Investment Risk Management: An Investor’s Guide

When you understand the relationship between investment risk and reward, you can create a portfolio to get you on track toward your financial goals.

Key Takeaways

There is no way to completely avoid risk when investing, but some types of risk can be reduced with the right strategies.

A portfolio’s risk level should depend on the investor’s comfort with risk, along with their specific goals and time horizon.

Understanding specific investment challenges—like market risk, inflation, interest rates and credit risk—can also help.

People often see themselves as either “fully invested” or “not invested” in the markets, or consider their holdings as either “risky” or “safe.”

But investment risk is not either/or, and investors may not always consider the varying degrees of risk in between. There are endless options between putting money under your mattress and betting it all on high-risk investments.

Understanding Investment Risk

All investing involves some level of risk, and we walk through investment risks with clients all the time. If they invest too aggressively in stocks, the potential benefits may not outweigh the risk they’re taking on.

But if they try to avoid risk altogether by selling or moving everything to conservative investments like money markets, that adds another type of risk. Selling during a market downturn can make it difficult to get back into the market to participate in the next upswing.

Learning how to manage different types of risks can help you create an investment portfolio to help you work toward your financial goals.

Basic Investment Risks, Plus Strategies to Manage Them

If you’re a beginner or a more hands-off investor, it’s important to understand the basic types of investment risks and ways you may be able to manage them. The more you know, the better you’ll be at choosing investments that are suited to your goals.

Market Risk

Economic events can cause the value of your investments to drop. Market volatility can be spurred by anything from news headlines to geopolitical events to weather—anything that causes investors to be wary.

Strategy: Diversify Your Portfolio

There’s no way to eliminate market risk, but diversifying your portfolio may help mitigate your potential losses. Diversification means including a mix of investment types that react in different ways when markets change. When one area of the market is not performing well, it may be offset by others that are.

Inflation Risk

Inflation—the increase in the prices of goods and services—can erode your purchasing power if your investments can’t keep pace. If you don't achieve a rate of return that’s higher than inflation, your investments won’t be able to buy as much down the road. This means you will have to invest more, wait longer to retire or even potentially never reach your intended goals.

Strategy: Add Risk to Outpace Inflation

You may need to take on some additional investment risk (with stocks, for example) to get returns that will outpace inflation. Note that riskier investments can mean higher highs but also lower lows. You can also hedge against rising prices with investments that are specifically designed to combat inflation.

Interest Rate Risk

Interest rates and bond prices generally move in opposite directions, so higher rates usually mean lower bond prices. Prices of longer-maturity bonds may rise or fall rapidly in response to interest rate changes.

Strategy: Choose a Shorter Duration

A bond’s duration measures its price sensitivity to changes in interest rates. Shorter-duration bonds are usually less volatile when interest rates rise. The longer the duration, the more the bond’s price will change.

Credit/Default Risk

Investing in bonds comes with the possibility that the bond issuer will fail to repay the loan. Credit ratings reflect an issuer’s financial strength and ability to make timely interest payments.

Strategy: Look for Quality

Higher credit quality can help decrease your risk. Investment-grade bonds have less risk of issuer default but also lower yield potential (rate of return). They have credit quality ratings of BBB or higher.

For Savvy Investors: Advanced Risk Management Strategies

Your portfolio should account for a broad range of investment risks, whether you build and maintain your portfolio yourself or consult a financial professional.

Allocation/Concentration Risk

When an investor is heavily invested in one asset class or a single stock, price declines in that asset type or stock could significantly impact the value of the whole portfolio.

Strategy: Choose Asset Classes Carefully

Asset classes are collections of investments with similar characteristics and market performance (tech stocks are a good example). Allocating your investments across different assets is crucial to avoiding sudden drops in any single asset class or stock.

Reinvestment Risk

Related to interest rate risk, reinvestment risk is the inability to reinvest money into securities that will earn the same or higher rates as your original investment. For example, if your bond matures during a lower-interest rate environment and you want to reinvest the principal, your new bond may not earn as much as before.

Strategy: Choose a Longer Duration

Having some longer-maturity bonds or bond funds may help mitigate reinvestment risk in this situation. Adding duration with longer-maturity holdings may help generate capital appreciation when rates fall. However, if rates have not yet peaked, this move would increase your interest rate risk.

Sequence of Returns Risk

Investors nearing retirement are more susceptible to portfolio losses because the sequence, or timing, of returns may matter more than the average return. When investors near retirement suffer negative returns and a loss in the value of their portfolios, it’s more detrimental than a loss suffered by younger investors who have more time to recover.

