How to Prepare for a Recession—For Your Life and Finances

Downturns are a normal part of the economic cycle—though they can feel alarming. Learn the warning signs and how you can be prepared long before one occurs.

Key Takeaways

Recessions are marked by significant economic downturns that can last for a period. They often feel alarming because of how they can affect your life and finances.

Understanding a recession and how long it may last may help ease some of the discomfort associated with these periods.

Likewise, smart financial decisions can help you be more prepared for times of economic uncertainty—and maybe even thrive during them.

Talks of a looming recession can make even the savviest investor uncomfortable. But rather than worrying and wondering if a significant decline in economic activity will happen—chances are it will at some point—the best course of action is to be prepared all the time.

Recessions can profoundly affect lives and finances—but not all in the same way. That’s why knowing how to prepare yourself is key.

To understand what an economic downturn might mean for you, it’s good to start by revisiting what a recession is, how long one typically lasts and how it can affect various parts of the economy. Then, consider some strategies designed to help you survive, and maybe even thrive, during challenging economic times.

What Is a Recession and How Long Does One Last?

According to the National Bureau of Economic Research (NBER), a recession is a period of declining economic activity lasting more than a few months. To qualify as a recession, declines must be spread throughout the economy rather than affecting only an isolated sector, such as housing or manufacturing.

A committee of NBER economists officially determines whether the economy is in a recession. The decision is based on several factors, such as payrolls, unemployment rates, real income, consumer spending and industrial production.

While some recessions may be relatively short-lived, lasting only a few quarters, others can persist for several years.

Shortest recession: The COVID-19 recession, which occurred from February to April 2020, is the briefest downturn on record.

Longest recession: The Great Recession, which lasted a year and a half (from December 2007 to June 2009), is the most prolonged downturn since the Great Depression of the 1930s.

