Riding the Rotation: Why Non-U.S. Equities Have Led the Way

Can Non-U.S. stocks maintain their outperformance?

Key Takeaways

Several structural shifts in global markets helped non-U.S. stocks outperform U.S. stocks in 2025, and many of those trends continue today.

Key 2025 developments included improving capital allocation across European companies and enhanced corporate governance in South Korea.

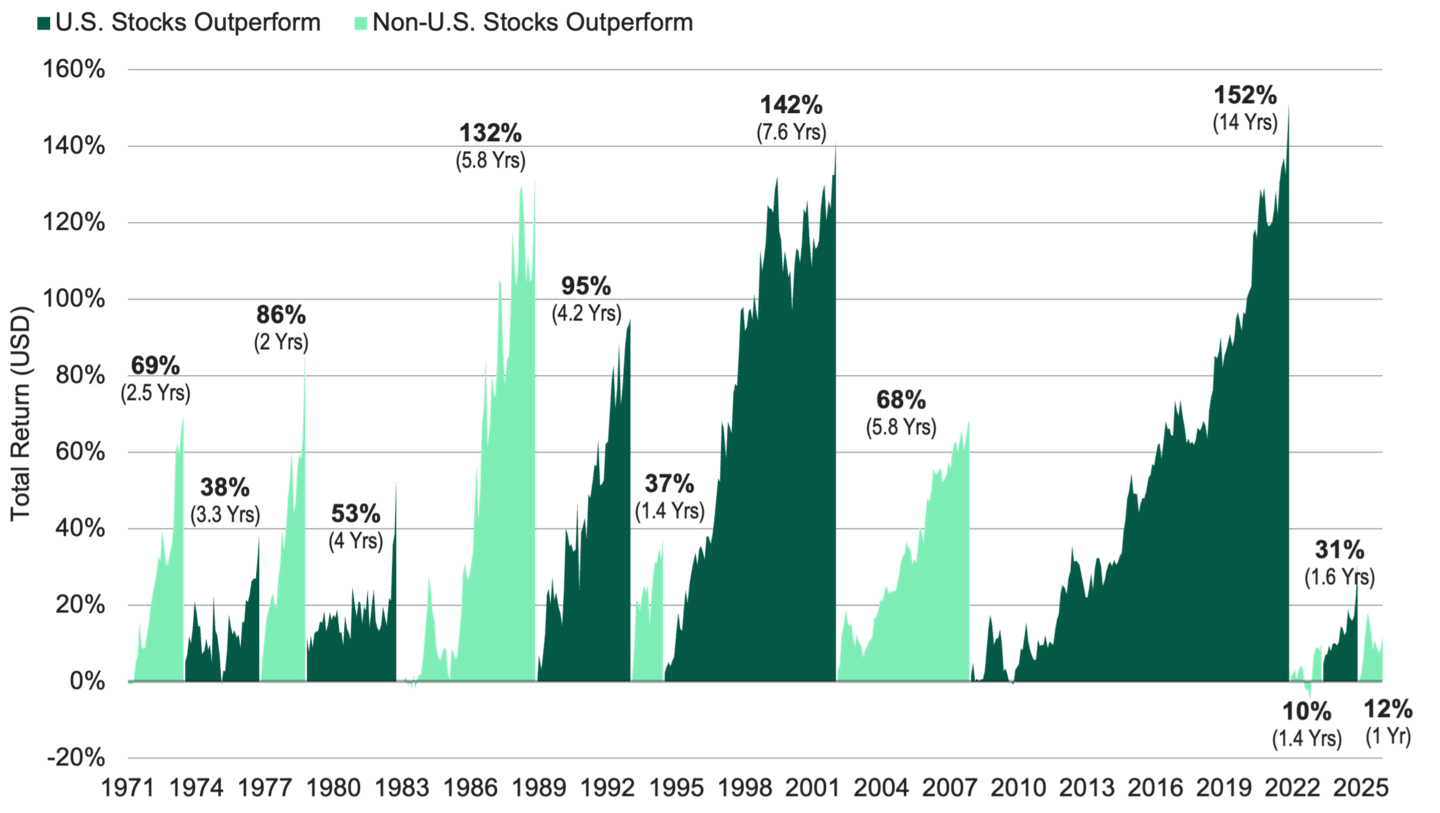

Historically, leadership shifts between U.S. and non-U.S. stocks have lasted for years. And when that shift occurs, value stocks tend to outperform.