Strategy: Lower Your Stock Exposure

As you approach retirement, you may want to shift to a more moderate strategy so that you’re less susceptible to potential losses. That means decreasing your stock allocation and increasing exposure to bonds and other short-term investments.

Longevity Risk

This is the risk that retirees haven't saved enough for retirement, effectively meaning they outlive their money. As investors move closer to retirement, longevity risk can come into play.

Strategy: Add Risk Early On

Understanding and adding investment risk early on, when you’re beginning to invest, could help you create a strategy that’s aggressive enough to help fully fund your retirement.

Understand How Risk Affects You

Adding investment risk to your portfolio can be concerning, but it might also help you get the returns you need to reach your goals. There’s also a difference between how much risk you can take in theory and how much you’re willing to handle in reality.

As you think about your investment strategy, you should consider two things: your time horizon and your risk tolerance.

Time Horizon: How Much Time Do You Have?

The longer you have to invest, the more risk you can likely take because your investments have time to recover from market drops. Generally, the closer you are to your goals, like retirement, the less risk you’ll want to take.

Risk Tolerance: How Does Risk Make You Feel?

Knowing your willingness to take risks can help you choose investments that best suit you. Avoiding risk (or taking as little risk as possible) may prevent you from reaching your goals. On the other hand, choosing riskier investments to compensate for a lack of savings could put your investments in a precarious position.

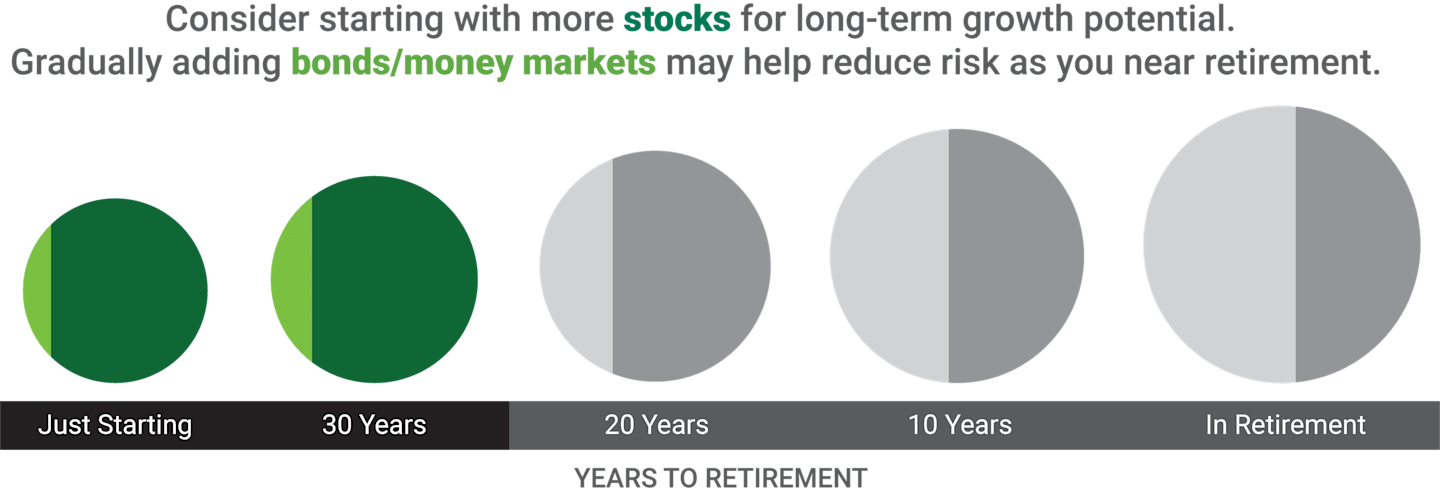

How Your Risk Needs May Change Over Time

Hypothetical Portfolio Illustration

Younger investors often start with smaller account balances. A stock-heavy portfolio might seem riskier, but theoretically, with lots of time to add to savings, market ups and downs have the potential to be absorbed before retirement.

Source: American Century Investments. For illustrative purposes only. The examples indicate hypothetical allocations. The circles assume increased contributions over time and are not meant to indicate gains based on market performance.

Your specific percentages of stocks, bonds and money market investments will vary depending on your own goals, time frame and risk tolerance, but this may give you a place to start as you evaluate your current and future investment plans.

