Energy Prepays: Powering Yields, Variety in Muni Portfolios

Specialized bonds can offer non-traditional muni-sector exposure without sacrificing the muni market’s hallmark tax-exempt income.

Key Takeaways

Issuance of energy prepayment bonds (energy prepays), once a niche sector in the municipal bond market, has recently increased significantly.

A wider gap between muni bond and U.S. Treasury yields, along with increased energy demand, has led to record trading volume.

These bonds allow municipalities to lock in discounted energy purchases while delivering potentially higher yields than similarly rated munis.

The municipal bond (muni) market has seen a significant uptick in the issuance of energy prepayment bonds. These previously overlooked tax-exempt securities allow public utilities to pay for future energy supply in advance.

In addition to delivering cost savings to municipal utilities, energy prepay bonds feature tax-exempt income, similar to traditional municipal bonds.

As artificial intelligence (AI) expands and data centers proliferate, energy demand is rising rapidly. We believe this backdrop is likely to encourage more municipalities to lock in long-term supply and discounted prices through the energy prepay bond structure.

What Are Energy Prepayment Bonds?

Energy prepayment bonds are structured financial instruments with two main objectives:

They enable energy purchasers, such as public utilities, to lock in discounted prices for natural gas or electricity, usually for several decades.

They provide a mechanism for “funding recipients” (traditionally large banks or life insurance companies) to borrow at tax-exempt rates and invest the proceeds at taxable rates. The funding recipient earns the spread between the two rates. As a result, these deals tend to be more economical when the yield ratios between muni bonds and U.S. Treasuries are low.

The funding recipient makes fixed monthly payments to the energy supplier that cover the energy purchases. Additionally, the funding recipient will bear the ultimate responsibility for paying bondholders if the energy agreement ends before its maturity. Therefore, the bond's credit rating is typically derived from the funding recipient.

What Are the Key Features of Energy Prepay Bonds?

To cut energy costs and secure long-term commodity supply, municipal entities issue tax-exempt bonds to fund the prepayment contract. Like other municipal bonds, tax-free income is a key feature of energy prepay securities.

Other features of energy prepays include:

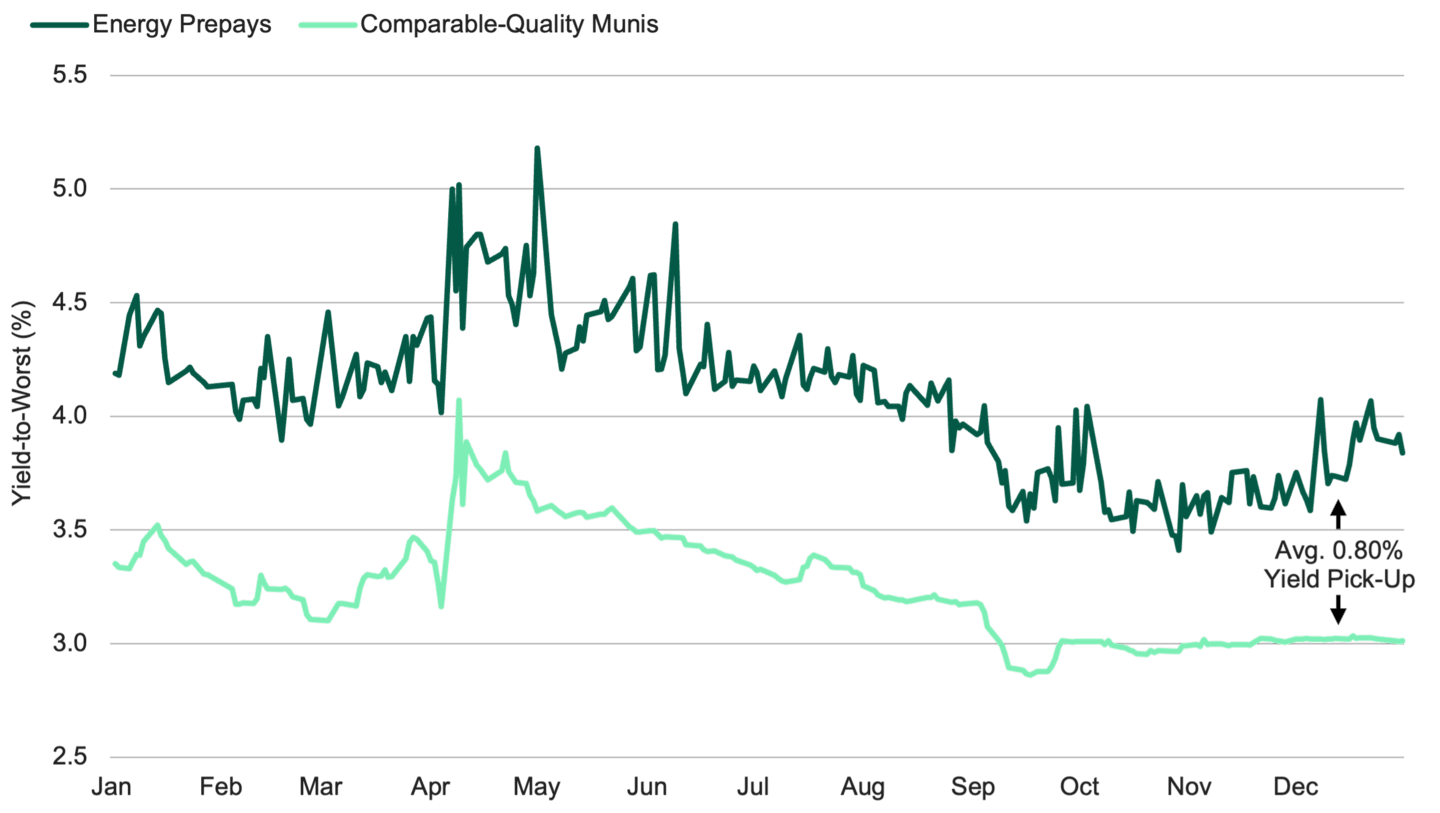

Higher yields than traditional munis: Because their structures are complex, energy prepay bonds have historically offered investors higher tax-free yields than comparable-quality municipal bonds. See Figure 1.

Investment-grade securities: Although municipal entities issue the bonds, they don’t drive the securities’ credit ratings. Instead, credit exposure most often aligns with funding recipients, which are typically large banks or life insurance companies with investment-grade credit ratings.

Repayment safeguards: These bonds include layers of risk-mitigation features designed to ensure energy flow, bondholder payments and liquidity. Throughout the sector’s history, only one funding recipient defaulted — Lehman Brothers during the 2008 global financial crisis.

Figure 1 | Energy Prepay Yields Have Historically Surpassed Comparable-Quality Muni Yields

Data from 1/1/2025 – 12/31/2025. Source: Bloomberg, Goldman Sachs. Past performance is no guarantee of future results.

We used the Black Belt Energy Series 2024B (a bellwether gas prepay bond with Goldman Sachs as the funding recipient with a 5% coupon and a 2032 maturity) as an example to represent Energy Prepays, as there is no index for these securities. Comparable-Quality Munis represented by the Bloomberg 5-10 Year Municipal Bond Index (a rules-based, market-value weighted index engineered for the long-term tax-exempt bond market. This index is the 5-10 year component of the Municipal Bond Index). Yield-to-Worst is the minimum yield an investor can receive if the issuer uses provisions like prepayments, calls or sinking funds.

Why Has Energy Prepay Issuance Increased in Recent Years?

