How Inflation-Protected Bonds May Calm Inflation Fears

Regardless of its growth rate, persistent inflation can erode investment values, highlighting the role TIPS may have in preserving purchasing power.

Key Takeaways

History shows that even when the inflation rate is seemingly low, consistently rising prices can weigh on your money’s long-term purchasing power.

We believe several economic and political trends suggest inflation will remain an important consideration for investors in the years ahead.

Unlike other bonds, TIPS adjust their face values according to the inflation rate, potentially offering protection from rising consumer prices.

While inflation has moderated significantly since climbing to a four-decade high in mid-2022, its current pace could still diminish your purchasing power over time. Even seemingly small increases in inflation can have serious negative effects on a portfolio’s value.

Consider this: From 1999 through 2023, the average annual inflation rate, as measured by the Consumer Price Index (CPI), was 2.5%. From a buying-power perspective, you needed $187 in December 2023 to purchase the same items that cost $100 in January 1999.

Higher Inflation Will Likely Persist

In our view, this trend is likely to continue. Inflation may remain a persistent threat, given several prevailing trends that include:

Record federal spending and deficits.

Elevated housing and rental costs.

Global trade and tariff uncertainty.

Corporate onshoring efforts.

We believe a portfolio allocation to Treasury inflation-protected securities (TIPS) may help avoid lasting damage from inflation.

TIPS: Bonds That Seek to Preserve Your Purchasing Power

TIPS are a class of U.S. Treasury securities designed to help protect investors from the long-term, corrosive effects of inflation. Figure 1 highlights the similarities and differences between traditional or nominal Treasuries and TIPS.

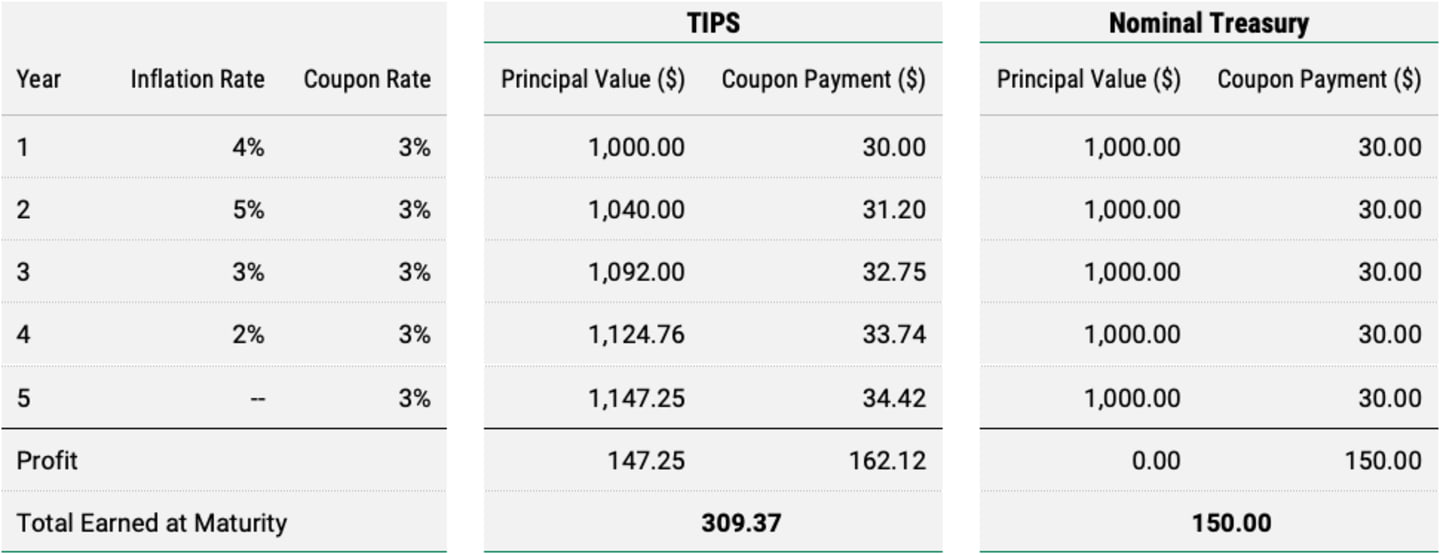

Figure 1 | Nominal Treasuries vs. TIPS

The principal value adjustment is the key feature setting TIPS apart. Unlike nominal Treasuries, the face value of TIPS changes along with the inflation rate. As inflation rises, the principal value of the security increases, creating a steadily growing stream of interest payments.