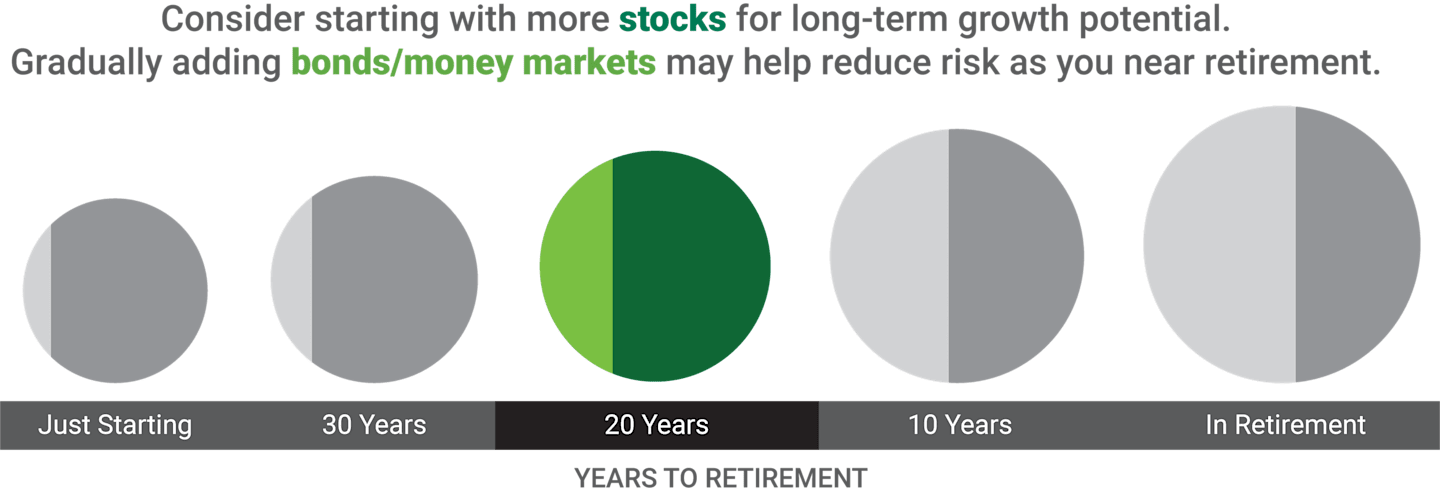

As your salary increases, commit to investing as much as you can. Your regular contributions and the return potential of stocks are both important factors as you seek to grow your account balance. A smaller allocation to bonds may help hedge against market downturns.

Source: American Century Investments. For illustrative purposes only. The examples indicate hypothetical allocations. The circles assume increased contributions over time and are not meant to indicate gains based on market performance.

Your specific percentages of stocks, bonds and money market investments will vary depending on your own goals, time frame and risk tolerance, but this may give you a place to start as you evaluate your current and future investment plans.

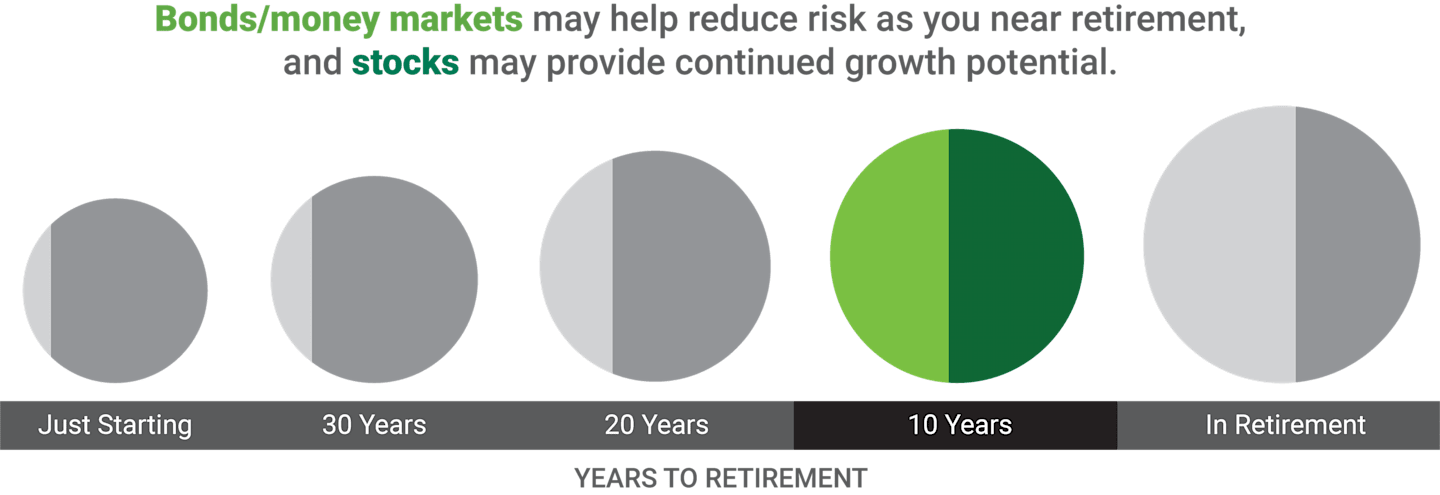

Risk looks different if you’ve got more to lose, especially if you’re counting down to your last paycheck. After years of saving, you’ll want to preserve your money. Balance your growth potential with conservative investments that may offer a buffer in case of market volatility.

