Cost Basis:

What It Means, Examples and Calculation

What you need to know to help minimize your taxes when selling investments.

At A Glance

Choose a Method

It’s up to taxpayers to choose the cost basis method when reporting sales of investments to the IRS.

Know the Difference

Different cost basis methods can change how much gain or loss you report, which may affect your tax bill.

Keep Good Records

Storing important documents and knowing what adjusts cost basis may lead to lower taxes and better returns on investments.

When the end of the year approaches, investors who want to make smart moves to reduce their tax burdens often take a closer look at the adjusted cost basis for investments, including mutual funds, exchange-traded funds (ETFs), stocks, bonds, cryptocurrencies and real estate.

You don’t have to wait until it’s time to file your taxes to begin cost basis management though. If you know what adjusts cost basis and how to use it in calculating your investment taxes, long-term planning can help you determine the best ways to minimize the amount of capital gains taxed.

Tax-savvy investors can include cost basis considerations in their investment decisions to help reduce their tax bills.

If you have investments in a taxable, non-money market account at American Century Investments®, then you can log in to your account and select the “Choose your cost basis method” link from the My Profile page. Or print and return the Cost Basis Election Form.

Have cost basis questions related to your American Century account? Jump to the Q&A below.

What Is Cost Basis?

Generally, cost basis is the price you paid for a security, including any applicable commissions and expenses. You use cost basis to determine whether you have a gain or a loss when you sell an investment. If the selling price is greater than your cost basis, your profit is called a gain. If the selling price is less than the cost basis, your deficit is called a loss.

The difficult part is figuring out your adjusted cost basis, as you might have invested money in your asset at different times or experienced a cost-adjusting event.

What Is Your Adjusted Cost Basis?

Certain investment types have unique aspects that will adjust your cost basis while you hold the investment. Here are some common adjustments.

The cost basis on a stock is relatively straightforward to calculate—the price you paid for the stock, including purchases made by reinvestment of dividends or capital gains distributions, plus other expenses like commissions to acquire the stock. However, some events will change the cost basis.

How Stock Splits Affect Cost Basis

When the company of an owned stock declares a stock split or reverse split, your per-share cost basis must undergo the same split. While your overall cost basis is not affected, your per-share cost changes.

For example, if you purchased 10 shares of stock at $10 each with no fee, your cost basis would be $100. Given a 2-for-1 stock split, your cost basis is still $100, but you now have 20 shares at $5 per share.

How Mergers Affect Cost Basis

Suppose you own stock in a business that merges with another company. In that case, you may receive stock in the new company and/or cash upon the merger.

If you receive stock, your new cost basis is calculated by multiplying your per-share cost basis with the ratio of new company shares you receive in exchange for old company shares. No taxable event has occurred.

If you are paid cash, a taxable event has occurred, so you may have a taxable gain that is calculated incorporating the original cost basis.

How Inherited Assets Affect Cost Basis

When you inherit assets, the investment’s cost basis becomes the asset’s fair market value on the previous owner’s date of passing. The basis is “stepped-up” or “stepped-down” to its current value in the marketplace, and the assets qualify for long-term treatment regardless of length of time held.

You are responsible for the potential tax on capital gains after you inherit the investment.

How Gifts Affect Your Cost Basis

The basis of gifted property depends on if you sell the security for a profit or at a loss. If you have a profit, you must assume the cost basis of the previous owner. If you have a loss, you must assume the lesser of the previous owner’s cost basis or the fair market value when the investment was gifted to you.

Be sure to ask the donor for the basis cost if you are gifted an investment.

While cost basis for mutual funds and ETFs is generally calculated in a similar manner, there are some differences in how it's applied and reported when it comes to tax implications.

Mutual Funds

With mutual funds, you must account for the fund’s dividends and capital gains distributions when tracking your cost basis. Flows into and out of the mutual fund are transacted in cash.

The manager often must sell portfolio securities to accommodate shareholder redemptions or reallocate assets. These sales may create capital gains for all fund shareholders, not just the ones selling their shares. These gains are taxable for all fund shareholders.

Your cost basis is reduced by the amount of tax paid on the distributed capital gains. Both amounts are reported to you on Form 2439: Notice to Shareholder of Undistributed Long-Term Capital Gains. Furthermore, any "return of capital" (nontaxable) distributions you receive from the mutual fund can reduce your basis risk and are shown in Box 3 of Form 1099-DIV.

