Understanding the U.S. Dollar: Why It Matters to You

From travel costs to everyday purchases, the dollar’s value can make a difference.

Key Takeaways

A stronger U.S. dollar often means cheaper imports and more affordable overseas travel, while a weaker dollar can raise costs but boost U.S. exports.

Currency fluctuations impact international investments because returns depend on both local market performance and exchange rate movements.

You can’t predict dollar moves, but understanding their ripple effects can guide spending and long-term portfolio diversification.

You’ve probably seen and heard headlines like “The dollar is strong” or “The dollar is weak.” It sounds like something only currency traders care about, right? But the truth is that these shifts probably affect your daily life: sometimes you’ll notice them, sometimes you won’t.

Think about your upcoming vacation, the price of the latest tech gadget or even your investment returns. The dollar’s value can affect all of these. Let’s explore what’s behind these headlines and why it should matter to you.

How Does the Dollar’s Value Affect Your Life?

Currency fluctuations are most evident in the cost of goods you buy and the vacations you plan.

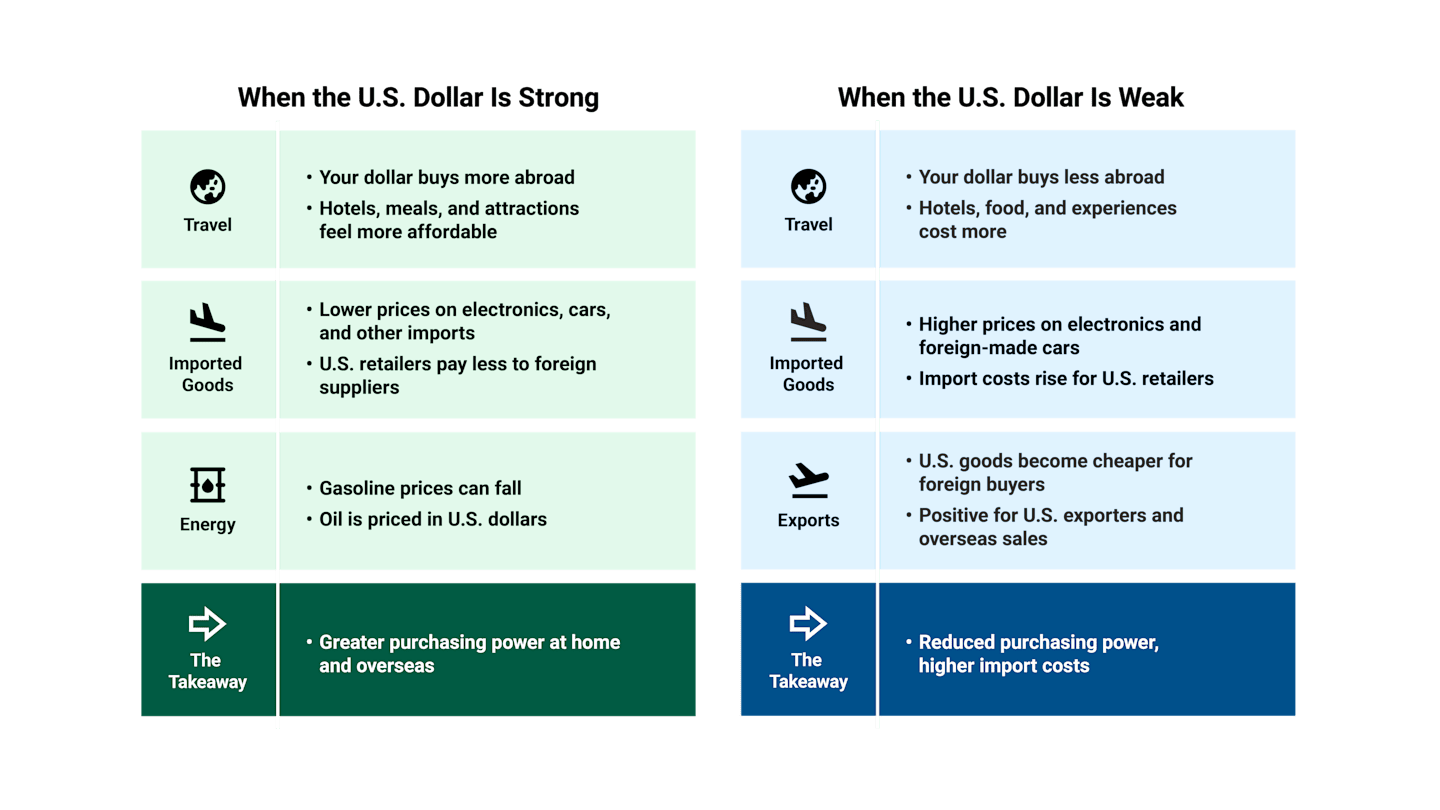

When the Dollar Is Strong

If you’re booking a trip to Paris, a strong dollar means your money buys more euros. Your boutique hotel might feel more affordable, and the cost of your steak frites won’t break the bank.

When you’re shopping back in the U.S., you may find that imported goods such as smartphones, laptops and cars often cost less. That’s because U.S. retailers pay lower prices to foreign manufacturers. Even gasoline prices can go down because oil is priced in U.S. dollars per barrel.

When the Dollar Is Weak

What if we flip the script and the dollar is weak? On that same trip to Paris, your dollar would buy fewer euros. Everything from hotel rooms to meals would cost more, so you might find yourself picking budget-friendly meal options to stretch your travel funds.

Back home, the prices of imported electronics and foreign-made cars may rise. On the bright side, U.S. exporters may welcome a weaker dollar because their products would become bargains to overseas buyers, leading to higher sales.

Figure 1 | How the Dollar’s Value Influences Everyday Life

Why Does the Dollar’s Value Change?

The dollar often moves in response to economic forces. You can think of it like a seesaw, balancing confidence with global demand.

The U.S. dollar is the world’s primary reserve currency. This means it’s the main currency global traders and central banks rely on for transactions and savings. Oil, gold and many other commodities are priced in dollars, and governments also hold U.S. dollars as part of their foreign reserves.

The dollar's prominence helps explain why its fluctuations affect economies worldwide.

