Strategies to Help Boost After-Tax Returns

Calculating your after-tax returns and thinking about investments and taxes together can pay off—especially when it’s time to pay Uncle Sam.

Key Takeaways

Many investors focus only on the investment returns before taxes, not realizing the potential impact until it’s too late.

Considering the after-tax returns of your investment options can lead to more efficient investment decisions.

Strategies could include choosing tax-efficient investments or tax-advantaged account types and tax-loss harvesting.

Federal income tax rates on certain types of investment income can reach up to 40.8% for investors in the top marginal tax bracket.1,2 That’s a considerable investment cost. Yet when evaluating investments, many investors focus only on the return on investment (ROI) before taxes, not realizing their tax bite until it’s time to pay the tax bill each year.

Being mindful of the true investment return after taxes can help you make savvy investment decisions. There are several ways to invest tax efficiently—all with the goal of improving your after-tax returns.

Add your tax rate into our Investment Rate of Return Calculator to see how taxes could be cutting into your investment returns.

Why It’s Worth It to Be Tax Aware

You could potentially pay less in taxes—and still stick to your investment plan—by choosing investments with better tax treatment. That means more money can stay invested in your nest egg to compound over time.

Understanding the potential after-tax returns on each of your investments will give you a clearer picture of the return you get to keep after paying Uncle Sam. Someone in the highest tax bracket with a goal to retire in 20 years may be disappointed to realize that a 10% rate of return on investments translates to an after-tax return of only 5.9% for bond income and 7.62% for stocks.

Calculating After-Tax Returns

= [(Ending market value – tax paid) – (beginning market value)] / (beginning market value)

Let’s look at the after-tax returns for an investment held by hypothetical investors Terry and Pam. The couple has a combined income of $375,000 a year and have $750,000 invested in an equity mutual fund. The fund’s dividend yield was 1.8% and had 10% in capital gains distributions before the end of the year.

Terry and Pam are pleased until they see their income tax return for the year. The dividends and capital gains distributions on equity mutual funds in a taxable account are potentially taxed at an 18.8% rate, so their tax bill for holding this investment is about $17,000. The couple wonders whether they are truly investing in the most tax-efficient manner to reach their financial goals.

Terry and Pam also have a $250,000 bond mutual fund investment held in a taxable account yielding 1.5% in income. Investment income from bond funds is taxed at the ordinary income rates. After calculating their income taxes, they estimate that their $1,000,000 total portfolio may cost up to $18,000 in taxes this year.