At maturity, the TIPS owner receives the original principal value plus the sum of all the inflation adjustments, as Figure 2 illustrates. Of course, the opposite is true in periods of deflation, which would cause the principal value of TIPS and the interest payments to decline. In the Figure 2 example, the TIPS paid more than double the interest of the nominal Treasury for the five-year period.

Figure 2 | How TIPS Adjust With Inflation Over Time

This hypothetical example assumes a five-year TIPS and a five-year nominal Treasury, each with a principal (face) value of $1,000 and a fixed coupon rate (the set interest rate assigned to a security when it’s issued) of 3%. For simplicity, this chart assumes one annual interest rate payment and one yearly principal value adjustment (rather than monthly). This chart contains assumptions that are intended for illustrative purposes only and are not representative of the performance of any security. There is no assurance investors can achieve similar results, and investors should not rely on this information as a specific recommendation to buy or sell securities.

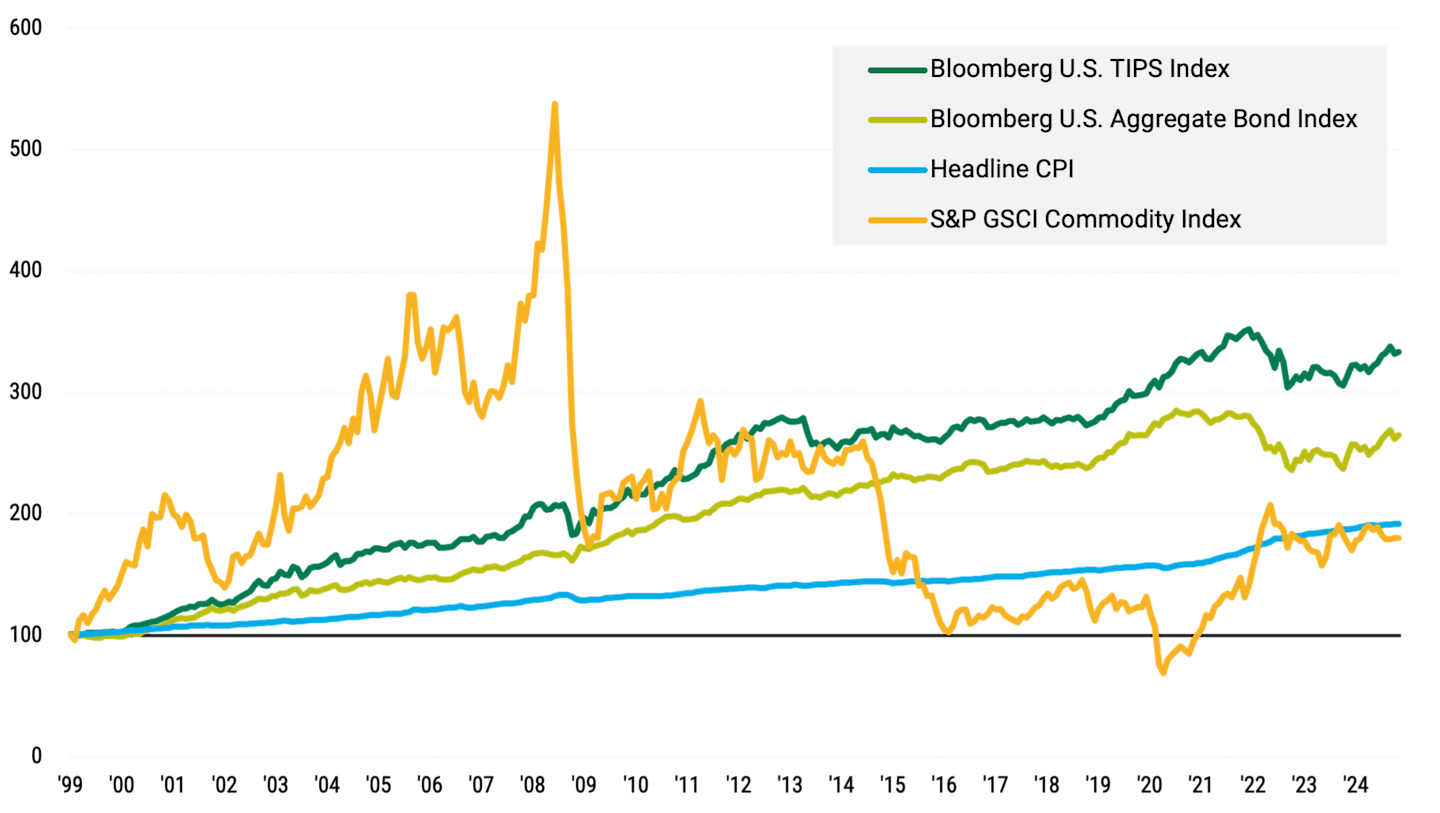

TIPS Have Historically Outpaced Inflation

TIPS have historically been an effective long-term hedge against inflation, significantly outpacing headline CPI over time, as shown in Figure 3.

TIPS have also outperformed commodities, another popular inflation-hedging asset class, and diversified core bonds over the last 25 years. The downside of gold and other commodities is that they have experienced periods of sharp volatility. TIPS, on the other hand, have historically delivered less volatile performance over time. So, along with their inflation-fighting qualities, TIPS may offer attractive risk-adjusted, long-term performance potential in a diversified portfolio.

Figure 3 highlights the historical performance patterns of TIPS and other instruments versus inflation.

Figure 3 | TIPS Have Battled Inflation With Less Volatility Than Some Other Investments

Cumulative Total Returns (Indexed to 100)

Data from 1/31/2001 – 11/30/2024. Sources: U.S. Bureau of Labor Statistics, CPI-U, Bloomberg. In our glossary, we define Bloomberg U.S. TIPS Index, Bloomberg U.S. Aggregate Bond Index and S&P GSCI Index.

