Nuclear Power: Balancing Energy Security and Sustainable Development

Key Takeaways

Demand for reliable (24/7), secure electricity is increasing worldwide. Nuclear energy can be a sustainable way to meet this need.

While nuclear power has its challenges, it also has advantages compared with other sources, including fossil fuels and renewables.

The nuclear energy value chain includes operators, developers and “picks-and-shovels” suppliers that may be affected by the industry’s growth.

Energy use and economic growth have risen at roughly the same rate since the Industrial Revolution. That relationship may now be changing.

In 2024, global electricity demand outpaced gross domestic product (GDP) growth for the first time in 30 years (aside from crisis related disruptions). This trend is expected to continue, with electricity use projected to grow at least 2.5 times as fast as overall energy demand through 2030.1

Three key megatrends are driving rising demand for electric power:

Artificial intelligence (AI). The data centers popping up around the globe need electricity to power energy-intensive AI chips and to stay cool, as these chips generate significant heat. While forecasts vary, demand for electricity from data centers is expected to more than double by 2030, reaching levels equal to Japan’s total power use in 2024.2

Electrification. Countries, companies and consumers seek to reduce carbon emissions and fuel costs. This is boosting electrification in transportation (cars, trucks, ships, trains, and even airplanes), industrial processes, heating, and more. Heat pump sales for heating and cooling homes are expected to double from 2025 to 2030.3

Emerging market (EM) economies. Per capita GDP is rising in many EM countries. Therefore, they need more electricity to meet the growing demand for modern conveniences such as household appliances and, especially in the global South, air conditioning. Emerging markets will account for nearly 80% of additional electricity consumption through 2030, according to the International Energy Agency (IEA). Over the next five years, China alone is expected to add demand equal to the EU’s total electricity consumption.

We advocate a pragmatic approach to meeting electricity needs. While traditional energy sources — along with solar, wind and potentially geothermal — will meet much of the demand, we believe nuclear power, with its ability to supply dependable, carbon-free electricity around the clock, will be an increasingly important part of the solution.4

What Makes Nuclear Energy a Secure Source of Power?