Source: American Century Investments. For illustrative purposes only. The examples indicate hypothetical allocations. The circles assume increased contributions over time and are not meant to indicate gains based on market performance.

Your specific percentages of stocks, bonds and money market investments will vary depending on your own goals, time frame and risk tolerance, but this may give you a place to start as you evaluate your current and future investment plans.

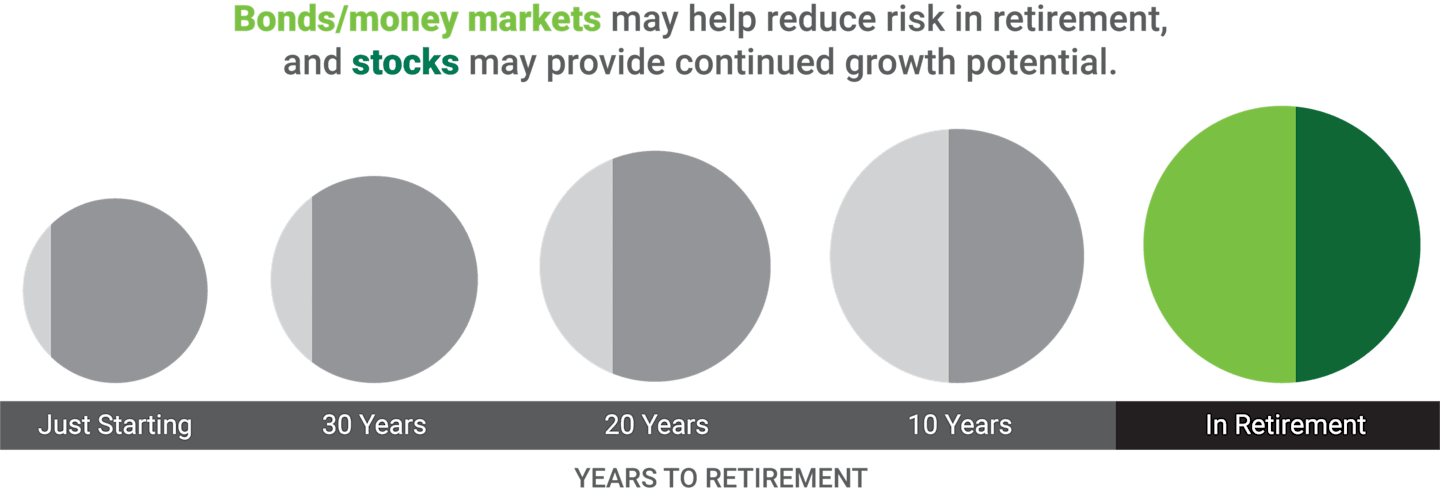

You’ll need to have a plan to make sure your money lasts. Calculating your expenses can help you determine a suitable withdrawal rate from your investments. Too little and you’ll have to adjust your lifestyle. Too much and you’ll deplete your accounts. (Learn more about retirement income strategies or talk to a financial consultant.)

Source: American Century Investments. For illustrative purposes only. The examples indicate hypothetical allocations. The circles assume increased contributions over time and are not meant to indicate gains based on market performance.

Your specific percentages of stocks, bonds and money market investments will vary depending on your own goals, time frame and risk tolerance, but this may give you a place to start as you evaluate your current and future investment plans.

Talk to a Professional

If you're sensitive about taking risks with your money, you may need to speak with a financial professional who can explain how to manage general investment risk and choose the right risk level for your situation. Even if you feel your risk tolerance is at zero, that doesn't mean that you should avoid investing completely.

Authors

Financial Consultant

Balance Your Risk and Reward

We can help you understand investment risks—and how to manage them—to help you make better investment decisions.

You could lose money by investing in a mutual fund, even if through your employer's plan or an IRA. An investment in a mutual fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

Generally, as interest rates rise, the value of the bonds held in the fund will decline. The opposite is true when interest rates decline.

Diversification does not assure a profit nor does it protect against loss of principal.

The letter ratings indicate the credit worthiness of the underlying bonds in the portfolio and generally range from AAA (highest) to D (lowest).

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.