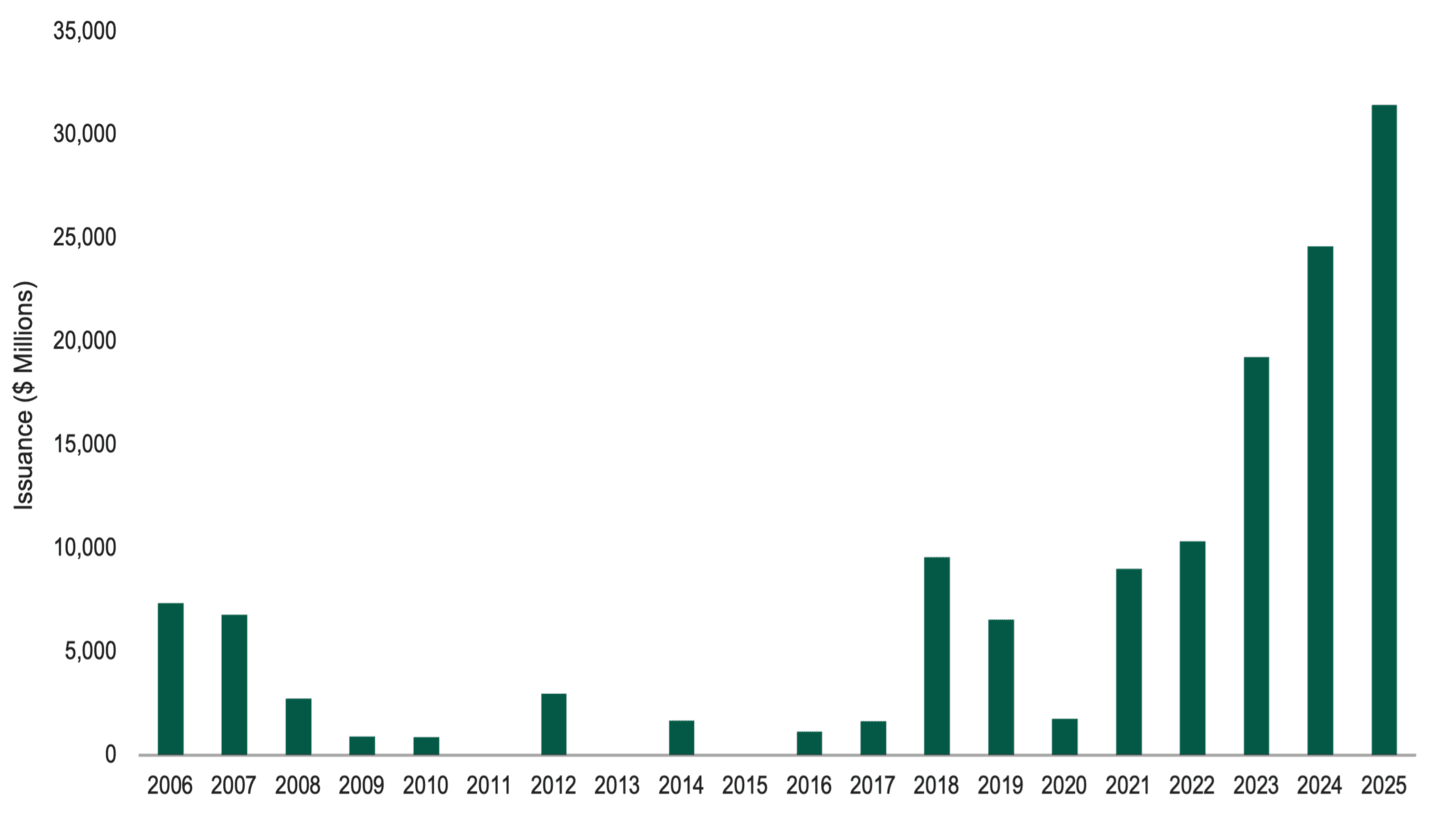

First issued in the 1990s, energy prepay bonds gained traction in 2005, when Congress passed legislation clarifying the tax-exempt structure of the securities. Issuance and demand for energy prepay bonds fluctuated over the next several years, as shown in Figure 2.

Following the COVID-19 pandemic, the yield spread between munis and Treasuries widened, resulting in a favorable environment for energy prepay issuance. In 2022, issuance reached $10 billion, matching the record set in 2018.

Record-setting issuance continued, with $19 billion in 2023, $25 billion in 2024 and more than $31 billion in 2025. The pace hasn’t slowed in 2026, with more than $4 billion in year-to-date issuance through mid-February.