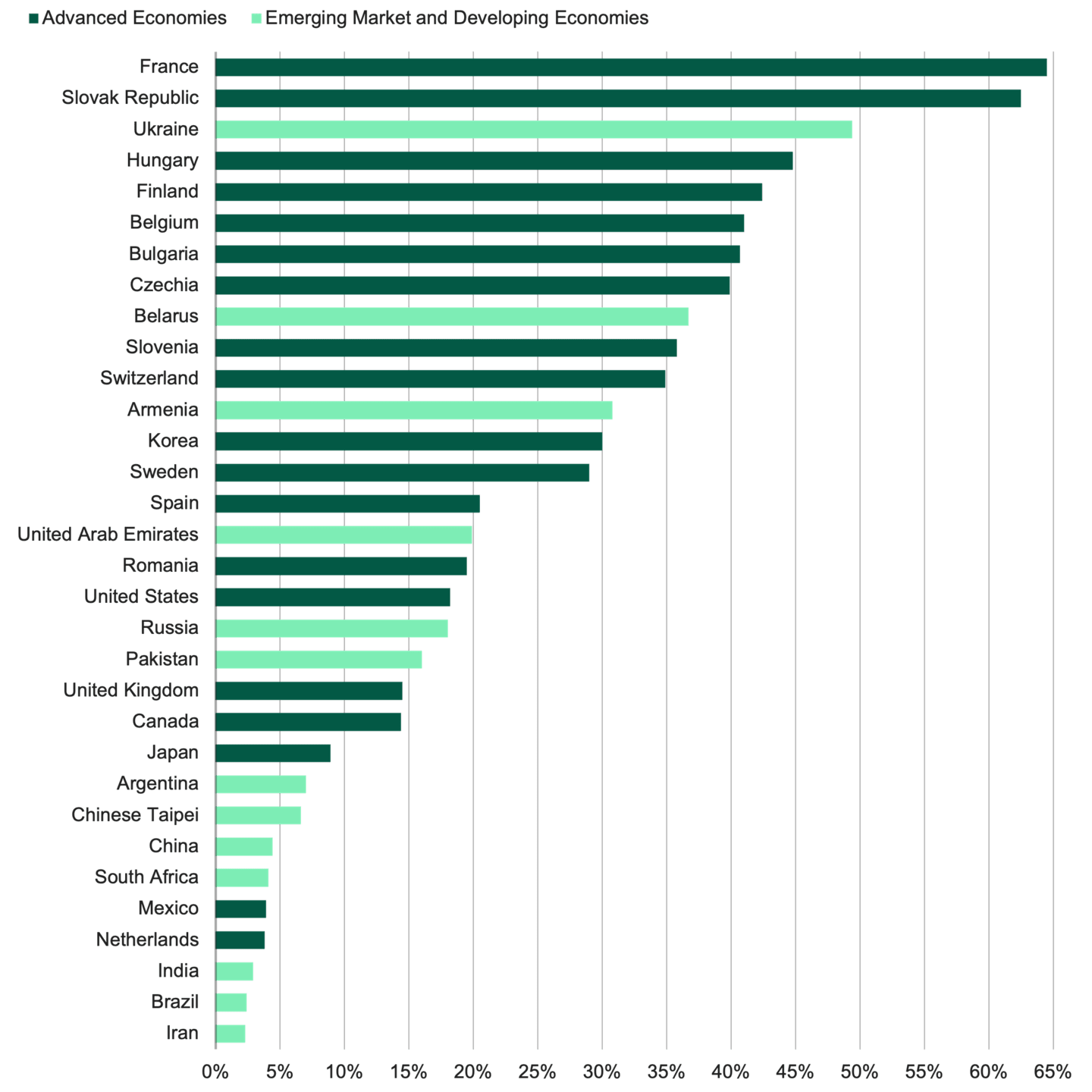

Nuclear power plays a complex role in sustainability debates. While technically non-renewable, it’s among the lowest carbon sources of electricity. It is available continuously on demand year-round, thereby qualifying as firm power throughout its life cycle. Figure 1 shows that nuclear energy supplies a meaningful percentage of electricity in many countries, across advanced and emerging markets.

Figure 1 | Which Countries Rely Most on Nuclear Power?

Data as of 12/31/2023. Source: IEA.

We emphasize that viewing nuclear power as “sustainable” rests not only on its ability to generate electricity without carbon emissions but also on its reliability, security, affordability, and resilience to climate-related and geopolitical disruptions.

This is a tall order. Increasingly extreme weather is likely to continue to cause damage to the infrastructure needed to extract and transport fossil fuels. Russia’s invasion of Ukraine and the blockade in the Strait of Hormuz are recent reminders of how geopolitics can affect supplies.

In our view, nuclear power offers four key advantages:

24/7 availability. The forces driving the growing demand for electricity — data centers, electrification and the expanding middle class in EM countries — expect round-the-clock reliability. Nuclear plants operate day and night, rain or shine. And because spent fuel rods are typically replaced only every 18–24 months, nuclear plants are viewed as a reliable power supply.

Small physical footprint, high energy density. Nuclear fuel is extremely energy-dense. This means nuclear reactors can generate large amounts of electricity from relatively compact facilities that can often be located near existing transmission lines. Small modular reactors (SMRs), while not yet commercially proven, are expected to further enhance this advantage by providing incremental capacity, potentially on-site at industrial facilities, thereby eliminating the need to build new transmission lines.

Very low life-cycle emissions. Emissions from nuclear power generation are effectively zero. Importantly, a nuclear plant’s carbon footprint across its life cycle, including uranium mining and enrichment, plant construction, storing spent fuel rods, and decommissioning, is in the same low-emissions range as wind and materially below natural gas and coal.5 This matters because regulators and investors increasingly consider a power source’s full carbon footprint, including its supply chain, when deciding whether it qualifies as low-carbon.

Waning public resistance. Nuclear power is increasingly viewed not only as a way to reduce carbon emissions but also as a means of improving energy security. In March 2026, European Commission President Ursula von der Leyen described Europe’s earlier turn away from nuclear power as a “strategic mistake,” emphasizing its value as a reliable, affordable, low-emissions source of electricity.6 Japan has shifted from reducing dependence on nuclear power after the Fukushima accident to a goal of maximizing nuclear output alongside a large renewables build-out.