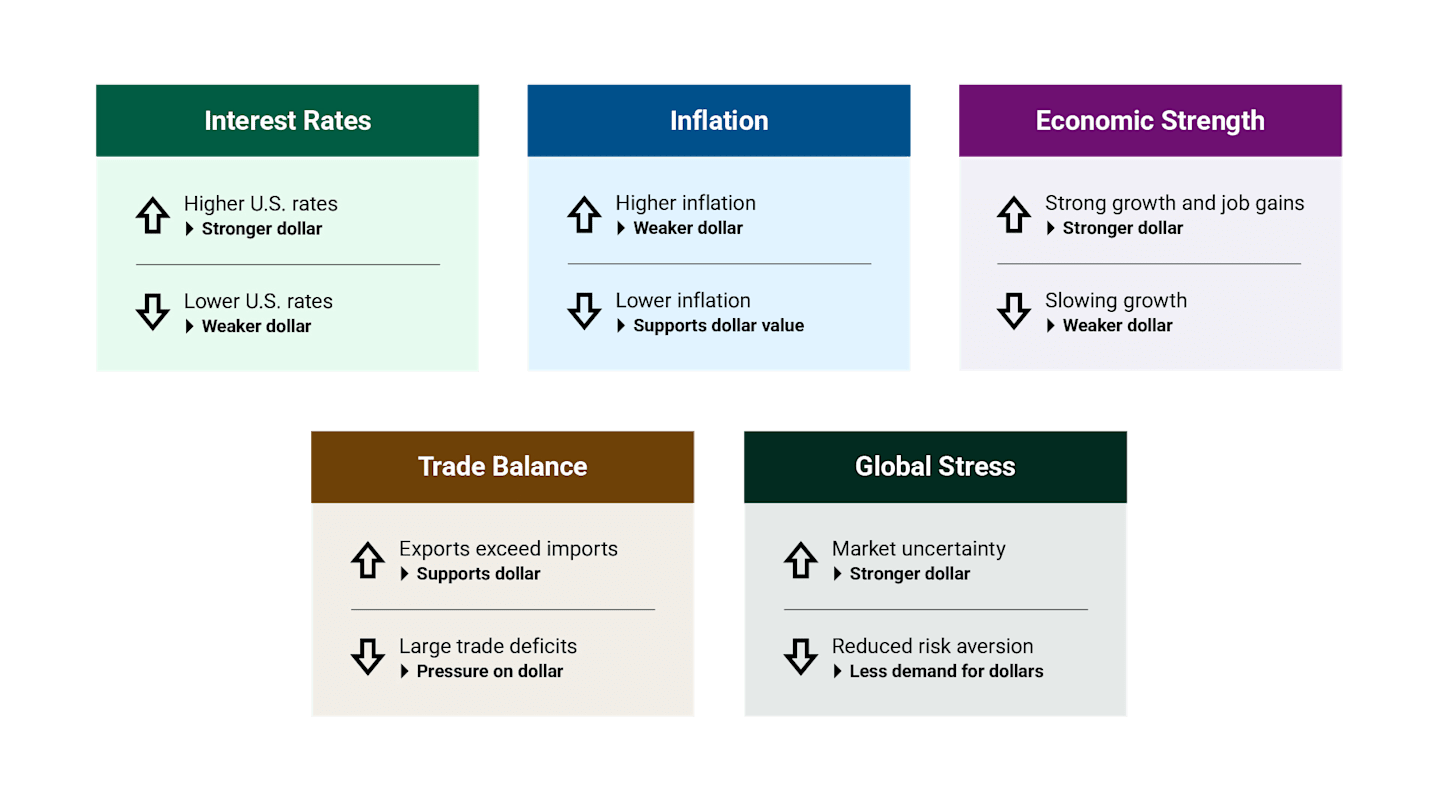

Several factors affect the value of the dollar, as depicted in Figure 2. These elements operate concurrently, often offsetting each other, resulting in minimal movement in the dollar’s value. Occasionally, however, one or more factors prevail, altering the equilibrium and causing significant shifts in the dollar's worth.

Interest rates: When U.S. rates rise, global investors tend to gravitate to dollar-denominated assets, strengthening the dollar. When rates are lower, the opposite happens.

Inflation: Higher inflation erodes purchasing power, weakening the dollar.

Economic strength: Strong growth and jobs boost confidence in the dollar.

Trade balance: Selling more than we buy supports the dollar. However, big trade deficits can hamper the dollar’s value.

Global stress: During times of economic uncertainty, investors often turn to the dollar, which has historically been considered the world’s “safe-haven” currency.

Figure 2 | Why the U.S. Dollar’s Value Changes

How the U.S. Dollar’s Value Affects Your Investments

Let’s break down what happens when a fund you own buys a foreign security. First, the fund exchanges dollars for local currency, which it then uses to purchase the security. After that, two factors shape your fund’s performance:

The local market’s return: Did the asset go up or down in its home currency?

The currency’s movement against the U.S. dollar: When you convert the investment back to U.S. dollars, did the exchange rate help or hurt you?

Both factors play a role in the result. Even if a stock performs well locally, a decline in the local currency versus the dollar can reduce your gains when you bring those profits home. Conversely, a weaker dollar may amplify your returns.