This once-niche sector now represents 5% of the total muni market and more than 25% of Bloomberg’s California Intermediate Municipal Bond Index.1

Figure 2 | Energy Prepay Issuance on the Upswing

Data from 1/1/2006 – 12/31/2025. Source: Bloomberg.

How Do Energy Prepay Bonds Compare with Traditional Munis?

In traditional muni transactions, investors lend money to a governmental entity that finances a public project and uses its taxing power to repay investors. If the project is revenue-generating (such as a toll road or hospital), the issuer uses the money it collects from the project’s operation to repay investors. In both scenarios, investors earn tax-exempt interest.

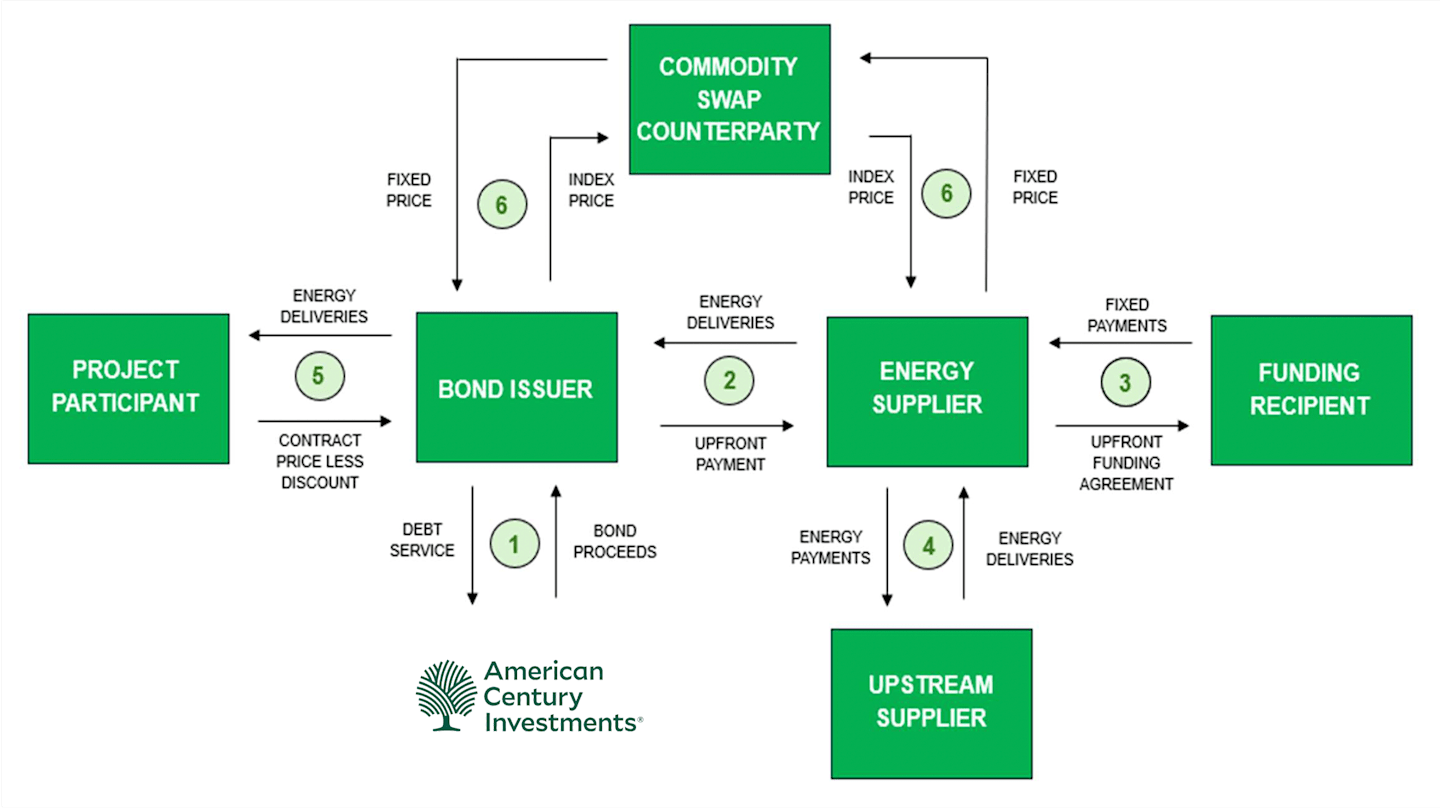

Energy prepay bonds are more complex transactions that rely on multiple participants, as Figure 3 illustrates.