Concerns about energy security are part of the reason for this change in attitude.7 In January 2022, the U.S. Nuclear Regulatory Commission (NRC) denied an application to build and operate a new advanced nuclear reactor due to insufficient data. A month later, Russia invaded Ukraine, causing major disruptions in global energy markets and highlighting the need for reliable electric power that doesn’t rely on fuel from potentially hostile countries.

Two years later, the U.S. Department of Energy and the Nuclear Regulatory Commission granted the necessary approvals to the same company whose application had been denied in 2022. Separately, in April 2026, two other companies began construction on new nuclear reactors in the U.S.8 Both are expected to be online by the end of the decade.

How Do Alternatives to Nuclear Power Stack Up?

To understand nuclear power’s role in the energy mix, it helps to compare its benefits and drawbacks with those of fossil fuels, solar and wind.

Fossil Fuels: Firm Power, but with Economic, Geopolitical and Sustainability Concerns

Natural gas and coal-fired plants provide firm power and historically offered the least costly way to meet fluctuating electricity demand. In recent years, this cost advantage has disappeared.

When fossil fuel prices surge, profits for power generators often suffer. Costs passed on to consumers can spark backlash when electricity bills spike.

The infrastructure needed to extract, transport and store fossil fuels is costly to build and maintain and has a large, often disruptive footprint.

Extreme weather and geopolitics can disrupt supplies, with economically painful consequences. Even in countries with ample oil and gas reserves, fuel prices are susceptible to global supply and demand fluctuations.

In addition to its environmental concerns, burning fossil fuels is also a human health issue. Millions of deaths each year are attributed to air pollution. Insurance costs for the industry increasingly reflect the impacts of climate change and pollution.

Fossil fuels are likely to remain part of the energy mix for decades. However, companies in the energy sector may face more variable returns and additional regulatory challenges as economic, social and geopolitical conditions change. These factors provide useful context when comparing fossil fuels with nuclear power.

Solar: Low Cost and Fast to Deploy, but Intermittent and Land-Intensive

Solar power is unlimited, capacity (large and small scale) can be added quickly, and on-site solar panels can reduce the need for new transmission lines.

Operational emissions are zero, and the cost per kilowatt hour is now below fossil fuel-based electricity.

However, intermittency is a critical limitation. Solar arrays generate electricity only when the sun shines, so the total cost of utility-grade solar must include battery storage (and the related environmental impact of these batteries).

Solar farms require significant land, and it can take years to obtain permits to build transmission lines that connect solar farms to the grid.

Wind: Clean Power with Development and End-of-Life Challenges

Onshore wind power is cost-competitive and can be quick to build in the right permitting environment, but like solar, wind power is intermittent.

Offshore wind can provide stronger, more consistent power and be sited at optimal points along the coastline to connect to the grid. Still, it often involves multi-year development and lengthy interconnection timelines.

Some consider wind turbines unsightly, which can lead to conflicts within communities despite the low-cost power they offer and the rental income generated for private land use.

Wind turbine blades present end-of-life issues. The blades are massive and difficult to recycle, and many communities object to having chopped-up blade pieces dumped in local landfills.

There is no problem-free way to meet electricity demand. Solar and wind power are essential to the energy transition, but they have limitations. Nuclear power can be a firm, flexible, carbon-free complement to other sources.

Diversity in energy sources can improve energy security. In March and April 2026, restaurants and hotels in India were temporarily closed due to a shortage of cooking gas (LPG) caused by the shipping blockade in the Strait of Hormuz. The Indian government prioritized providing LPG to households over commercial users, making it easy to see restrictions extending to residential heating and industrial activities.9 Electrification powered by nuclear and renewable energy could reduce these risks and meet the growing global demand for secure power.

What Are the Risks of Nuclear Power Plant Accidents?

Concerns about nuclear reactor accidents are understandable. Since the nuclear power industry began, three major accidents have shaped public perception of its risks.

Three Mile Island (1979)

This accident in Pennsylvania involved a limited release of radioactive material, with no immediate injuries or deaths.

Exposure for residents was equivalent to the radiation from a chest X-ray. Today, roughly 10,000 people live within three miles of Three Mile Island (TMI); close to 200,000 live within a 10-mile radius of the site.

Constellation Energy plans to restart an adjacent unit at TMI. The facility, now known as the Crane Clean Energy Center, is intended to meet Microsoft's power needs for its data centers.

