States at 250: What Federal Funding Changes Mean for Muni Investors

While the credit quality of our 50 states remains healthy overall, shifting federal funding keeps active municipal bond managers on watch.

Key Takeaways

As we noted in our 2026 Muni Outlook, state credit quality remains strong. All states have investment-grade ratings, and most land in the AA category.

States are better-positioned than local governments to raise revenues, reduce expenses and pass through spending cuts from federal funding reductions.

Active management and a focus on stringent municipal credit research may help identify pockets of opportunity and areas of stress.

With America preparing to celebrate its 250th birthday (the semiquincentennial), we’re taking stock of the nation’s 50 states. As municipal bond investors, we’re particularly interested in select states’ financial and credit conditions.

What Federal Funding Changes Could Mean for State Budgets

Thanks to their diverse economies, healthy reserves and ability to pass costs to local governments, most states have maintained relatively healthy credit standings. However, some states are starting to feel the pinch of slower revenues and accelerating expenses. This means they may not be able to absorb all the funding cuts in store for key federal programs.

Figure 1 summarizes the challenges and impacts to the states for four large federal programs undergoing funding shifts:

Medicaid: The federal and state governments share the costs of this low-income health care program, which covers approximately 20% of the U.S. population.

Supplemental Nutrition Assistance Program (SNAP): SNAP provides monthly food stipends to low-income households.

Federal Emergency Management Agency (FEMA): FEMA provides disaster relief across the country.

Transportation infrastructure: The U.S. Department of Transportation delivers financial support for various capital projects and ongoing maintenance.

Figure 1 | More Funding Responsibilities Shift to the States

Sources: Centers for Medicare and Medicaid Services, U.S. Department of Agriculture, Federal Emergency Management Agency, U.S. Department of Transportation, U.S. Congress.

Medicaid cuts, which account for the largest share, don’t take effect until 2028, giving states time to adapt. Overall, we don’t expect major credit rating changes for states. But we believe these federal budget cuts underscore the need for active management and a research team that can identify pitfalls and downstream effects.

2027 Proposed Budgets Include Some Surprises for Highly Rated States

The 2027 budget cycle finds many AAA-

For example, North Carolina, known for historically stable revenue growth and strong expenditure control, failed to pass its biennial budget last year. The state is operating on fiscal 2025 funding levels. Additionally, Minnesota projects a near-term surplus but unexpected out-year deficits.

Elsewhere, Tennessee’s proposed budget contracted by 9.6%, driven largely by a 22% reduction in federal funding for the general fund. Meanwhile, Maryland closed its $1.5 billion budget gap by reducing expenses and drawing on reserves.

