that show the price of available ETF shares it’s willing to buy and sell. Market makers help maintain a fair and orderly market and are always ready to buy available ETF shares from potential sellers and sell ETF shares to potential buyers at share sizes that they assign to their quotes.

Typically, there are two prices for an ETF visible to the public. From the brokers’ perspective, there is the price at which they are willing to purchase a specific number of ETF shares (known as the bid) and the price at which they are willing to sell a specific number of ETF shares (known as the offer or ask). The difference between the two prices is called the spread.

It’s important for investors to consider the spread because it affects the cost of trading an ETF. Because ETFs hold multiple securities in the portfolio, the spread of those securities also influences the spread of the ETF. Essentially, the weighted spread of the underlying securities that the ETF holds is the basis of the spread of the ETF.

Broker-Assisted Liquidity

On-screen liquidity is limited on public financial websites. Most often, investors have access to only the highest bid and lowest offer and the number of shares that are assigned to the quotes. They won’t see all the quotes in an ETF’s order book on the exchange. Investors can access this level of liquidity with the assistance of a broker, who can see additional levels of quotes that represent additional prices at which ETFs can be traded.

Additionally, market makers will publish quotes beyond the visible liquidity for most ETFs. This helps provide market depth. Market makers do this so that larger-size trades can be executed while covering their costs of providing liquidity.

By sending a limit order to a broker, an investor can buy or sell ETF shares at a stated price beyond the on-screen liquidity. The broker buys or sells ETF shares up to the limit price requested. Alternatively, investors can contact a broker’s ETF block desk, which handles large purchases and sales of ETF shares.

If offered, the broker or advisor’s custodian (a financial intuition that looks after the clients’ funds or investments) may have an institutional trade desk that can assist in ETF trading. The institutional trade desk has professional traders with direct access to ETF market makers who will compete for the order. Institutional trade desks are great resources particularly for midsize to large ETF orders.

*Investor access exchanges through their trading platform.

Investors and advisors have access to ETF on-screen liquidity via a financial website but can only see what is available to them. With the assistance of a broker, investors and advisors have access to the ETF shares in the secondary market.