What About Interest Rate Risk?

Because TIPS are Treasury securities, they’re backed by the U.S. government and contain virtually no credit risk — a key risk associated with most non-government-issued bonds. However, like all bonds, TIPS are subject to interest rate risk.

In general, TIPS have the potential to perform better than nominal Treasuries if interest rates are rising along with inflation. The inflation-adjustment feature of TIPS is designed to provide price protection as interest rates rise.

Nominal Treasuries don’t have this feature, and their prices typically decline when interest rates rise. However, if interest rates rise while inflation remains low or flat, TIPS prices could decline.

Consider TIPS When Seeking Inflation Protection

With inflationary pressures likely to linger, we believe TIPS may have a role in well-rounded portfolios. Unlike other securities, TIPS have features designed to protect against inflation and deliver solid performance potential in times of rising prices. We think these features make them effective tools for preserving purchasing power over time.

Authors

Senior Portfolio Manager

Explore our funds offering inflation protection potential.

Past performance is no guarantee of future results. Investment returns will fluctuate and it is possible to lose money.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

Investments in fixed income securities are subject to the risks associated with debt securities including credit, price and interest rate risk.

In certain interest rate environments, such as when real interest rates are rising faster than nominal interest rates, inflation-protected securities with similar durations may experience greater losses than other fixed income securities. Interest payments on inflation-protected debt securities will fluctuate as the principal and/or interest is adjusted for inflation and can be unpredictable.

Generally, as interest rates rise, the value of the bonds held in the fund will decline. The opposite is true when interest rates decline.

Diversification does not assure a profit nor does it protect against loss of principal.