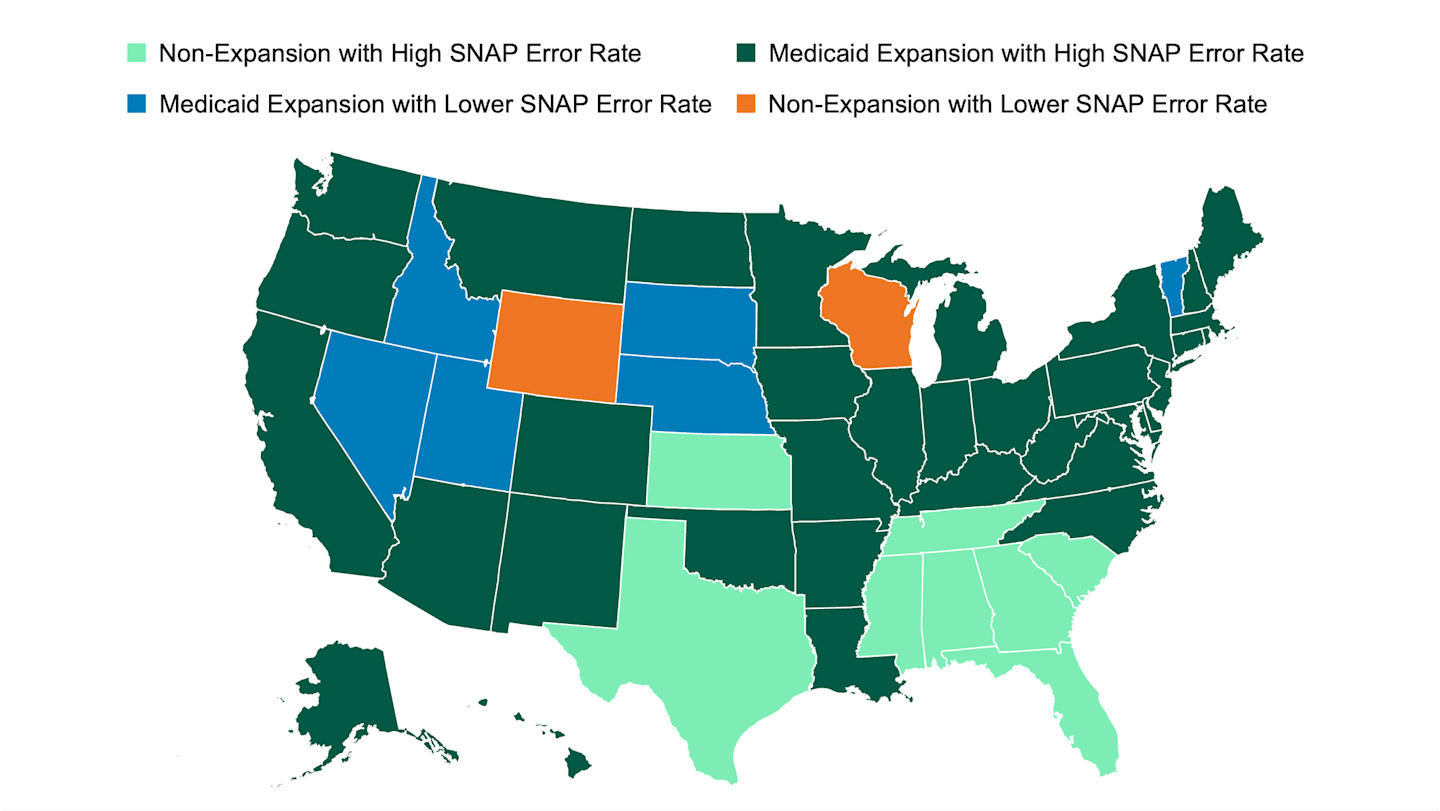

Most States Expanded Medicaid While Facing SNAP Funding Swings

Figure 2 shows the 35 states (dark green) exposed to both Medicaid and SNAP funding shifts. States in mint green didn’t expand Medicaid but have high SNAP payment error rates that will likely trigger an increased state match.

Figure 2 | Most States Face Higher Medicaid and SNAP Funding Responsibilities

Sources: Kaiser Family Foundation, May 21, 2026; U.S. Department of Agriculture, June 30, 2025.

How States Could Adjust Their Budgets

Near term, we expect highly rated states to balance their budgets, though some may need to tap reserves to do so. Most states are actively working to avoid increased SNAP costs by reducing payment errors but have delayed final policy decisions related to Medicaid funding.

Given the size of the Medicaid program, we don’t expect states to fully backfill funding, which will likely pressure county-owned hospitals to provide safety net care. We regularly monitor Medicaid costs in California, Illinois and New Jersey, but we may flag other states for enhanced monitoring. We view states that anticipate and proactively address shortfalls and backfill funding as engaging in credit-positive actions.

Officials in California, Washington and Illinois are considering wealth taxes to help backfill funding. California’s Santa Clara County anticipated the state’s inability to backfill funding and passed its own sales tax increase last fall.

Elsewhere, Rhode Island, Michigan and Pennsylvania have decoupled certain taxpayer provisions from the OBBBA to prevent significant revenue shortfalls.

According to the National Governors Association, 39 states are holding gubernatorial elections in 2026, with 18 incumbents seeking reelection. States with the ability to adjust budgets mid-cycle could make changes, especially if the political party shifts.

Why Municipal Credit Research Matters When Funding Shifts

As always, rigorous credit research represents the foundation of our investment process. As various funding provisions of the OBBBA unfold, our research team is diligently monitoring responses from state and local officials. Our goal is to assess the funding solutions and identify areas of stress and pockets of opportunity.

Authors

Senior Portfolio Manager

Senior Municipal Credit Analyst

Learn about the tax advantages of municipal bonds.

Investment return and principal value of security investments will fluctuate. The value at the time of redemption may be more or less than the original cost. Past performance is no guarantee of future results.

Diversification does not assure a profit nor does it protect against loss of principal.

Generally, as interest rates rise, the value of the bonds held in the fund will decline. The opposite is true when interest rates decline.

The opinions expressed are those of American Century Investments (or the portfolio manager) and are no guarantee of the future performance of any American Century Investments portfolio. This material has been prepared for educational purposes only. It is not intended to provide, and should not be relied upon for, investment, accounting, legal or tax advice.