Chernobyl (1986)

A significant amount of radioactive material was released, causing immediate injuries and 28 deaths, and later leading to many cases of thyroid cancer due to radiation exposure.

The “Chernobyl Exclusion Zone” has been deemed uninhabitable for humans for the next 20,000 years.

This accident in Ukraine was caused by a flawed reactor design, a dangerous test conducted without adequate safeguards, and a culture fearful of admitting mistakes. This is not a common problem that could affect other nuclear power plants.

Fukushima (2011)

The Fukushima Daiichi nuclear reactor meltdown in Japan was triggered by an earthquake and tsunami that overwhelmed safety measures and disabled backup systems.

Loss of life was caused by the natural disasters, not by radiation exposure; still, the disasters led to major economic costs and a loss of public support for nuclear power.10

The incident prompted Japan and Europe to phase out nuclear power. Those positions are now being reversed amid growing concerns about energy security.

The human impacts of these accidents shouldn’t be trivialized. However, as we’ve noted, all power sources require trade-offs.

Nuclear Power Expansion: What Are the Key Challenges?

We see numerous opportunities to invest in what we anticipate will be a new era of growth for nuclear power. At the same time, we acknowledge the risks associated with construction, operations, regulation and nuclear waste management. Strategies to reduce these risks include the following:

1. Capital Intensity, Time and Expertise

New nuclear power plants face significant challenges because they can take years to build and require substantial upfront costs. It takes six to eight years (potentially longer) to build a nuclear power plant in most parts of the world. Building large reactors requires substantial upfront capital and qualified engineering, construction and project management teams.

Because nuclear plants take years to build, investors often prefer companies that already have long-term agreements to sell the electricity they’ll produce. The industry also needs more experienced workers, so companies with proven teams may be especially valuable. For these reasons, projects such as restarting existing reactors or extending the life of current plants may be viewed as lower risk than building entirely new plants.

Separately, SMRs aim to lower costs by standardizing designs, reducing build times and using factory-style manufacturing. Whether they can deliver at scale remains unproven; however, if they can, the implications for expanding nuclear power generation could be significant.

2. Policies and Regulations

The lengthy construction period for building nuclear plants is partly due to permitting timelines and safety requirements. Supportive policies (including production tax credits, zero-emissions credits, or contracts that fix the purchase price of power long into the future) reduce risk, while adverse policies can destroy value. Regulatory and policy environments can affect the risks and economics of nuclear power projects.

3. Fuel Supply Chains

While fuel costs are a modest share of the all-in cost of nuclear generation, supply security is also a consideration, particularly for the advanced fuels proposed for some next-generation reactors. Where a reactor’s fuel rods are produced can affect the security of the fuel supply. Countries without uranium enrichment capability, including most with nuclear power plants, must import fuel rods, which can introduce geopolitical risk.

Key Issues

Few suppliers. Only a few countries (China, France, Germany, the Netherlands, the UK and Russia) enrich uranium commercially for export. The U.S. produces only a fraction of the enriched uranium it needs for domestic power plants. However, efforts to expand capacity are underway (Japan and Brazil also have modest operations to meet domestic demand).11 This concentration could cause price and availability shocks. Russia is the largest supplier, raising risks of disruptions for Western countries.

Supplier lock-in. Nuclear fuel rods are typically specific to a reactor’s design, so importing them locks the buyer into the supplier for decades and entails legal and regulatory non-proliferation requirements. Still, in practice, importing nuclear fuel poses less geopolitical risk than importing fossil fuels, given nuclear fuel’s advantages:

Stockpiling ability. Nuclear power plants can store roughly two years’ worth of fuel on-site, allowing them to withstand unexpected supply disruptions. Oil and gas rely on "just-in-time" deliveries, making them highly vulnerable to sudden geopolitical shocks or transit chokepoints.

Energy density. A small amount of nuclear fuel generates a massive amount of power. While it takes 30 tons of fabricated nuclear fuel to power a 1-gigawatt plant for a year, roughly 3 million tons of coal or 700 million barrels of oil are required to achieve the same output. Thus, transportation is easier and less vulnerable to disruption.

Cost stability. While fuel is the largest component of the total cost of generating electricity in oil- and gas-fired plants, it’s a small part of nuclear power's total generation costs. Oil and gas prices are highly volatile, while nuclear fuel costs are quite stable.