ETFs

ETF managers accommodate investment inflows and outflows through the in-kind creation and redemption process, which enables them to shed securities that may generate significant capital gains.

ETF shares are passed back and forth on the exchange with an authorized participant without transactions occurring among the underlying securities. This creates an additional level of liquidity.

Trading in-kind may help eliminate or significantly reduce costs compared to the trading occurring in the underlying securities in mutual funds. In addition, when managers rebalance an ETF portfolio, they typically apply tax-management strategies, such as tax-loss harvesting, to minimize gains distributions.

Given that you may use coins to purchase goods/services and sell cryptocurrency for other cryptocurrencies, calculating cost basis can become a bit complicated. Nonetheless, digital assets like cryptocurrency are considered taxable property by the IRS.

Cryptocurrency follows similar methods for calculating cost basis as stocks. But it bears mentioning that you also create taxable events by using crypto to purchase an item or exchange it for another cryptocurrency.

For example, say you purchase a car for one bitcoin, and bitcoin is trading at $30,000 that day—but you purchased the bitcoin six months ago for $20,000, including fees. You realized capital gains of $10,000 ($30,000 - $20,000) that will be taxed at your short-term capital gains rate, which equals your ordinary income bracket because you held the coin for less than one year.

Bonds purchased in the secondary market may be purchased above par value and carry a premium or below par value and carry a market discount.

For bonds purchased at a premium, a brokerage firm may amortize the premium using the constant yield method. The amount of amortization will reduce your current-year income and cost basis.

For bonds purchased at a market discount, brokerage firms may accrue the market discount using the constant yield method. Your accrual will not be reported as current-year income and does not adjust upward your cost basis—you incur the tax liability for the entire accrual when the bond matures or you otherwise dispose of it.

With real estate, your purchase price minus all closing costs determines the cost basis; however, you must consider the impact of capital improvements and depreciation on your adjusted cost basis.

According to the IRS’ Publication 523, Selling Your Home, you may increase the cost basis of a property by the amount of allowed capital improvements made during your ownership.

Conversely, suppose you used the property as a rental and were allowed to deduct depreciation to offset the rental income for tax purposes. In that case, you would lower your cost basis by the allowable depreciation amount when you sell a property.*

* Corporate Financial Institute. Depreciation Recapture. January 6, 2023. https://corporatefinanceinstitute.com/resources/accounting/depreciation-recapture/

Why Is Cost Basis Important for Taxes?

Your cost basis determines your potential gains and losses and, therefore, the taxes you may owe when you sell investments. You—the taxpayer—are responsible for accurately reporting your cost basis information to the IRS.

Yet, the government is vested in ensuring your reported costs are accurately calculated because it affects your taxes. Therefore, Congress created laws requiring financial service companies to track and report cost basis to the IRS and to taxpayers for taxable accounts beginning in 2012 for stocks, in 2014 for bonds, and in 2021 for cryptocurrencies.

Planning Pointer

Your elected cost basis methods are critical to many financial decisions, including:

- What securities and lots to sell, which impacts your income tax liability.

- What shares to give to others when gifting to your children and family members.

- What shares to donate to charities to satisfy your charitable and philanthropic inclinations. Consider working closely with your tax advisor and investment advisor to ensure your decisions are appropriate for your personal situation.