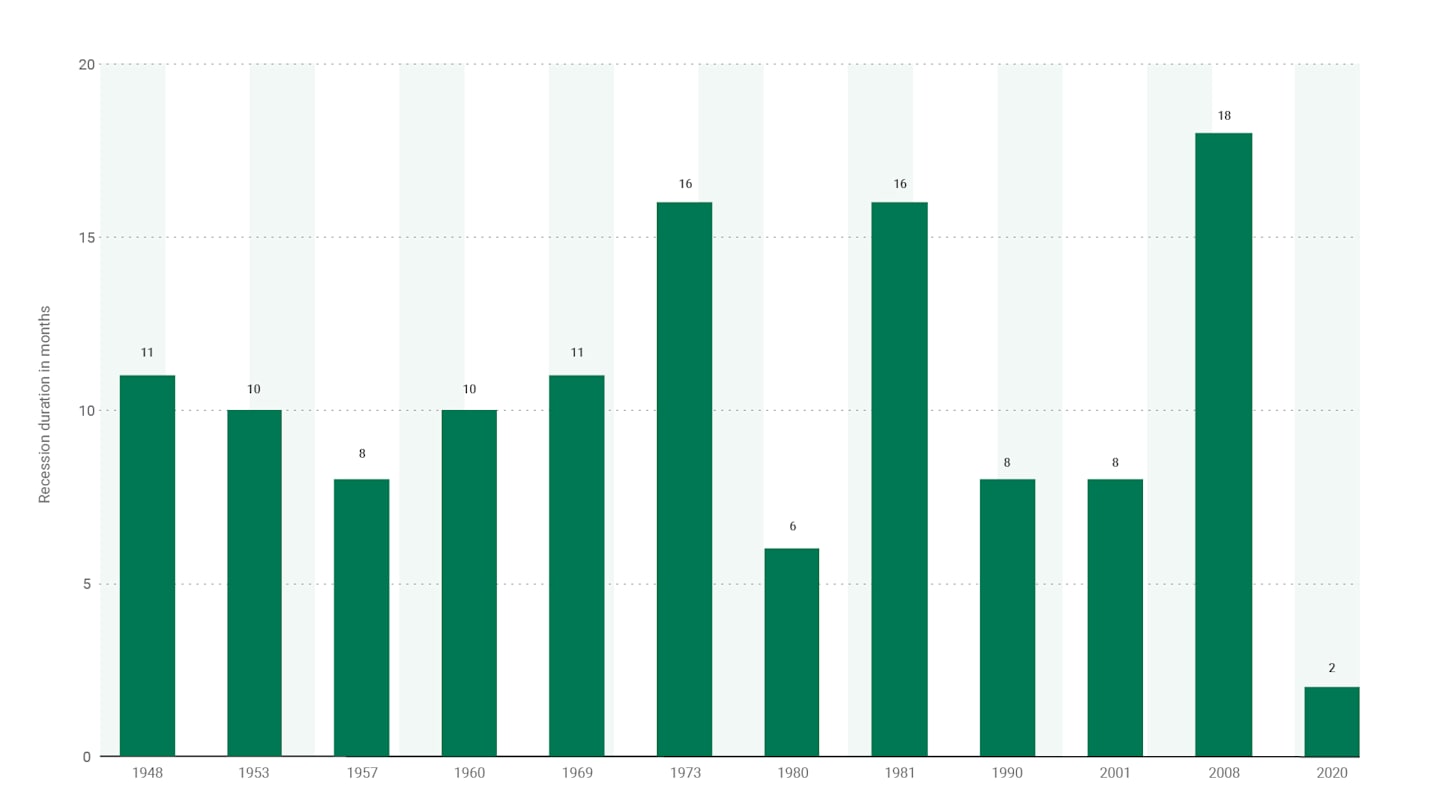

Since 1948, the NBER has recorded 12 recessions, which lasted an average of 10 months. Fortunately, the periods of economic expansion between each recession lasted much longer than the recessions themselves.

12 Recessions in Last 75 Years Lasted 10 Months on Average

Source: St. Louis Fed as of December 2024.

What Are the Causes and Warning Signs of a Recession?

The U.S. economy experiences ups and downs regularly. Economic activity expands until it reaches a peak, then slows and sometimes bottoms out in a recession. This is part of the normal economic cycle.

The factors that result in a recession are more nuanced. It’s always difficult to predict a recession, but several telltale economic indicators may point to downturns in the economy.

- Decline in economic growth. Two consecutive quarters of negative growth in the gross domestic product is generally the NBER’s definition of recession, but it’s not a guarantee.

- Inverted bond yield curve. The yield curve is a graphic representation of bond yields at different maturities, and an inverted yield curve often precedes a recession. An inverted yield curve has longer-maturity bonds with lower yields than shorter-maturity bonds, which indicates that bond investors see the economy slowing.

- Increase in job loss, decrease in personal income. When the economy slows, employers look for ways to save money, which often results in reducing employees’ hours or laying off workers. As a result, income levels decrease and consumer spending declines. Economists consider payroll levels across the economy when determining whether a recession is underway.

- Slowdown in consumer spending. When people are spending less money throughout the economy, either because many of them have lost income or because inflation has driven up the price of goods, that may be another sign of an economic downturn.

What Does a Recession Mean for You?

There’s a long history of recessions in the U.S. Each one is unique and affects people’s lives and finances differently.

Investors: What Does a Recession Mean for Investment Strategies?

Market ups and downs occur daily, but recessions commonly bring deeper market declines. A bear market, which is a decline in value of more than 20% from the market’s previous high over an extended period, is often—but not always—accompanied by a recession.

When investing in bear markets, it’s tempting to sell some holdings rather than continue watching prices fall—but doing so may result in greater losses. Selling when the market is low locks in losses; you no longer have the opportunity for those holdings to rebound. Also, having fewer stocks in your portfolio leaves you with a reduced ability to potentially recoup some losses when the market bounces back.

Over the past 50 years, stock prices have typically fallen during the early part of a recession, but the opposite has occurred during the second half, with stocks showing strong positive returns. Investors with diverse portfolios may be able to weather recessions, and those with money to invest can add to their portfolios at bargain prices.

How Can You Prepare Your Portfolio?

A key to navigating a downturn is to prioritize strategic diversification. Portfolios with different types of investments may fall less during downturns and recover sooner.

Periodic portfolio check-ins to rebalance your portfolio can also help keep you on track. Some investments may perform better than others, and your portfolio can become misaligned, which could expose you to more risk than you expected.

The thought of a recession can be very scary. During those times, working with a financial professional to ensure your portfolio is properly diversified and you have a sound financial plan in place can make all the difference.

Another option to consider is a professionally managed asset allocation portfolio, which offers a mix of funds covering multiple asset categories in a single product. Importantly, fund managers carefully select and monitor the investments in these portfolios.

