How Are Investments Taxed? A Guide for Investors

Owning or cashing out an asset can trigger more investment taxes than you might expect. But with the right strategy, you may be able to lower them.

Making a profit from an investment can be exciting—until the tax bill comes due.

Depending on the length of ownership and type of asset, taxes on investments can take a significant amount of money out of your pocket. Understanding how (and when) your investments are taxed is an essential part of your financial plan.

How Much Will I Pay in Taxes? Taxable vs. Tax-Deferred vs. Tax-Exempt Accounts

Different account types have unique tax obligations that may impact the tax outcome.

- Tax timing: Annually. Earnings, dividends and capital gains in taxable accounts are subject to tax annually in the year paid.

- Examples: Individual or joint investment accounts, checking and savings accounts

- Tax timing: Later. Earnings and contributions grow tax-deferred until you withdraw those earnings at a later date.

- Examples: Traditional IRAs, retirement plans such as 401(k), 403(b), defined.

- Tax timing: None. Qualified withdrawals from these accounts (also called tax-free accounts) are not subject to income tax.

- Examples: Roth IRAs and Roth 401(k) plans

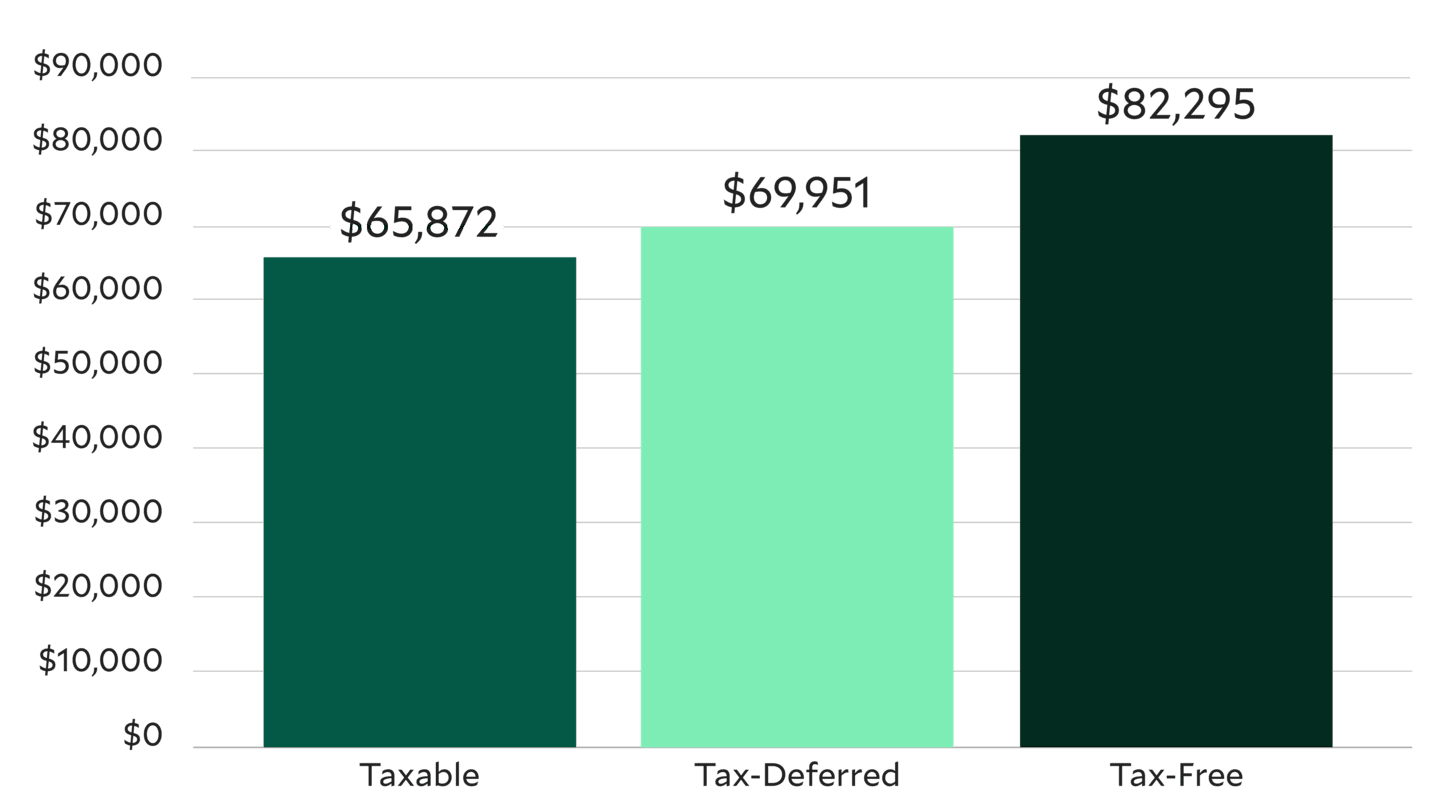

What could that look like for your own investments? In this hypothetical example, you can see the tax treatment of a $10,000 investment after 20 years.

Tax Treatment of $10,000 Investment

Source: Taxable vs. Tax-Deferred vs. Tax-Free Calculator, American Century Investments, June 2026. These hypothetical calculations contain assumptions that are intended for illustrative purposes only and are not representative of the performance of any security. There is no assurance similar results can be achieved, and this information should not be relied upon as a specific recommendation to buy or sell securities. The calculations assume a $10,000 initial investment and monthly investments of $100 over 20 years with a 6% return rate. Assumes reinvestment of all gains, dividends and interest, and does not include fees or expenses. Tax assumptions: 25% tax during contributions, 15% tax during withdrawal, no tax deductions.