Figure 3 | How Energy Prepay Bonds Work

Source: American Century Investments.

The transaction’s components include:

Bonds: Investors lend the upfront capital to a public energy authority through tax-exempt municipal bonds. These deals tend to be large, ranging from $500 million to more than $1 billion.

Prepaid contract: The authority uses bond proceeds to prepay an energy supplier for future deliveries of natural gas or electricity, usually more than 30 years.

Funding agreement: The energy supplier transfers the bond proceeds to the funding recipient (typically a large bank or insurance company). The funding recipient invests the proceeds from the tax-exempt bonds at taxable rates, making its profit on the difference (spread) between the two yields. The funding recipient makes fixed payments back to the supplier, who uses this money to procure energy over time at a discounted price. Commodity swaps (see below) lock in the discounted price.

Energy supply agreement: The energy supplier buys the electricity or natural gas from an upstream supplier, typically a commodity arm of a large bank.

Energy delivery agreement: The municipal utility receives the energy from the supplier at the discounted price. Customers pay the municipal utility for their energy, and the utility pays the issuer, which is responsible for making timely repayments to bondholders.

Commodity swaps: These critical components of energy prepay transactions ensure the utility receives a fixed discount regardless of price swings in electricity or natural gas.

What Risks Are Associated with Energy Prepay Bonds?

While the structure of energy prepay bonds may offer some precautions, these securities still carry risks, including:

Funding recipient risk: The credit risk of the funding recipient is key, as the funding recipient makes the fixed payments that allow for the procurement of energy. Also, if the energy supply agreement terminates prematurely, the funding recipient will accelerate its loan, providing sufficient funds to redeem the bonds.

Project participant risk: The municipal utility’s payment for energy is essential for the structure to work. However, the energy supplier or funding recipient will typically absorb a default by the utility.

Energy market shifts: Movement away from fossil fuels into renewable energy may reduce the demand by project participants and require the gas supplier to remarket unused energy. Any selling of energy to non-municipal participants could trigger a taxable event.

Tax law changes: While unlikely, there’s always a chance that Congress may change the tax laws surrounding energy prepay securities or even the broader municipal market. Such changes could affect the tax-exempt status of the securities.

Through research and experience in the sector, we seek to mitigate and manage risk in pursuit of attractive performance. Our municipal bond analysts and portfolio managers focus on high-credit-quality issuers and sound security structures.

Given their non-traditional nature, we believe energy prepay bonds have the potential to enhance yield, diversification and overall performance in municipal bond portfolios.

Authors

Senior Municipal Credit Analyst

Municipal Bonds in Focus

Get market updates, behavioral insights and investment ideas.

Source: Bloomberg. Bloomberg California Intermediate Municipal Bond Index is an unmanaged, tax-exempt benchmark that tracks investment-grade, fixed-rate California municipal bonds with maturities typically between 5- and 10-years. It represents a broad selection of California general obligation (GO) and revenue bonds, often used to measure the performance of intermediate-term CA municipal bond funds.

Past performance is no guarantee of future results. Investment returns will fluctuate and it is possible to lose money.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

Generally, as interest rates rise, the value of the bonds held in the fund will decline. The opposite is true when interest rates decline.

Diversification does not assure a profit nor does it protect against loss of principal.

IRS Circular 230 Disclosure: American Century Companies, Inc. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated with American Century Companies, Inc. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

This information is for educational purposes only and is not intended as tax advice. Please consult your tax advisor for more detailed information or for advice regarding your individual situation.