4. Spent Fuel Storage

Storing used nuclear fuel rods requires relatively little space. The U.S. Department of Energy says that all the spent nuclear fuel generated by the U.S. commercial nuclear industry since the 1950s could fit on a single football field, stacked less than 10 yards high. Despite this, no one wants such storage sites nearby. Although the technology exists, finding permanent locations remains a challenge.

One way to reduce the size of the problem is to reduce the amount of nuclear waste requiring storage. Recycling in a “closed” system, still an early-stage concept, would reposition spent fuel rods from waste to an underutilized energy resource. The U.S. does not currently recycle commercial spent nuclear fuel at scale, but companies are pursuing this to recover material usable in certain types of reactors.

For example, Oklo, a nuclear power company, plans to pair advanced reactors with fuel recycling and to open an advanced fuel center and recycling facility in the early 2030s. The opportunity could be significant, as analysts estimate that the U.S. has enough stored nuclear waste to generate power for more than 100 years.

This is a proven, commercially viable technology — the U.S. government operated an experimental breeder reactor (EBRI-II) for three decades, using recycled fuel.12 Recycling would provide Oklo with a vertically integrated supply stream with the potential to become a multi-billion-dollar revenue opportunity within 10 years.

5. Decommissioning

Decommissioning costs are part of delivering nuclear power. Decommissioning funds are intended to cover the future cost of safely closing a nuclear power plant. How those funds are structured can affect who bears the risk if costs exceed expectations. Robust decommissioning mechanisms can reduce long-run balance-sheet uncertainty; weak ones can become a political and legal liability.

Where Are Opportunities in the Nuclear Power Value Chain?

Nuclear Operators: Electricity, Reliability and Long-Term Contracts

The case for investing in large nuclear operators typically hinges on plant performance, license extensions, authorized increases in maximum generation capacity, and the ability to monetize the scarcity value of clean, firm capacity — especially in regions with load growth and constrained interconnection.

Key factors for nuclear operators can include the duration of a plant’s license, its operational history and, in cases involving long-term power purchase agreements, the reliability of the counterparty. The Constellation–Microsoft agreement supporting the planned restart of the TMI Unit suggests that more hyperscalers and other large corporate users may contract for nuclear power’s firm, carbon-free output.

SMRs and Advanced Reactor Developers: Innovation, Scale and Commercial Viability

SMRs and other new reactor designs are often seen as the next chapter in nuclear power. However, many have yet to prove their commercial viability and scalability. Companies in the nuclear power supply chain, such as engineering and construction firms and component manufacturers, may benefit if SMR demand grows, regardless of which reactor designs gain traction.

In 2024, Amazon became both an investor and a client in a privately held company focused on meeting demand for modular nuclear reactors, committing to receive more than 5 gigawatts of new power. Shortly after the company went public in April 2026, it announced a collaboration with Louisville Gas and Electric and Kentucky Utilities, subsidiaries of PPL Corp., to explore deploying its SMRs in Kentucky to meet the state’s growing energy demand.

Oklo is also a relevant example. The company plans to commercialize and scale the proven EBR-II research reactor and technology. It has also signed term sheets and master power agreements to provide roughly 14 gigawatts of power. Oklo estimates that each new GW will generate roughly $1 billion in revenue, priced at $125 per megawatt-hour (competitive with nuclear power but still at the high end for other power sources).

The growing SMR market also includes companies that provide engineering and related services to the nuclear industry, including SMR projects. Some of these companies directly engineer, test and seek regulatory approval for their own small modular and micro-reactor designs.

‘Picks-and-Shovels’ Suppliers

Uranium Mining and Enrichment

Companies that produce nuclear fuel, which requires uranium mining, enrichment and conversion, offer a different risk/return profile than building and operating reactors. For example, Cameco, one of the world’s largest nuclear fuel providers, mines, mills and refines uranium.

Equipment, Services and Useful Life-Extension Supply Chains

Companies that support nuclear plant operations are another part of the nuclear power value chain. This includes outage services, maintenance and modernization, instrumentation and controls, specialized materials, engineered components and quality assurance.

For example, aerospace company Curtiss-Wright provides safety-related products, services and engineering solutions to the nuclear power industry. Mirion Technologies offers radiation monitoring and safety systems.

