Concentration Risk—Too Much of a Good Thing?

You invest in stocks and stock funds for growth, but what happens if all your investments act the same way? Find out how to mitigate concentration risk with diversification.

Key Takeaways

Stock investments can be key to helping investors get the potential growth they need to reach their goals. But they shouldn’t all act the same way.

Having too many stock investments that all react the same way to market conditions can open you up to concentration risk and potentially amplified losses.

Diversification can help mitigate concentration risk, but it’s not always easy and often misunderstood. Review tips to help ease the risk of too much of a good thing.

Investing in stock funds has been a popular strategy to potentially grow your money, but having too many investments that act the same way to market events could open you up to large losses.

Learn about concentration risk and how to know if the stock portion of your portfolio is diversified enough from financial consultants Zach Roth and Addison Schubert.

What Is Concentration Risk?

Concentration risk is the threat of outsized losses that could occur if you have a large part of your holdings in a particular investment, asset class or market segment in relation to the rest of your portfolio.

According to the Financial Industry Regulatory Authority (FINRA), concentration risk can occur intentionally (e.g., you expect a particular investment will perform well, so you put all your eggs in that basket), or unintentionally. Unintentional concentration risk could occur if one of your investments performs extremely well and moves your portfolio off balance.

Zach says, “Sometimes investors just have one large-cap growth fund, and that’s all. Or, they have multiple large-cap growth funds that all react the same way when the market goes up or dips.”

“While an all large-cap growth portfolio can feel comfortable when the asset class performs well, which it has done a majority of recent years, it’s not so comfortable if those stocks take a significant loss,” says Addison.

Narrow Return Sources Can Mean Greater Risk

Concentration risk can be particularly troublesome when stock market performance is based on a few stocks or areas of the market, rather than dispersed across more asset classes, industries and sectors.

“This was the case in 2023,” says Addison, “A handful of technology stocks accounted for a large share of market gains.” Concentration in a few stocks in a portfolio can mean more risk. The same stocks that had significant positive performance in 2023 had experienced losses just the year before—and could fall again in the future.

“The up and down cycles of different asset classes is another argument for diversifying your stocks—actually your entire portfolio—to help mitigate losses and set you up for potentially better success in the long run,” says Zach.

Avoiding Concentration Risk in Your Portfolio

Addison says, “A good place to start in managing concentration risk is with what is likely most people’s largest slice of their portfolio pie—their stock portion.”

You may wonder if having stocks and bonds in your portfolio is enough. It could be, but it also depends on the kinds of stock and bond investments you own.

“Having one large-cap growth stock fund and one bond fund is not true diversification,” says Zach. “That’s also true if you have several funds but all their top holdings are similar, or they tend to react the same way when the markets change.”

How to Diversify Your Portfolio and Manage Concentration Risk

Diversifying your stock portfolio means having a wide range of different kinds of stocks that span market capitalization sizes, investing styles, market sectors and geography—the ideas is to have a stock portfolio that covers the gamut.

"It may help to have a refresher about how different asset classes are the building blocks for your portfolio,” says Zach. Or learn the role each type of stock plays and how they complete your portfolio.