Periods of market leadership by either U.S. or non-U.S. stocks have typically lasted several years. After the leadership shift in 2025 — characterized by strong non-U.S. stock performance — a key question for investors is whether this change will continue into 2026.

While the historical trends shown in Figure 1 suggest the answer is “yes,” we believe there’s more to it. We think structural and lasting changes in global markets, such as Western Europe and South Korea, support a positive outlook for international stocks.

Figure 1 | U.S. vs. Non-U.S. Stocks: Changes in Leadership Can Last for Years

Data as of 9/30/2025. Source: FactSet. U.S. stocks represented by the MSCI USA Index. Non-U.S. stocks represented by the MSCI EAFE Index. In our glossary, we define total return. Past performance is no guarantee of future results.

Valuations have further strengthened the case. Non-U.S. stocks are continuing to trade at meaningful discounts to U.S. stocks, which we think could create an opportunity to explore attractively valued companies that may benefit from these favorable conditions.

History also highlights the role of style leadership during periods of international outperformance. Value stocks have outperformed growth stocks in every period of non-U.S. leadership since 1971 by an average of 7.31%. More recently, value stocks outside the U.S. have outperformed growth stocks for five consecutive calendar years.1

This article will explore why we believe a rotation toward non-U.S. markets is happening and why this shift could favor value stocks.

Improving Business Conditions in Europe

After years of sluggish growth, Europe now faces long-standing challenges to its competitiveness. In a 2024 report commissioned by the European Union, former European Central Bank President and Italian Prime Minister Mario Draghi emphasized the need for better coordination among member countries, increased infrastructure investments and less dependence on fragile global supply chains.

The leaders of Germany, Western Europe’s largest economy, seemed to take Draghi’s recommendations to heart. In March 2025, the country’s parliament approved a €1 trillion stimulus plan to boost defense and upgrade infrastructure. To make this possible, lawmakers relaxed long-standing limits on government borrowing — known as the “debt brake.” It marked a major shift in fiscal policy that analysts believe will support economic growth for years to come.

For a country that has been cautious about accumulating much debt since World War II, the 2025 stimulus was a bold move.

Importantly, corporate earnings have yet to reflect much of the recent fiscal policy shift in Europe. We expect these measures to begin reaching company bottom lines in the first half of 2026, potentially providing a meaningful boost to earnings for key European businesses. In our view, 2025 was about setting the stage with new policy, and 2026 is when we’ll most likely start to see tangible results.

Workforce Flexibility Evolving Across Europe

Historically, it’s been challenging for Western European businesses to right-size headcounts due to the strength of their unions, extensive legal protections for workers and the robust unemployment benefits provided by employers.

Recently, however, we’ve heard from management teams of European companies that unions are increasingly recognizing the need for businesses to be more flexible and improve their cost structures to stay competitive internationally. This has resulted in greater flexibility in managing staffing levels, with less conflict from the unions.

Improving Outlook for European Banks

We have found that, generally, European companies are becoming more selective in how they invest their capital. This is evident in European banks that we follow, which, in recent years, have tended to focus more on improving capital efficiency.

And, in a break from the past, they have shown greater willingness to divest from non-core assets or underperforming segments and to use the proceeds to increase shareholder returns through dividends and buybacks. This is why returns on equity for European banks now hover closer to those of U.S. banks.2

Policy Changes Ease Pressure on Europe’s Auto Industry

In 2023, the EU implemented a measure to ban gas- and diesel-powered vehicles by 2035, requiring European automakers to switch to producing only electric cars by then.