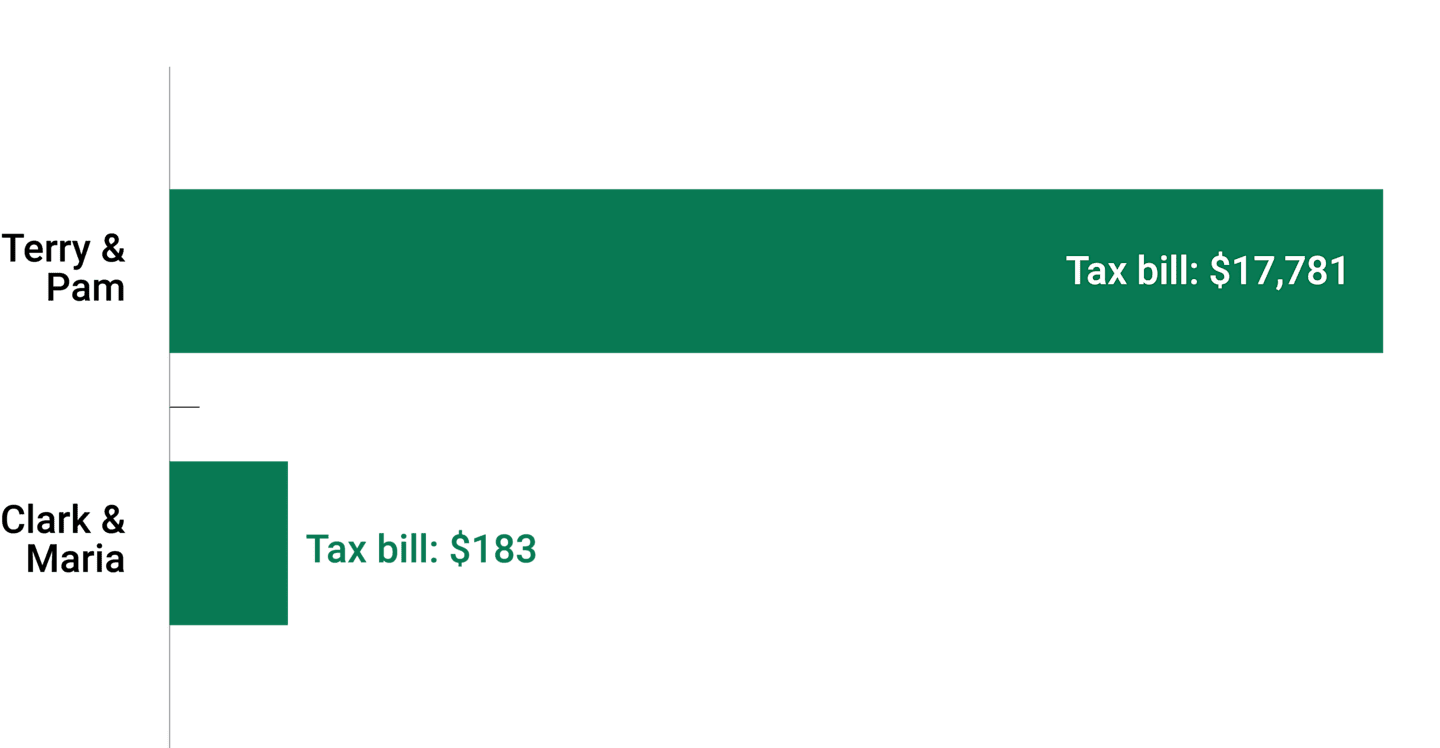

Let’s look at Terry and Pam’s tax costs compared to those of a tax-aware couple, Clark and Maria. Compare Costs

The Difference of a Tax-Aware Portfolio

Clark and Maria, another hypothetical couple, earn a household income of $375,000 and also have a 75% equity/25% bond investment portfolio totaling $1,000,000, like Terry and Pam. However, Clark and Maria chose a tax-managed equity mutual fund product that has no capital gains distributions but yields 0.13% in dividends, and a tax-free municipal bond fund that yields tax-exempt interest income of 0.09%.

Note: Municipal bond investments generate income that’s free from federal taxes and, in some cases, state and local taxes. They can offer yield advantages for those in both moderate and higher tax brackets.

Hypothetical After-Tax Portfolios

Source: American Century Investments. Assumes capital gains distributions are reinvested and dividends are qualified. This hypothetical situation contains assumptions that are intended for illustrative purposes only and are not representative of the performance of any security. There is no assurance similar results can be achieved, and this information should not be relied upon as a specific recommendation to buy or sell securities.

Although the two couples have a similar stock/bond investment mix, they have starkly different tax costs for the year. Terry and Pam may pay nearly $18,000 in taxes on their portfolio income. Clark and Maria’s tax bill on their portfolio may be about $200.

Once you understand the impact of taxes on your investments, you can explore various tax strategies to see if you can keep more of your returns.

Steps to Help Enhance After-Tax Returns

Several strategies may add tax efficiency to an investment portfolio if they fit within your investment plan goals.

1. Make Tax-Mindful Investment Choices.

ETFs are generally more tax efficient than mutual funds. Why? Two key reasons:

First, ETFs are structured differently than mutual funds, which reduces the turnover and potential taxable events.

Second, when ETFs are redeemed, the investor may be shielded from capital gains distributions generated due to other investors’ redemptions.

For more details on why ETFs are so tax efficient, check out Understanding ETF Tax Efficiency.

Municipal bonds, purchased individually or as an ETF or mutual fund, generate tax-exempt income at the federal level. They can also be tax-exempt at the state and local level, depending on the state and whether you are a resident.