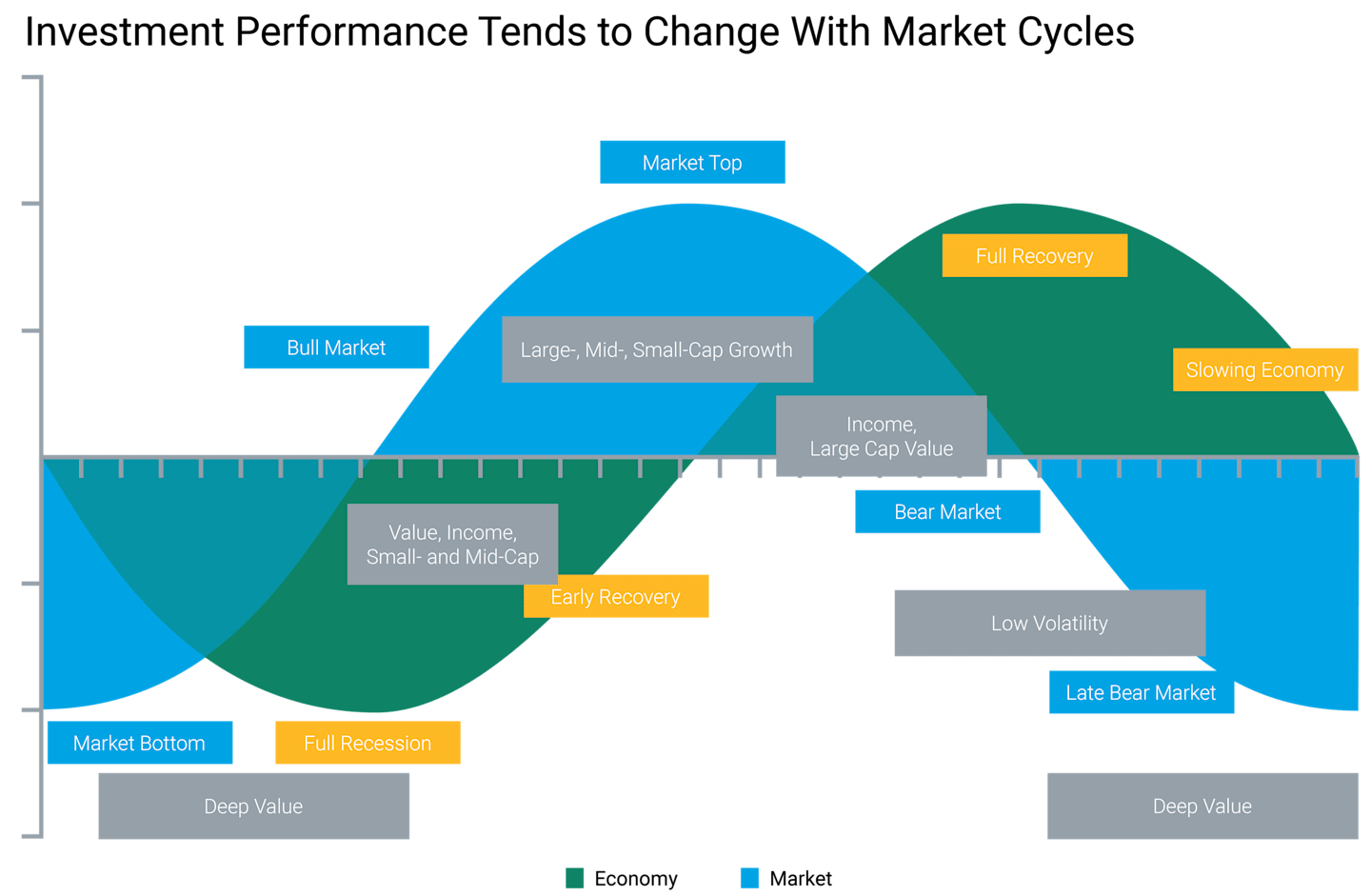

In addition, it may help to know how different stock asset classes have historically performed during economic and business cycles, as shown in the image.

Source: American Century Investments, June 2024.

The chart is a general representation of when different investment types have historically performed more favorably during different economic cycles. It is intended for illustrative purposes only and does not represent the performance of any security. There is no assurance similar results can be achieved, and this information should not be relied upon as a specific recommendation to buy or sell securities.

Consider the following:

1. Choose Investments of Different Company Sizes (or Market Capitalizations)

Market capitalization refers to company size: generally large, mid-size and small. Choosing large-cap stocks means investing in larger, more established companies, which historically have been less risky than mid- and small-cap companies. Including all cap sizes in your portfolio may be beneficial when conditions are more favorable for a particular company size.

“An example of this is that our investment professionals believe the recent trend of companies moving their manufacturing to the U.S. (instead of overseas) may be a good backdrop for small-cap stocks,” says Zach. Read about a real-world example of reshoring and why it might mean good news for small-cap investments.

2. Include Different Investing Styles: Growth and Value

Growth stocks are expected to have high future earnings, while value stocks trade at a discount relative to their true value. Each style has historically performed better under different market and economic conditions.

For example, growth stocks have historically performed well in bull markets and during periods of economic expansion, but they can also more volatile. Value stocks have done better in bear markets and recessionary periods and tend to have lower volatility.

But keep in mind that a decade of growth stocks outperforming value stocks has been unusual and could harm the balance of your portfolio. “Consider both investment styles,” says Addison. “That way you’re not potentially missing out on part of the market that may be performing better or opening yourself up to more risk.”