European automakers found this deadline daunting and viewed it as a threat to their competitiveness. Meanwhile, a hyper-competitive auto market in China has led Chinese automakers to flood the European market with their less expensive electric vehicles.

Now the EU is softening its stance. Policies unveiled in December are more forgiving and call for a 90% reduction in emissions by 2035, instead of an outright ban on combustion engines. The EU also provided automakers with greater flexibility to meet near-term emissions targets. We believe these adjustments will help European automakers defend their market share across the continent.

Fixing the ‘South Korea Discount’

South Korea is home to many large global brands, but investors have needed to conduct sharp analysis and diligence due to heightened corporate governance risks. Historically, founding families of publicly traded companies have wielded outsized control over corporate affairs, leaving minority shareholders with virtually no say in management.

President Lee Jae Myung made reforming the country’s commercial code a central focus of his 2025 campaign. Following his election, South Korea made corporate boards legally accountable to all shareholders and curtailed the voting rights of major shareholders when appointing members to a company’s audit committee.

Even before the reforms, shareholder pushback was becoming more consequential. For example, Doosan Group tried to merge its construction equipment segment with its unprofitable robot-making unit. Shareholders opposed Doosan’s move because it inflated the share value of the robot company, making the plan untenable.

These changes make South Korea a more appealing destination for investment. We believe ongoing progress could create a multi-year tailwind, similar to the sustained boost Japan saw when it pushed to improve corporate governance more than a decade ago. South Korean stocks were the top performers globally in 2025, marking their strongest year of the 21st century.