Use the Municipal Bond Tax-Equivalent Yield calculator to determine what rate is required for a taxable bond to equal the tax-free rate of return of a municipal bond. For example, a California resident in the highest marginal brackets investing in a municipal bond with a yield of 5% could, according to the calculator, earn a tax-equivalent yield of 9.434%.

In other words, after taxes are paid, the investor pockets the same return from the 5% California municipal bond that they would have for a 9.434% taxable bond.

Separately managed accounts (SMAs)³ are portfolios of securities managed by an investment firm. They give investors the opportunity to customize the underlying holdings of a professionally managed portfolio. This customization has the potential to enhance returns, increases control and allows for use of tax-smart strategies.

Remember that in addition to capital gains distributions resulting from others selling their holdings, investors could incur capital gains when they sell. Investors can direct their SMA manager to sell and harvest tax losses to offset potential capital gains and reduce their taxable portfolio income.

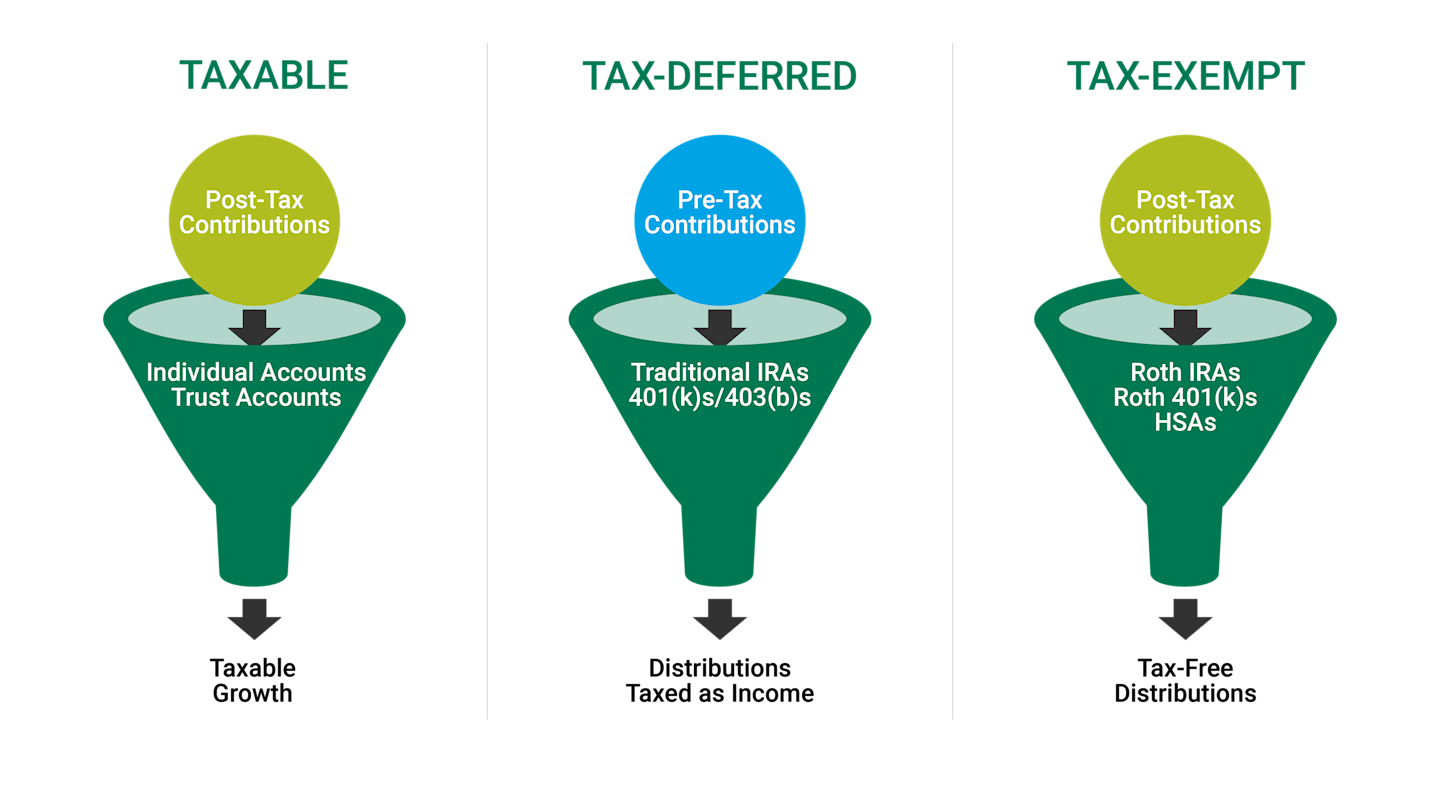

2. Choose the Appropriate Asset Location.

Choosing which type of account (such as taxable, tax-deferred or tax-free) you use to invest your assets is another way to contain taxes. Placing investments that may create higher levels of interest income or capital gains distributions in tax-deferred investment vehicles may reduce your current taxes, and ideally, you may be in a lower tax bracket later. This concept is commonly referred to as asset location.

For Terry and Pam, holding their equity mutual fund account in their IRAs or 401(k)s could allow them to defer taxes on the fund’s distributions and decrease their current tax bill by over $17,000.

You should generally seek to place actively managed mutual funds, which generate capital gain distributions, in tax-deferred accounts such as 401(k)s and IRAs, while ETFs often work well in taxable accounts because of their tax efficiency.

You also want to consider the holding period of your investment in taxable accounts to potentially qualify for the preferred capital gains treatment. Otherwise, realized gains held for one year or less will be treated as short-term capital gains rates, which are taxed at the ordinary income rates.

Investment Taxation by Account Type

Source: American Century Investments. Trusts may be subject to other tax rules. HSAs = Health Savings Accounts.

3. Tax-Loss Harvest to Offset Realized Gains.

You can manage your taxable gains through tax-loss harvesting, by selling investments at a loss to offset gains.

For example, if your stock is trading at a loss of $2,000, that loss can offset $2,000 worth of gains you recognized from selling another investment. This strategy can be complicated, so it’s good to discuss with a tax professional.