While everyone will experience the same economy, not everyone has the same tolerance for risk or timeline. But in times of uncertainty, avoid knee-jerk reactions to the market. Spur-of-the-moment decisions for an existing plan are rarely the best way to reach your goals and objectives, and that’s true, especially in volatile times.

Workers and Business Owners: What Does a Recession Mean for Jobs?

During a recession, unemployment typically rises as some employers try to cut payroll costs to stay afloat. Some industries are more susceptible to cuts than others. Industries that are typically at risk include construction, personal services and tourism because consumers have less discretionary spending available.

While some businesses struggle during a recession, others may thrive. For example, grocery stores and food manufacturers often stay busy, as consumers dine out less to save money. Similarly, cheaper entertainment providers, such as streaming services, may boost revenue. And because people are more likely to repair old cars than buy new ones during a recession, car maintenance shops may also maintain a brisk business.

Homebuyers and Sellers: What Does a Recession Mean for Housing and Mortgages?

During a recession, people usually spend less money than normal because they’ve lost income, or they’re worried about their finances. As a result, demand for homes decreases, construction of new homes slows and home prices often drop—although that can depend on location.

In addition to lower home prices, mortgage interest rates might decrease during a recession as fewer people borrow to buy homes. Even when interest rates are lower, a recession is a time of economic uncertainty and, for many people, job loss or instability. This may prevent them from taking the plunge on purchasing a new home. Whether it’s a good time to buy a home depends on a person’s individual financial situation.

Borrowers: What Does a Recession Mean for Other Loans?

During a recession, banks and other lenders usually become more cautious about risk and tighten their lending standards. At that point, fewer people qualify for loans and credit, so interest rates gradually drop.

People who qualify for new credit during a recession may be able to secure it at a lower rate. However, economic uncertainty and the ongoing risk of layoffs make a recession an uncertain time to borrow money.

How to Survive (and Maybe Even Thrive) During a Recession

Being prepared can help you be ready for when a recession hits. Start by taking some smart financial steps, such as:

Build your emergency fund, aiming for enough to cover at least three months’ worth of expenses.

Cut back on spending as much as possible.

Pay down high-interest debt as quickly as you can.

Seek out additional income streams, such as a side job or part-time gig.

When you’re living through an economic slowdown, you can continue to make smart financial choices to help you ride out the challenges and land on firm footing on the other side. Some of the best financial choices to make during a recession include:

Prepare your resume and nurture your network. Despite your best efforts, layoffs during a recession happen—so it’s a good idea to revamp your resume and have it ready.

Make sure your professional online profiles are up to date. Use them to interact with your network on a regular basis and focus on helping others in your network by making introductions and offering helpful advice. If you need to find another job, your network will be primed and ready to help.

Revise your budget and stick to it. Sticking to a budget is important for managing money wisely at any time, but it’s crucial during a recession. That includes prioritizing your spending by evaluating essential and discretionary expenses.

Even if you have a budget, take time to revisit it and look for areas to cut back. Budgeting during a recession is a little different because you may have less money to cover your needs, or you may need to focus on setting aside more savings in case of a potential layoff.Take advantage of financial assistance if needed. If you’re short on cash and your mortgage lender or student loan provider is willing to pause payments, take advantage of the temporary reprieve.

Also, some credit card companies or lenders may be willing to adjust their terms to make it easier for you to stay on track with your payments. If you need help, don’t be afraid to contact your creditors to ask.

If you’re unsure about your financial footing or feel unprepared if a downturn should occur, consider talking to a financial professional who can help you navigate the uncertainty. Here we offer personal consultations with a Certified Financial Planner® or ongoing, in-depth advice and planning if you’re looking for something longer-term with an advisor.

Whichever way you choose, being prepared and having a plan in place can help you feel more confident about your finances no matter what the economy does.

Authors

Financial Consultant

Is Your Portfolio Prepared for All Economic Conditions?

Talk to an advisor to help make sure you’re prepared. Choose your option.

Rebalancing allows you to keep your asset allocation in line with your goals. It does not guarantee investment returns and does not eliminate risk.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

Diversification does not assure a profit nor does it protect against loss of principal.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

American Century's advisory services are provided by American Century Investments Private Client Group, Inc., a registered investment advisor. These advisory services provide discretionary investment management for a fee. The amount of the fee and how it is charged depend on the advisory service you select. American Century’s financial consultants do not receive a portion or a range of the advisory fee paid. Contact us to learn more about the different advisory services. All investing involves the risk of losing money.