What Earnings and Valuations Show About Non-U.S. Stocks

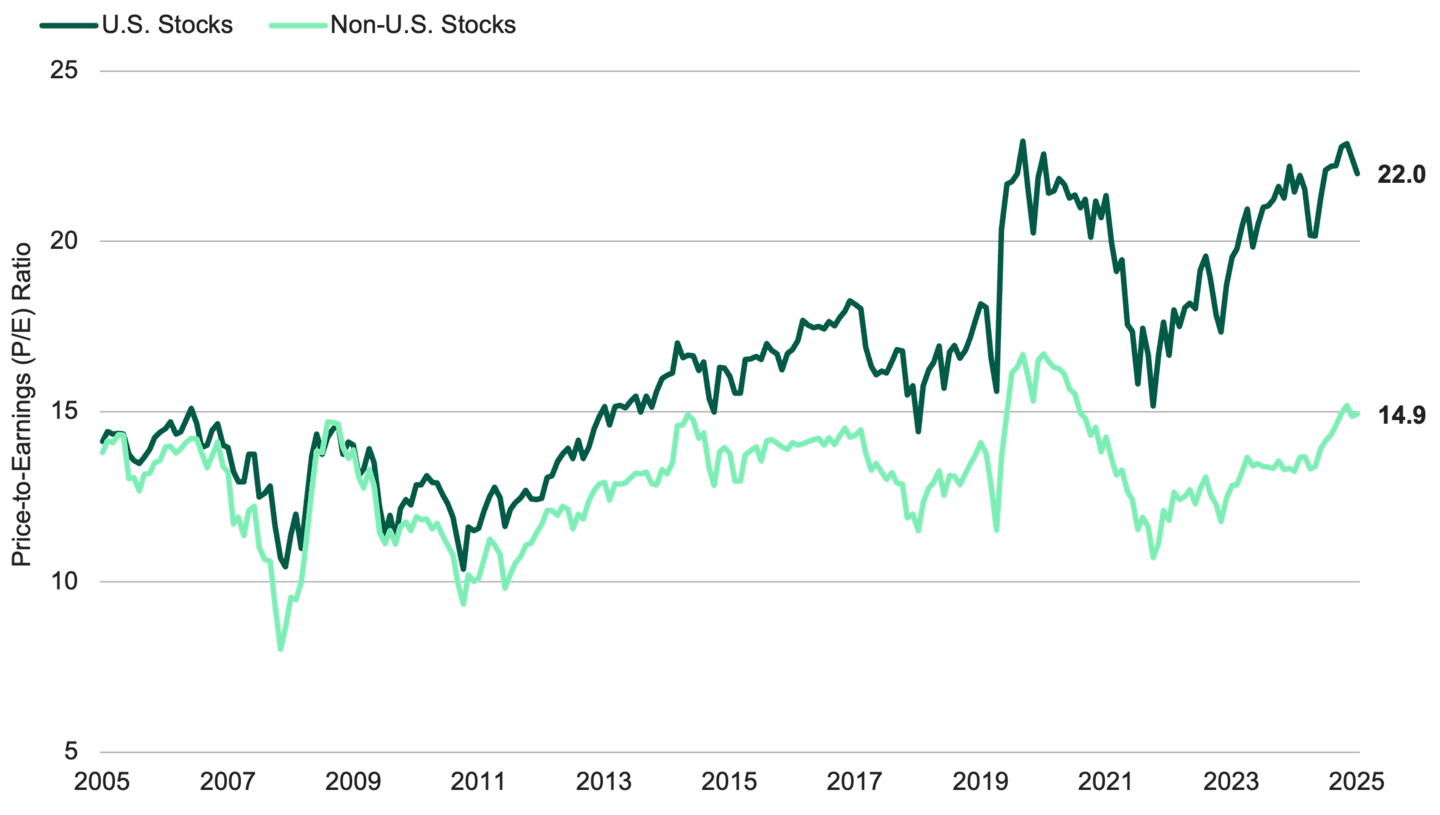

In addition to the positive trends we’ve discussed, non-U.S. stocks trade at notable discounts to U.S. stocks, as shown in Figure 2.

Figure 2 | Non-U.S. Stocks Are Historically Cheap Relative to U.S. Stocks

Data from 12/31/2006 - 12/31/2025. Source: FactSet. U.S. stocks represented by the S&P 500® Index. Non-U.S. stocks represented by the MSCI ACWI ex-USA Index. In our glossary, we define the price-to-earnings (P/E) ratio. Past performance is no guarantee of future results.