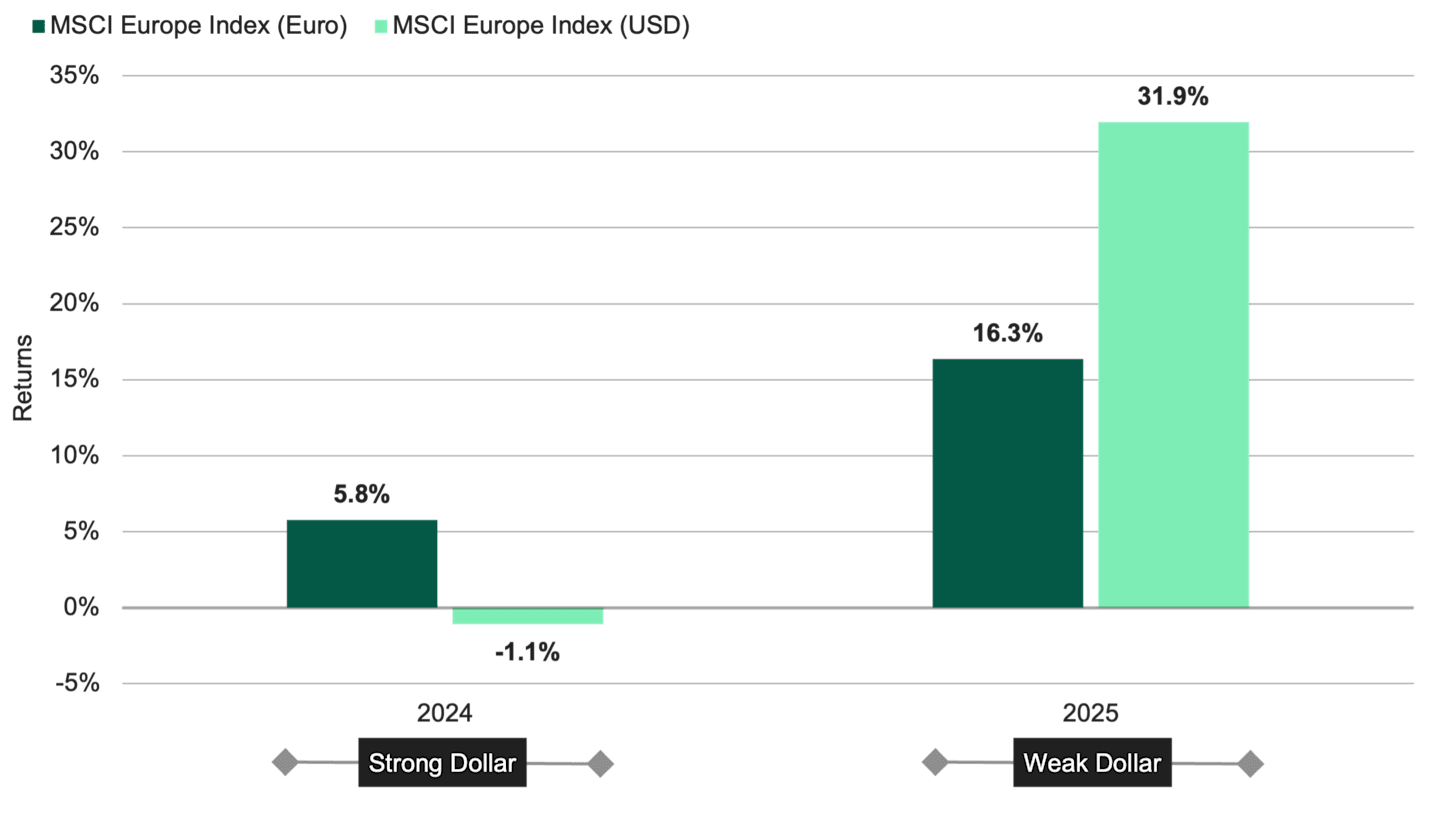

Figure 3 illustrates how the strength of the dollar shaped the recent returns of European equities. In 2024 and 2025, the underlying European stock market produced positive local‑currency returns. But U.S. investors experienced very different outcomes due to changes in the U.S. dollar’s value.

Figure 3 | Currency Can Change the Returns You Earn

Data from 1/1/204 – 12/31/2025. Source: Bloomberg Finance L.P. The MSCI Europe Index tracks the performance of large- and mid-cap stocks across 15 developed market countries in Europe. Past performance is no guarantee of future results.

In 2024, the dollar strengthened versus other currencies. European stocks delivered positive local returns — about 6% in euros — but U.S. investors ended up with a slight loss after converting euros into dollars. The stronger dollar effectively erased the equity gains.

In 2025, the dollar weakened versus other currencies. European stocks rose more than 16% in euros, but after converting euros back into U.S. dollars, the gain nearly doubled to 32%. The weaker dollar acted as a tailwind, boosting returns simply through currency conversion.

Some portfolio managers use hedging strategies to help neutralize the impact of currency movements. However, implementing such strategies, typically with derivatives and forward contracts, incurs a cost.

Many mutual funds don’t hedge foreign exchange risk. In these funds, you can expect currency fluctuations to influence performance.

Making Sense of Dollar Headlines

Currency fluctuations are just one of many factors that affect your buying power. You can’t control currency movements, but you can adjust certain purchases according to the dollar’s value.

You can also discuss with your investment advisor how currency trends and foreign assets influence your portfolio. Together, you can assess whether your portfolio is well-diversified and positioned to withstand fluctuations in currency exchange rates.

Authors

Build Your Investing Knowledge with Our Latest Investment Insights

Read our latest articles and market perspectives.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

Diversification does not assure a profit nor does it protect against loss of principal.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.