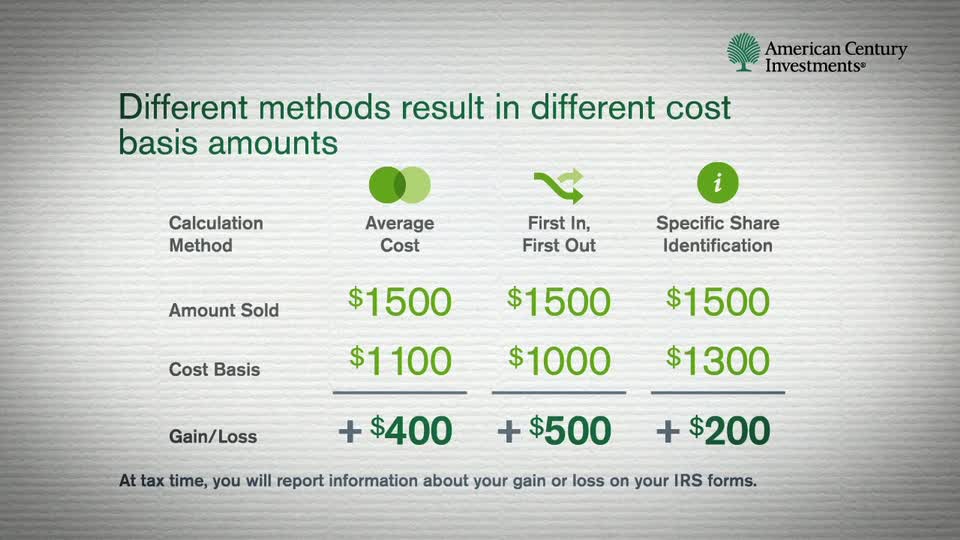

Hypothetical Cost Basis Calculation Examples

For comparison, we describe below how mutual fund cost basis is determined using three primary methods with the same purchase/sell dates.

As you calculate potential gains and losses through these cost basis method considerations, you can help determine which option is best for your investment portfolio.

Using the first in, first out method, it's assumed that the first shares purchased are the first ones sold.

If 20 shares are sold, they would be the first 20 shares purchased on June 15, 2022. To determine the mutual fund cost basis:

Multiply the purchase price of the shares x the number of the shares sold

$11 x 20 = $220 cost basis

Using the average cost method, the shares in the account at the time of the sale are averaged to determine the cost.

The cost of the 20 shares sold is an average of all the purchase prices. To determine the cost basis using the average cost method, there are three steps:

Step 1. Find the total amount invested.

Cost of all purchases including reinvested dividends = Total amount invested

$5,500 + $240 + $7,000 = $12,740

Step 2. Find the average cost of the shares.

Total amount invested / share balance = Average cost per share

$12,740/1,020 = $12.49 per share

Step 3. Determine the cost basis for the 20 shares sold.

Average cost of shares x the number of shares sold

$12.49 x 20 = $249.80 cost basis

Tax-Saving Cost Basis Strategies

Your choice of cost basis method is a tax planning strategy in itself. The specific-share ID method gives the most flexibility and control over the shares you choose to sell, give or donate. It also requires careful recordkeeping; financial software may offer you an easy way to track it. A couple of tax strategies investors use regarding cost basis include:

Loss/Gain Utilization

You dispose of shares with losses before the shares with gains consistent with minimizing potential taxable gains. When dealing with gains, the focus is on selling shares with a higher cost basis. Note that this method does not take the holding period into consideration, hence the higher cost shares could be held by you for one year or less and potentially subject to a higher short-term capital gain tax rate.

Time and Holding Period Management

If the share price has appreciated, using shares that have been held for more than one year may be taxed at the preferred long-term capital gains tax rate. If the price has depreciated, using shares that have been held for one year or less could offset other short-term gains you’ve realized.

Tax-Efficient Portfolio Moves

Investors also may find tax savings by keeping an eye on their overall investment mix through the following.

Tax-Loss or Gain Harvesting

A popular year-round tax strategy, tax-loss harvesting involves reducing your tax bill by selling shares at a loss to offset realized gains from other investments. It may also entail selling shares to realize gains (gain harvesting) and offsetting realized losses you may have.

What if you want to sell a security for tax purposes but still like the investment’s long-term prospects? You’ll want to be mindful of the wash-sale rule, which states that you can’t purchase the same or substantially identical shares within 30 days before or 30 days after a sale since the loss would be disallowed.

Asset Allocation and Location

How you divide your assets among different asset classes can impact your tax bill. For example, stock dividends are generally taxed more favorably than interest income from traditional bonds, so if you are in a high tax bracket, you may want to have more of your investments in taxable accounts. ETFs also tend to have superior tax efficiency relative to mutual funds.

Tips for Not Overpaying on Investment Taxes

Keeping an eye on the tax consequences of your decisions throughout the year may save you money when you file your taxes. While the IRS gives you flexibility in how you calculate your cost basis, it’s up to you to have the documentation to back it up.

These are just some of the ways to manage taxes on investments. Your tax preparer and financial professional may have more tips suited to your particular situation.