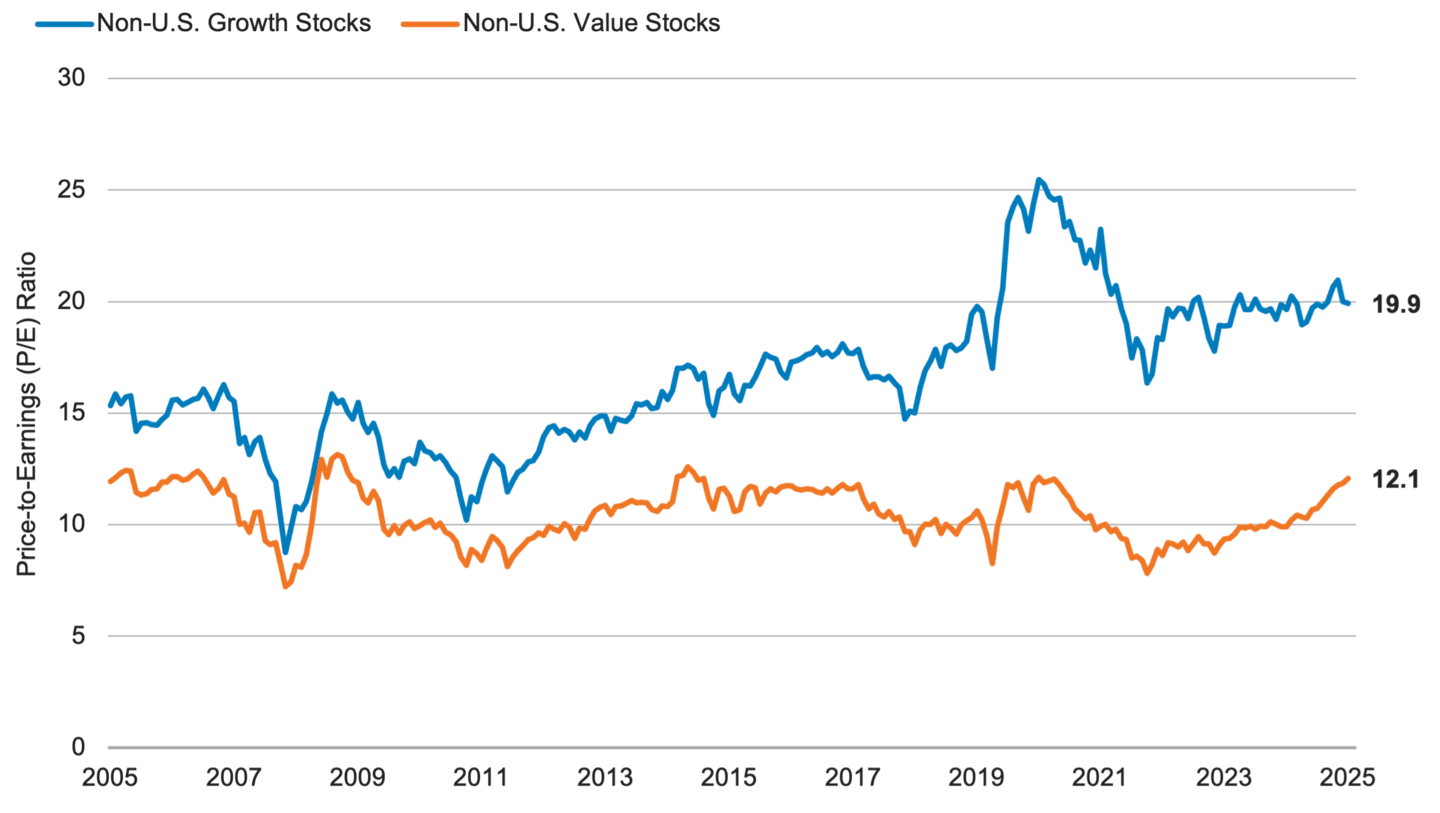

Within non-U.S. stocks, the valuation gap between value and growth stocks shown in Figure 3 continues to create opportunities.

Figure 3 | Value Stocks Also Trade at a Wide Discount

Data from 12/31/2005 - 12/31/2025. Source: FactSet. Non-U.S. Growth stocks represented by the MSCI ACWI ex-USA Large Cap Growth Index. Non-U.S. Value stocks represented by the MSCI ACWI ex-USA Large Cap Value Index. Past performance is no guarantee of future results.