Use our tax calculator to help optimize your tax benefits and growth potential.

What Are the Common Types of Investment Taxes?

Tax-exempt and tax-deferred retirement accounts may help investors cut down on taxes, but they do come with annual contribution limits.

Those who want to invest beyond tax-exempt and tax-deferred vehicles should be mindful of the taxes associated with their investments. Because no matter how great a gain you make on an investment, taxes can significantly cut down on your bottom line.

Dividend Taxes

Dividends are the payment of a company's earnings to stockholders as a distribution of profits. You pay taxes on dividends in the year paid, even if the dividends are reinvested. The amount of tax owed on dividends will depend on whether they're qualified or nonqualified.

Nonqualified dividends are taxed at the same rate as the taxpayer’s income bracket. Nonqualified dividends include payouts from real estate investment trusts (REITs) as well as unexercised employee stock options.

Qualified dividends are taxed at the long-term capital gains rates, which tend to be lower than the marginal ordinary income brackets.

A dividend is qualified if:

It’s paid out by a qualifying U.S. company or similar foreign business.

Most publicly traded stocks, equity-based exchange-traded funds (ETFs) and mutual funds will fall into this category.

The security has been owned for a certain period.

Taxpayers must own the security for at least 60 days during the 121-day period that starts 60 days before the ex-dividend date (you must own the stock at least a day before the ex-dividend date to receive the dividend).

If dividends are paid and reinvested within a tax-deferred vehicle like an IRA or qualified retirement plan, the tax is deferred.

Capital Gains Taxes

When you sell a capital asset, the profits from the sale may be subject to capital gains tax (unless held in a tax-deferred vehicle). Taxes will not be owed on the investment until it is sold, only when it becomes realized capital gains. Taxes are only applied to the appreciation from the investment, not the initial investment. The tax rate for capital gains varies based on the asset holding period and your income. The short-term capital gains tax will apply if you hold on to an asset for one year or less. In that case, your short-term capital gains rate equals your income tax rate.

But if you hold on to the asset for more than a year, you’ll pay the lower long-term capital gains tax on the profits from the sale. Then you'll owe long-term capital gains tax at a rate of 0%, 15% or 20%, depending on your overall annual income.

Holding on to an asset for more than a year will benefit most taxpayers, as the gains are taxed at a generally lower rate than their ordinary income.

Qualified dividends are taxed at 0%, 15% or 20%, depending on the taxpayer’s income bracket. Investing in an asset that’s a qualified dividend can mean paying taxes at a lower rate.

Capital Gains for Mutual Fund Investments

Mutual funds held in taxable accounts are subject to taxes on capital gains distributions and dividends. That means investors may owe capital gains taxes during the time they own a fund’s shares, as well as when they sell those shares at a profit. Holding on to a mutual fund for more than a year may mean paying the long-term capital gains rate. Similarly, if a mutual fund pays out dividends, choosing to invest in a fund that pays out qualified dividends could impact the tax rate.

Where an investor keeps their mutual funds can also impact taxes. Holding them in a retirement account can help defer taxes associated with interest and dividends and capital gains distributions. This concept is commonly referred to as asset location.

Income Taxes

A final consideration is your income tax rate. U.S. income and capital gains tax rates are progressive, meaning the higher the income, the higher the marginal ordinary income and capital gains rates.

When redeeming from a tax-deferred investment vehicle such as a traditional IRA or 401(k), whatever is redeemed will be taxable as ordinary income. That means any tax-deferred contributions, as well as any potential earnings or growth, will be taxable at the federal income tax rate.

Understanding the federal income tax rate can give you an idea of how much you may owe if an asset sale pushes you into a higher bracket. You can work with your financial advisor and tax advisor to prepare a year-round tax plan to help decrease your tax liability and keep more of your investment returns.

Selling an asset for a profit is exciting, but taxes owed may dampen the celebration, eating into your bottom line. Understanding how to reduce them can mean keeping more money for you.

What Is Tax-Efficient Investing?

Tax-efficient investing aims to put more money in your pocket by reducing capital gains and income taxes. Efficient investments include retirement accounts but also encompass:

ETFs. Overall, ETFs have built-in tax advantages, making them appealing investment options for retirement, among other goals.

Bonds. Investing in municipal or Treasury bonds may be advantageous, as interest income isn’t always taxed at the federal level for Treasury bonds, and interest on municipal bonds may not be subject to state or local tax.

Health savings accounts (HSAs). These accounts can be a great way to save for health care expenses in retirement.

Tax-loss harvesting is a tax-efficient strategy that can help offset capital gains with capital losses. That means if an investor reports capital losses from one investment, they could potentially offset gains from a different investment. Tax-loss harvesting can get complicated, so it may be worth working with a financial advisor to learn more.

For those in or nearing retirement, when investment income is a priority, incorporating tax-efficient vehicles can mean owing less in taxes, which can mean more money to meet expenses and invest for your future.

Authors

Financial Consultant

Seek to Keep More of What You Earn

Get more information about how tax rules affect your investments.

IRS Circular 230 Disclosure: American Century Companies, Inc. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated with American Century Companies, Inc. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

This information is for educational purposes only and is not intended as tax advice. Please consult your tax advisor for more detailed information or for advice regarding your individual situation.

Please consult your tax advisor for more detailed information regarding the Roth IRA or for advice regarding your individual situation.

Taxes are deferred until withdrawal if the requirements are met. A 10% penalty may be imposed for withdrawal prior to reaching age 59½.

IRA investment earnings are not taxed. Depending on the type of IRA and certain other factors, these earnings, as well as the original contributions, may be taxed at your ordinary income tax rate upon withdrawal. A 10% penalty may be imposed for early withdrawal before age 59½.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.