Specialist-Accessed Liquidity

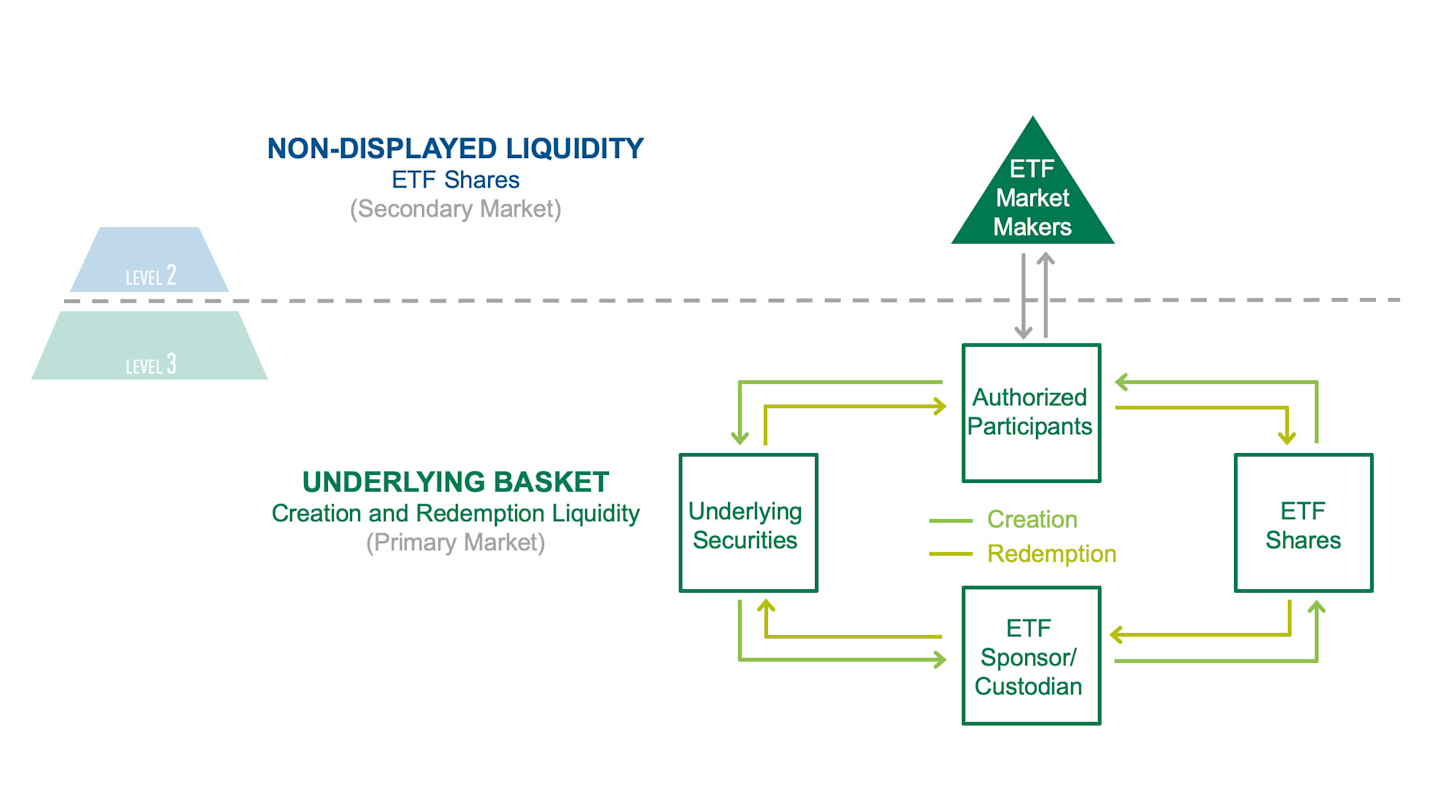

The bulk of ETF liquidity is in the primary market, where the ETF market makers can access the liquidity of the underlying securities they hold. Here, the creation and redemption mechanism, which is an important process for ETFs, comes into play.

When buying or selling a large number of ETF shares—on the scale of thousands—ETF market makers can reach out to large institutions that act as authorized participants (AP) to create and redeem large blocks of ETF shares directly from the ETF provider or its custodian.

The Creation and Redemption Process Ensures ETFs Liquidity

The creation and redemption process ultimately ensures there is sufficient inventory to fill investors’ orders. It allows large buy or sell trades to be executed in the ETF with little or no impact to the market.

For the creation of an ETF share, the AP assembles a portfolio or basket containing the ETF’s underlying securities. The AP then turns the basket over to the ETF custodian, who holds all the securities in the ETF. In return, the custodian delivers ETF shares that can be bought and sold in secondary markets. This is generally done in blocks of 25,000, 50,000 or 100,000 ETF shares.

The Creation and Redemption Process

The ETF creation and redemption process occurs when an ETF market maker either needs to create or redeem ETF shares if there are not enough or there are too many shares available on the secondary market.

The creation and redemption process helps keep supply and demand in balance and leads to an ETF share price that is generally in line with the value of the underlying securities.

Resources Are Available To Help You Access Liquidity

Remember, the volume of the ETF represents only what has been traded, not what could be traded. You’re not alone when trading ETFs. From small to large ETF trades, you can take advantage of the ETF community of professionals and the resources and tools they can provide. Their jobs are to support advisors in fulfilling their clients’ needs.

And if you have questions around trade execution, you can always contact the American Century Investments capital markets desk through your American Century Investments® or Avantis Investors® representative.

Contact Professionals To Help You Execute ETF Trades

Institutional Block Deck

- Advisors who are on institutional platforms have access to institutional block desks for ETF orders. These desks provide trade guidance, execution expertise and advice on trading strategies.

- The platform’s website or advisory help center will have contact information for the institutional block trading desk.

Broker-Dealer ETF Trade Desk

- Advisors or institutional investors who are not on an institutional platform or do not have access to an institutional block desk should contact their broker-dealer ETF trade desk.

- Sales representatives at the broker-dealer should be able to direct advisors to the relevant ETF trade desk.

ETF Issuer's Capital Markets Desk

- ETF specialists are available to discuss trade execution and provide overall guidance.

If you have questions about trade execution, please refer to the tools provided above or contact the American Century Investments capital markets desk through your American Century Investments or Avantis Investors representative.

Diverse Approaches, Independent Thinking

Explore our ETF lineup in depth.

Exchange Traded Funds (ETFs) are bought and sold through exchange trading at market price (not NAV), and are not individually redeemed from the fund. Shares may trade at a premium or discount to their NAV in the secondary market. Brokerage commissions will reduce returns.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.