3. Select Various Market Sectors and Industries

Sector funds focus on one segment of the market, like technology or utilities. “Having a fund that includes as many sectors as possible may be a consideration for diversification, especially if an economic event negatively affects an entire sector of the market,” says Zach. Investors can have a sector-specific investment, but it should not be a core holding. You’ll also want to consider including plenty of other types of investments for a balanced portfolio.

Sectors and industries can be affected positively and negatively by economic changes, government policies or investor interest. For example, the manufacturing sector may suffer during tight labor markets, supply chains interruptions or economic uncertainty.

4. Look Beyond Domestic Stock Borders

Another way to diversify your stock portfolio is to consider global funds (which include U.S. stocks), international funds (which don’t include U.S. stocks) and emerging markets funds, which invest in countries that have developing economies.

“Many U.S. investors have a domestic stock bias,” says Addison, “But there can be benefits to investing in funds that include companies outside the U.S.” Not all economic conditions are favorable for domestic stocks, so seeking to capture returns from other parts of the world is smart to consider.

Diversification Roadblocks

For all the times you’ve heard it’s important to diversify your portfolio, the truth is that many people don’t practice this strategy. That may be because they are loyal to a particular investment and don’t want to give up a perceived good thing, or they misunderstand diversification.

Letting Go of a Good Thing

“Diversifying your portfolio could mean selling shares of a fund that’s done well for several years, which doesn’t always feel good,” says Addison. Investors can be very loyal to an investment that has grown their portfolio over time, even if there were some less-than-stellar years. They also may feel more comfortable with the familiar.

Selling some shares of a fund you’ve owned for 20 or 30 years may seem counterintuitive. “It can be tough because a diversified portfolio’s returns may not seem as great,” says Addison. “When it comes to performance, the highs may not be as high, but the lows may not be as low. A diversified portfolio can give investors a potentially smoother ride and help them be less likely to make emotional decisions when markets drop.”

A pitfall of not having a diversified portfolio may be that it’s more tempting to make an emotional decision when markets are volatile. That goes back to the idea of the smoother path diversification can offer versus the roller coaster of having all your investments react the same way. “You may get higher highs with a concentrated stock portfolio, but you’ll also experience lower lows if they all drop,” says Zach.

“We see a lot of investors wanting to jump out of the markets when the stock market drops and unfortunately, they usually want to move to cash.” Says Addison. “That can set them up to miss out on gains when there’s a market recovery.”

Misunderstanding Diversification

Zach says some people may not truly understand diversification. “For example, investors may believe they are diversified when they hold funds at different investment companies.”

He says, it’s important to not only look at the financial firms you invest with, but at your whole portfolio and how diversified you are across the board. “Many times, there can be an overlap in asset classes. People could be investing with more risk than they intended by owning funds with similar holdings from different firms.”

Other investors may try to diversify with multiple asset allocation products, such as owning more than one fund of funds. Zach says, “I’ve seen investors who own three risk-based portfolios—a conservative, a moderate and an aggressive portfolio—thinking it covers them for all market conditions.” He explains, “What that really does is give them a portfolio that is off balance and doesn’t match how they specifically feel about taking risks.”

How Can You Know If Your Portfolio Is Diversified Enough?

Diversifying your portfolio can take time and effort if you’re choosing single funds or stocks. “It can be a challenge to do on your own,” says Zach. “But there are options such as choosing an already diversified portfolio or working with a financial professional.” And then there’s the work of exchanging funds or selling shares to get your portfolio truly diversified.

The benefit of choosing to work with a financial advisor is that they will take you through a risk assessment. “So not only do you get recommendations for a diversified portfolio,” says Addison. “It’s a portfolio that’s diversified according to how you feel about risk.”

In our experience, investors who have a diversified portfolio that matches their risk appetite are more comfortable riding out those market ups and downs.

Authors

Financial Consultant

Financial Consultant

No Time for Diversification?

Consider an already diversified portfolio that includes a mix of several different stock and bond investments and is designed to help manage market ups and downs.

Diversification does not assure a profit nor does it protect against loss of principal.

Historically, small- and/or mid-cap stocks have been more volatile than the stock of larger, more-established companies. Smaller companies may have limited resources, product lines and markets, and their securities may trade less frequently and in more limited volumes than the securities of larger companies.

International investing involves special risks, such as political instability and currency fluctuations. Investing in emerging markets may accentuate these risks.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

Deep value stocks are less expensive and priced low compared to its earnings level. The intrinsic value of the stock is much higher than its current price.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.