The performance of these companies may be influenced by activity across multiple areas of the nuclear power industry, rather than by a single plant operator alone. A recent Bloomberg article noted that mergers and acquisitions (M&A) activity is growing in this sector.13

Nuclear Technology Applications in Space, Defense and Fusion

Nuclear technologies have uses beyond power generation. Some examples under development include nuclear thermal propulsion and space power applications that could leverage nuclear power's energy density in locations where refueling is impractical. Other technologies use gamma rays to inspect pipelines and welds for defects and, in agriculture, to sterilize pests to protect crops without pesticides.

What About Nuclear Fusion?

Fusion is the holy grail of power generation — unlimited, with no radioactive processes or emissions. But while one or more pilot plants may be built by the early 2030s, commercial-scale fusion is not yet investable in the public equity market. Fusion would be vastly preferable to nuclear fission if it becomes commercially feasible.

However, replacing existing nuclear facilities would likely take considerable time due to the substantial capital investment and long construction timelines involved.

Why Is Nuclear Power Considered a Strategic, Clean and Firm Energy Source?

Electricity demand is growing rapidly as the IEA expects electricity consumption to outpace economic growth through 2030.14 We believe that meeting this demand calls for more than a single solution, requiring scale, reliability and affordability at the same time.

This isn’t a choice between nuclear and renewables — both are needed. Solar and wind capacity will keep growing, and costs will continue to come down. Nuclear adds firm, always-on power with near-zero emissions. Together, they can provide a more stable, resilient and secure system to meet the world’s electricity needs.

We will continue to rely on traditional energy sources, such as fossil fuels, for many decades. In our view, the priority should be to reduce emissions while ensuring reliability and controlling costs during this transition.

Nuclear plays a distinct role by delivering high energy output from a small footprint and supporting grid stability. It reduces dependence on fuel imports, which matters for countries without domestic oil and gas resources. Plus, advances in safety and design are improving its outlook.

The trade-offs are indisputable. Nuclear projects require time, capital and long-term stewardship. Public perception still weighs on deployment. Yet the strategic value is hard to replicate elsewhere. Nuclear sits at the intersection of energy security, affordability and decarbonization. We believe this position supports a durable role in the global energy mix, creating investment opportunities over the coming decade.

Authors

Head of Sustainable Investing

Sustainability: It’s in Our Genes®

Sustainability isn't just something we practice; it is part of who we are as a company and as global citizens.

International Energy Agency, “Electricity 2026,” February 6, 2026.

Sophia Chen and Nature Magazine, “Data Centers Will Use Twice as Much Energy by 2030—Driven by AI,” Scientific American, April 10, 2025.

Markets and Markets, “Heat Pump Market,” Report Code EP 6413, July 2025.

International Energy Agency, “The Future of Geothermal Energy,” December 13, 2024.

UNECE (United Nations Economic Commission for Europe), “Life Cycle Assessment of Electricity Generation Options,” October 29, 2021.

European Commission, “Speech by President von der Leyen at the Nuclear Energy Summit,” March 10, 2026.

Mari Yagamuchi, “Japan Adopts New Carbon Reduction Targets as It Plans to Boost Nuclear and Renewable Energy by 2040,” Associated Press, February 18, 2025.

Jennifer Hiller, “America’s First Commercial Nuclear-Power Projects in a Decade Just Broke Ground,” Wall Street Journal, April 23, 2026.

Omkar Khandekar, “War-Fueled Cooking Gas Shortage Hits Households, Restaurants and Factories in India,” NPR, March 19, 2026.

UN Scientific Committee on the Effects of Atomic Radiation, “A Decade After the Fukushima Accident: Radiation-Linked Increases in Cancer Rates Not Expected to be Seen,” March 11, 2021.

World Nuclear Association, “Uranium Enrichment,” June 6, 2025; U.S. Department of Energy Office of Nuclear Energy, “Uranium Enrichment, Explained,” November 4, 2025.

Catherine Clifford, “The Energy in Nuclear Waste Could Power the U.S. for 100 years, but the Technology Was Never Commercialized,” CNBC, June 2, 2022.

Veena Ali-Khan, “Here’s Why M&A Is Heating Up in Nuclear Infrastructure Sector,” Bloomberg, April 4, 2026.

International Energy Agency, “Electricity 2026,” February 6, 2026.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.