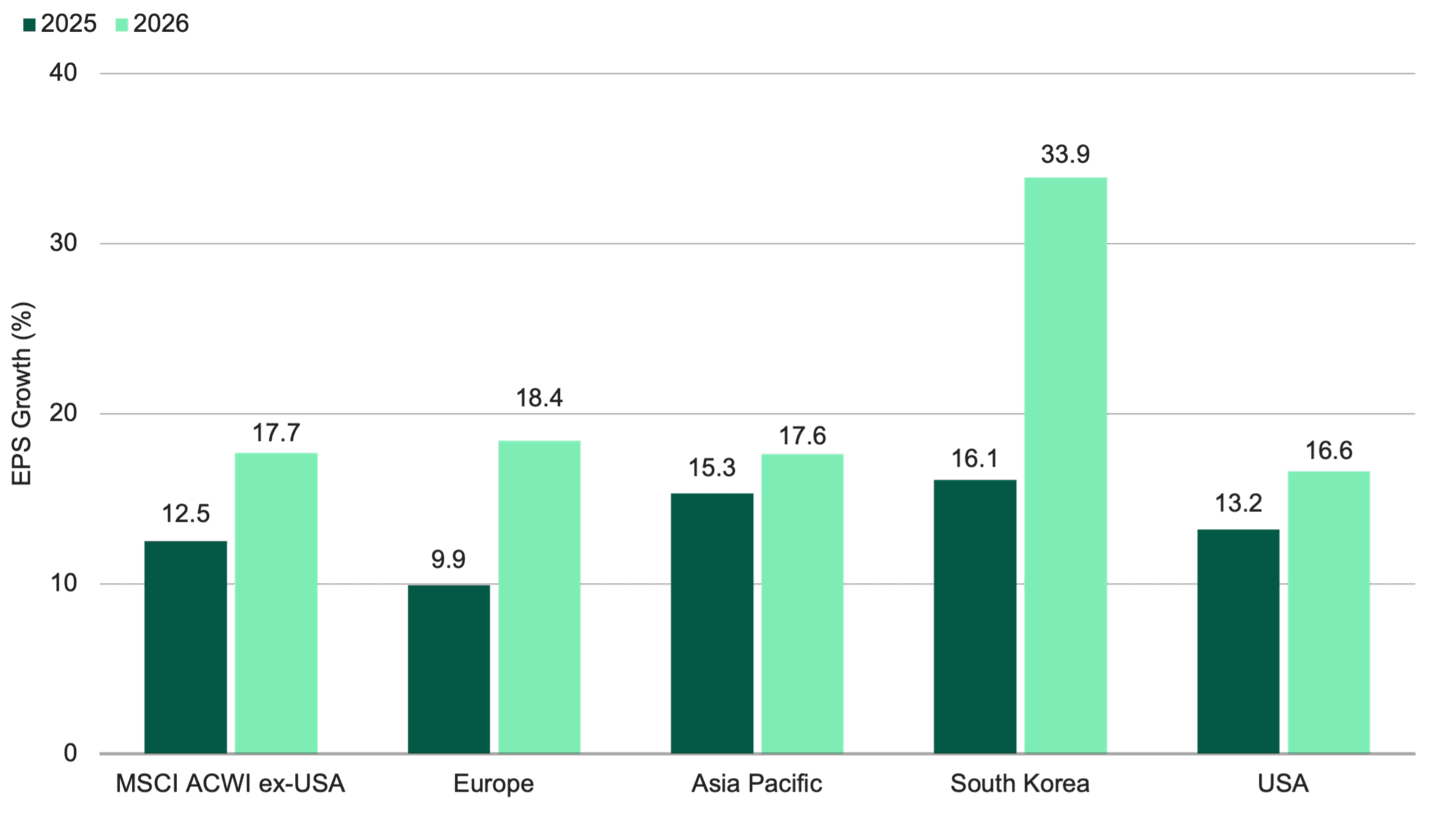

We believe these factors alone make a strong case for non-U.S. value stocks. It’s more compelling when considering that, according to FactSet, earnings-per-share (EPS) growth is expected to accelerate more among non-U.S. stocks than U.S. stocks in 2026.

In select markets, such as Europe and South Korea, EPS growth forecasts are even more pronounced. See Figure 4.

Figure 4 | Earnings Are Expected to Grow Faster Outside the U.S.

Data as of 12/31/2025. Source: FactSet. Forecasts are not a reliable indicator of future performance. Past performance is no guarantee of future results.

With valuation tailwinds, strengthening earnings and meaningful structural reforms in Europe and South Korea, we believe non-U.S. equities may offer potential opportunities for value-focused investors today.

Authors

Explore Our Global Value Capabilities

Source: FactSet. Data from 1/1/1971 to 12/31/2025. Calendar-year performance covers 2021 – 2025. The performance of U.S. and non-U.S. stocks is represented by the MSCI USA Index and MSCI EAFE Index, respectively. Non-U.S. growth and non-U.S. value stock performance is represented by MSCI AC World ex USA Growth Index and MSCI AC World ex USA Value Index, respectively.

As of 12/31/2025. Source: FactSet.

References to specific securities are for illustrative purposes only and are not intended as recommendations to purchase or sell securities. Opinions and estimates offered constitute our judgment and, along with other portfolio data, are subject to change without notice.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.