Q&A for American Century Clients

If you have investments in a taxable, non-money market account at American Century®, then you can log in to your account and select the “Choose your cost basis method” link from the My Profile page. Or print and return the Cost Basis Election Form.

Investment Consultants at American Century are not licensed tax advisors and do not provide tax advice.

American Century will select the corporate default method if we do not receive an election from you. Keep in mind, our default is not a recommendation and may not be the best choice for your situation. Cost basis method considerations are important decisions and should reflect what is best for your personal situation as determined by you and your tax advisor.

American Century Investments Cost Basis Default:

Brokerage - First In, First Out (FIFO)

Mutual Funds and ETFs - Average Cost

If you sold noncovered stock shares (purchased prior to January 1, 2012) and we have not provided average cost information on your statements, it may be because we were unable to calculate it. This may be because the records are not available or the shares were transferred from another financial institution. To find the details to calculate your cost basis, log in to your My Account page and review your transaction history.

Giftrust Clients

The maturity status of your Giftrust determines your cost basis options.

Matured Giftrust Accounts

You have the same choices for electing a cost basis method as other mutual fund account holders.

Non-Matured Giftrust Accounts

You do not need to make an election. American Century Investments will continue to complete the tax reporting on your behalf as outlined in the trust agreement. The trustee has selected the FIFO method for the shares purchased under the trust.

Corporate Clients

The regulations require investment firms to report sales and cost basis information on accounts held by S corporations as defined by the Internal Revenue Code section 1361(a).

If no response was received, we registered the account as an S corporation. We do not report sales and cost basis information on C corporations.

Transfer of Shares

In the event account shares are transferred to another company (including American Century® Brokerage) and you have not indicated the cost basis method to be used, the receiving company's default will apply regardless of the underlying fund company's default.

The Infrastructure Investment and Jobs Act passed in November 2021 requires any broker involved in a cryptocurrency transaction to track and report your cost basis on a Form 1099 to both you and the IRS. Otherwise, you may find your cost basis by looking at your records. And if you don’t have a recorded cost, you may estimate it by finding the historical price of your currency when you acquired it.

We are required to report cost basis to the IRS for certain bonds purchased after January 1, 2014. The reporting requirement covers a bond if it has a fixed rate, fixed maturity, and fixed payment schedule, even if it is callable by the issuer. At this time, we will not report cost basis to the IRS for more complex bonds or debt instruments issued with less than one year to maturity.

The IRS will not err on your side as the taxpayer when calculating your cost basis, so it's worth maintaining a good recordkeeping system to determine your adjusted cost basis since you bear the responsibility. You may find it beneficial to use financial software to keep your transactions in one place.

For taxable bonds purchased at a premium, American Century does not amortize the premium. Your income will not be reduced by the amount of amortization nor will your cost basis be adjusted.¹

For bonds purchased at a market discount², you may advise us to calculate your accrual using the ratable method instead of the constant yield method.³ Additionally, you may opt that the accrual be included as current-year income. This method is known as inclusion. We will adjust your cost basis upward by the amount of the accrual if you chose the inclusion method.

If you would like to choose an option other than the default methods, please mail a request signed by all authorized owners/signers to:

American Century Brokerage

P.O. Box 419146

Kansas City, MO 64146

A request to change the default amortization method will apply to all of your covered bond holdings, and it must be received in the year in which the election is to apply.

See IRS Publication 550 for additional information.

For OID instruments, the discount is the difference between the adjusted issue price and the purchase price.

Once the constant yield method has been used to report accruals for bonds purchased at a market discount, it cannot be revoked.

Looking to Keep More of What You Earn?

Get more information about how tax rules affect your investments.

Long- and short-term capital gains are taxed at different rates. Long-term gains may only be offset by longer-term losses. Likewise, short-term gains may only be offset by short-term losses.

IRS Circular 230 Disclosure: American Century Companies, Inc. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters contained herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone unaffiliated with American Century Companies, Inc. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

This information is for educational purposes only and is not intended as tax advice. Please consult your tax advisor for more detailed information or for advice regarding your individual situation.

This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.

Giftrust® is an irrevocable trust designed to be given as a long-term gift to someone other than yourself or your spouse and is not available for an IRA. The Giftrust investment is invested in the Growth fund.

Brokerage Services are provided by American Century Brokerage, a division of American Century Investment Services, Inc., registered broker/dealer, member FINRA, SIPC.