Volatile markets can create more opportunities for tax-loss harvesting. Good candidates for selling would be investments that no longer fit your strategy or that can be replaced with similar ones.

One thing to watch out for is the wash-sale rule, which prohibits deducting the loss from selling an investment and replacing it with the same asset or a “substantially identical” investment 30 days before or after the sale.4 Triggering a wash sale would disallow the loss from offsetting the gain until a later date. (See the Wash Sale details in our tax FAQs.)

Putting It All Together

Having an eye on after-tax returns matters because you get to keep more of your money invested—and have the opportunity for the power of compounding to kick in—for your financial goals.

Bringing tax strategies into your investing decisions is well worth it and can eliminate sticker shock when it comes time to pay Uncle Sam each year.

Looking to Keep More of What You Earn?

Get more information about how tax rules affect your investments.

Separately Managed Accounts (SMAs) are not available for purchase directly through American Century Investment Management, Inc. Client portfolios are managed based on investment instructions or advice provided by the client’s advisor or program sponsor. Management and performance of individual accounts may differ from those of the model portfolio as a result of advice or instruction by the client's advisor, account size, client-imposed restrictions, different implementation practices, the timing of client investments, market conditions, contributions, withdrawals and other factors.

IRS Circular 230 Disclosure: American Century Companies, Inc. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated with American Century Companies, Inc. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

This information is for educational purposes only and is not intended as tax advice. Please consult your tax advisor for more detailed information or for advice regarding your individual situation.

Please consult your tax advisor for more detailed information regarding the Roth IRA or for advice regarding your individual situation.

Taxes are deferred until withdrawal if the requirements are met. A 10% penalty may be imposed for withdrawal prior to reaching age 59½.

IRA investment earnings are not taxed. Depending on the type of IRA and certain other factors, these earnings, as well as the original contributions, may be taxed at your ordinary income tax rate upon withdrawal. A 10% penalty may be imposed for early withdrawal before age 59½.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

Long- and short-term capital gains are taxed at different rates. Long-term gains may only be offset by longer-term losses. Likewise, short-term gains may only be offset by short-term losses.